Now that Fed Chair Jerome Powell has delivered his speech at the Jackson Hole Symposium, Fedwatchers will set their expectations for the next FOMC meeting on September 19-20. Powell spoke about policymakers needing to be “agile” and responsive to incoming data. The only thing certain is that the tone of the remarks was definitely hawkish in terms of the inflation fight. It remains to be seen if the economic data support a sense of urgency regarding inflation, or if there is enough evidence that financial markets and/or lagged effects of past rate hikes that a pause will follow the 25-basis-point increase on July 26.

In the August 28 week there is a run of data that will illuminate conditions in the labor market. These are JOLTS for July at 10:00 ET on Tuesday, the ADP national employment report for August at 8:15 ET on Wednesday, the Challenger report on layoff intentions in August at 7:30 ET on Thursday, initial jobless claims at 8:30 ET on Thursday, and last but most importantly, the employment situation for August at 8:30 ET on Friday.

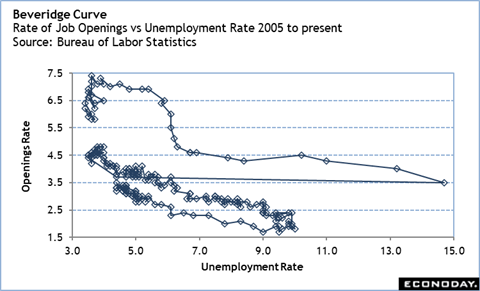

The question awaiting the data is whether the Fed’s path of restricting monetary policy has had the desired effect of addressing the imbalance in labor supply and demand without materially sending workers into the ranks of the unemployed. What the data are expected to show is that businesses have fewer open positions – either through attrition or finding someone to fill them. Hiring should be slower overall but at the same time layoffs remain relatively rare outside of a few narrow sectors. Fed policymakers anticipate a cooling in the labor market.

The August employment report will need to be read particularly carefully. The August number for nonfarm payrolls has a strong tendency to come in below the consensus estimate and then be revised higher in the subsequent month. August can be a tough month for surveying households and establishments with many people on vacation, in transition from vacation to the school year, and/or for summer seasonal work. Additionally, there are some ongoing work stoppages that may mean fewer hires and/or some temporary layoffs while negotiations continue. These jobs should boost payrolls when strikes are settled. A soft August report for nonfarm payrolls will need to be taken in these contexts.