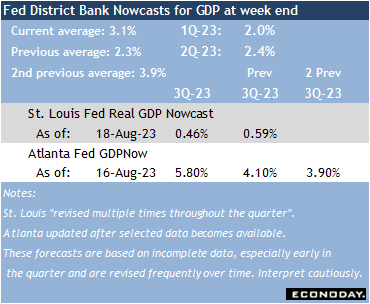

The economic data in the August 21 week will take a backseat to the annual Jackson Hole Symposium over the three days of August 24-26. This year’s topic is “Structural Shifts in the Global Economy”. The annual meeting of the minds is intended to have a more academic tone, but the gathering of policymakers means it is an opportunity to gauge their policy leanings. The focus will be on remarks from US central bankers regarding the outlook for Federal Reserve monetary policy. Powel is scheduled to give his speech on the “Economic Outlook” at 10:05 ET on Friday.

Markets will be listening for any signal about the next steps in FOMC interest rate decisions. The most immediate question is whether there will or will not be a rate hike at the September 19-20 meeting. After that, it will be the tone of a more general outlook for inflation and employment and if that means Fed policymakers are at or nearing the end of the current tightening cycle.

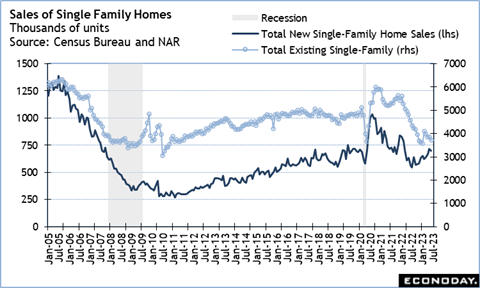

The economic data may feel a bit out of date. In particular, the June numbers on sales of existing homes at 10:00 ET on Tuesday and new single-family homes at 10:00 ET on Wednesday will not have caught up with the more recent jump in mortgage rates. Nevertheless, sales of existing homes should continue to reflect the squeeze that limited supplies of homes available for sale have put on that side of the housing market. Sales of existing homes are closings of contracts taken out a month or more before July. Some of the sales activity will be due to potential homebuyers who managed to pre-qualify for a mortgage at a lower rate in May or June who were lucky enough to find a suitable home to purchase.

This will be true for sales of new single-family homes as well. However, for new homes, those who have a mortgage loan already secured can commit to buying a home that has not yet started or is under construction. The lack of inventory of existing units is driving homebuyers to look at new homes. Historically new homes accounted for about one-fifth of sales, but at present it is close to a third.

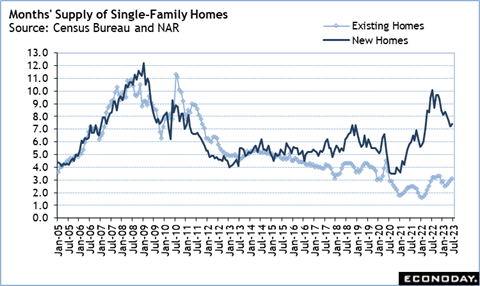

Where a household has a mortgage rate roughly under 6 percent, it is more likely to spend on renovation and repair rather than give up a more affordable loan. This will keep existing units off the market until rates decline again. At present, the rate for a 30-year fixed rate mortgage is around 7 percent, the highest in over 20 years. This is driving some buyers to take out adjustable-rate mortgages to reduce their initial monthly payments while hoping to refinance at a lower rate before the reset. In turn, this sets up a potential wave of refinancing activity when mortgage rates decline enough to make it worthwhile to get a fixed rate at or below the rate of the original ARM loan.