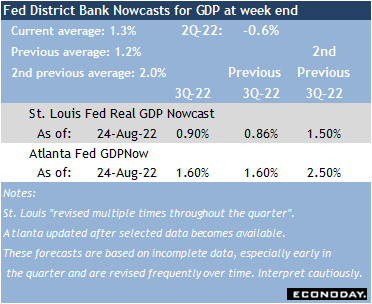

The focus for the coming week is going to be data related to the labor market. To all appearances growth in the US economy is slow. The Bureau of Economic Analysis has reported a shallow economic contraction for the first and second quarters; early forecasts for the third quarter expect a return narrow expansion. It looks like the housing sector is in a recession as of the July data. Manufacturing and services are both looking weak in the early August surveys.

The labor market is what has kept an outright recession at bay. The numbers suggest still plentiful job openings, a brisk pace of hiring – although some of that may be part-time work or second jobs – while layoff activity remains limited. This week’s crop of labor market reports is the last major one the FOMC will have in hand before the September 20-21 meeting.

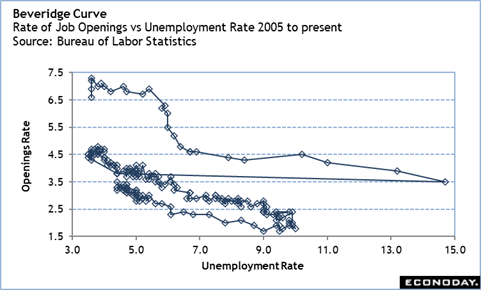

The July numbers on job openings and labor turnover (JOLTS) are at 10:00 ET on Tuesday. These data lag much of the other jobs data by a month but should still have something to say about what businesses are doing with all those job openings. Are they finding workers and hiring? Are they eliminating unfilled positions? Are workers still confident enough to leave one job for another? The Beveridge Curve – which compares the rate of job openings to the national unemployment rate – should show if conditions are starting to display a more balanced state between available jobs and the supply of labor.

Wednesday at 8:15 ET will see the return of the ADP national employment report with new and revised data after an overhaul of the report’s methodology in partnership with the Stanford Digital Economy Lab. The report for August is supposed to “deliver a richer labor market analysis”. It will likely take a few months to fully appreciate and understand the changes in the report. Nonetheless, having a first look at what is happening with private payrolls in August could bring some last-minute influence on expectations for Friday’s employment situation.

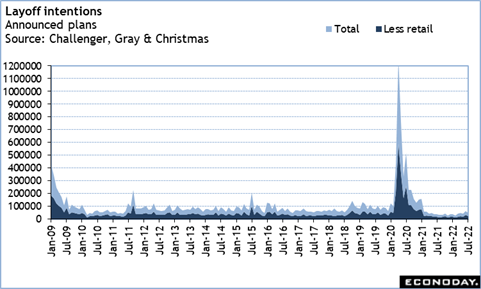

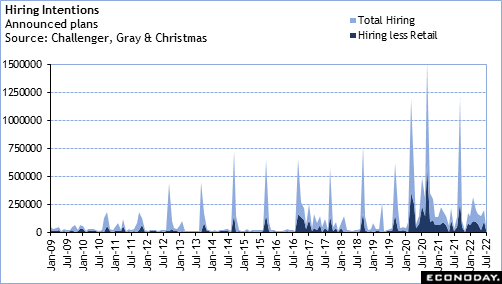

The Challenger numbers on layoff intentions for August at 7:30 ET on Thursday will also help shape perceptions of the labor market. So far there have not been widespread layoff plans even as the economy slows. The data on hiring intentions may include the first wave of plans to add seasonal workers for the upcoming holiday season. Plans for 2022 are likely to be modest given the shortage of labor. Retailers may be intending to only hire limited numbers of temporary workers out of concern for a sharper downturn in the economy. There is also the issue of whether stores are going to have the inventory to power holiday sales events. Lean shelves may push more shoppers online. Delivery services are likely to see a need for extra help in the coming months.

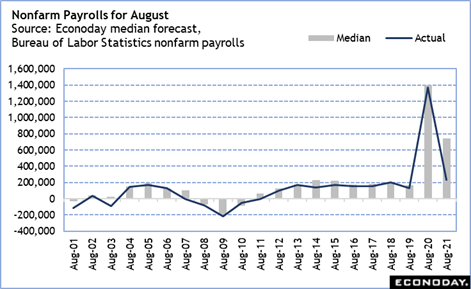

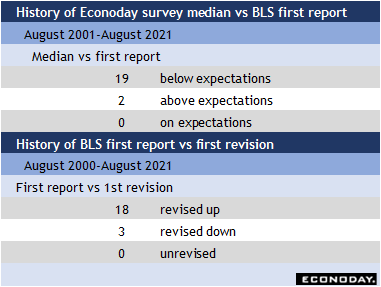

On Friday at 8:30 ET, the Bureau of Labor Statistics will release the August employment situation. Early estimates for nonfarm payrolls are around the 300,000-mark. Keep in mind that the July report had a big upside surprise. It is possible that the August number will be weak in comparison. The history of the median expectation in Econoday’s surveys for August payrolls shows that it consistently comes in below the consensus, although this is also almost always revised higher in the subsequent report. If there is a downside surprise in August, it should be taken as payback for an oversized increase in the prior month.