The December 2 week will start off with a lot of recaps of conditions for retailers over the Thanksgiving weekend and running interest in how Cyber Monday looks for the winter holiday sales period. Retailers at both brick-and-mortar stores and e-commerce sites have been heavily advertising deals and discounts well in advance of Black Friday, Small Business Saturday, or any of the other themed sales pushes. Looking at the post-Thanksgiving days is reflexive but spending on gifts and services is more spread out in recent years with early shopping and one- and two-day delivery services. It could be hard to tell if this is a good year for retailers until the December data becomes available in January.

The final FOMC meeting of 2024 is on December 17-18. Markets will be keeping an eye on conditions in the labor market and for inflation and inflation expectations. The coming week will have a lot of data related to the labor market, but none more important than the monthly employment situation at 8:30 ET on Friday. Note that the FOMC communications blackout period around the FOMC meeting goes into effect at midnight on Saturday, December 7. Any message Fed policymakers want to convey will have to be made before then. The period lifts at midnight on Thursday, December 19.

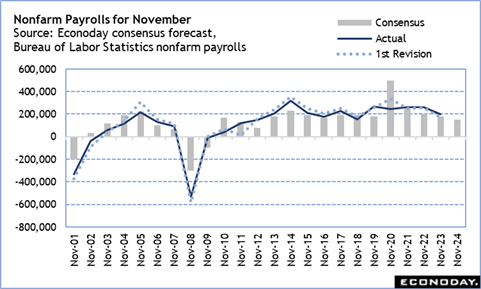

The October change in nonfarm payrolls was a measure increase of 12,000 that was due mainly to two special factors. First was strike activity. There was Boeing which affected 38,000 workers and thereby reduced manufacturing payrolls by a similar amount and 3,400 hotel workers in Hawaii which cut into leisure and hospitality payrolls. These were both settled early in November and workers will return to be counted as on payroll. Second is hard to quantify impacts from Hurricane Helene in late September and Hurricane Milton in early October. A clearer picture should emerge in the November data about outright job losses or where workers were temporarily idled.

Another thing that could impact November payrolls is there is a 5-week survey reference period between October 12 and November 16. It is possible that some job gains from October were not captured in last month’s report and will show up in November.

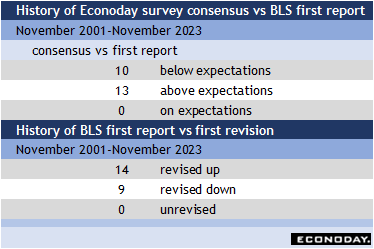

In any case, it may be a bit challenging to place the November employment report in the historical context. November nonfarm payrolls have a mild tendency to come in below expectations but are almost equally likely to be revised higher in the subsequent report.