The August 7 week is going to be a sleepy one for economic data with only two reports likely to wake up markets.

With the July employment data out of the way, the focus for the monetary policy outlook will shift back to the inflation measures. Front and center will be the July CPI at 8:30 ET on Thursday. The June report raised hopes that inflation was not only moving in the right direction, but that the path lower was sustainable. The July numbers may disappoint those hopes. In particular, increases in energy costs will probably boost the all-items CPI year-over-year rate. If there isn’t much progress bringing the core CPI annual rate lower, the stage will be set for another rate hike as soon as the September 19-20 FOMC meeting. The data in the monthly employment report and others related to the labor market suggest that the FOMC will not be overly concerned about maintaining the maximum employment side of the dual mandate.

The CPI report is the first of the third quarter 2023. The July CPI-U will give a hint as to what the Social Security cost-of-living-allowance will be in January 2024. If there is an uptick in inflation in the July-September period, recipients can look forward to an above average increase again, although not on the scale of the 8.7 percent increase for 2023.

The final University of Michigan consumer sentiment index in July was 71.6, up 7.2 points from 64.4 in June, and the highest since 71.7 in October 2021. If the index manages to rise further when the preliminary index for August is released at 10:00 ET on Friday, it will confirm that consumers are getting past the gloom related to the increase in inflation in early in 2021 and are more confident that the worst of the current price episode is past. The level will remain well below pre-pandemic readings, but the labor market and rising wages are helping to improve confidence.

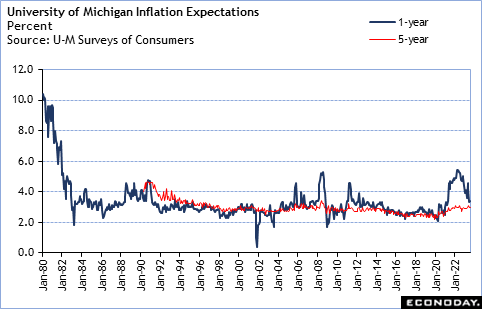

Also in the University of Michigan survey of consumers, Fed policymakers will be watching to see if inflation expectations remain well anchored. Recent gains in gasoline prices are likely to send the 1-year inflation expectations measure higher, but the 5-year inflation expectations measure should remain around the 3 percent mark.