Entering the December 5 week, the focus will be less on the economic data and more on the FOMC meeting on December 13-14. The communications blackout period around the meeting is in effect between midnight Saturday, December 3 and midnight Thursday, December 15. There will be no comment about monetary policy from Fed officials in the coming week, and none of the data on the economic calendar is likely to affect thinking about the meeting’s outcome. At this writing, expectations are broadly in line with a 50 basis point hike in the fed funds target range from 3.75-to-4.00 percent to 4.25-to-4.50 percent. Chair Jerome Powell’s recent remarks have reinforced anticipation of a slower pace of rate increases. More in question is whether this will be the last hike for a while as the FOMC allows time for prior sharp hikes to show through into inflation data and correct supply/demand imbalances.

The only inflation number on the calendar for the coming week is the November Final Demand PPI at 8:30 ET on Friday. The FOMC tends to pay more heed to the CPI numbers, but any evidence about inflationary pressures will get a hard look at this stage of the efforts to bring down pressures. Data for October showed a modest letup in price pressures, but one month’s data is not a trend. In any case, the FOMC will have the November CPI in hand at their meeting when those numbers are released at 8:30 ET on Tuesday, December 13.

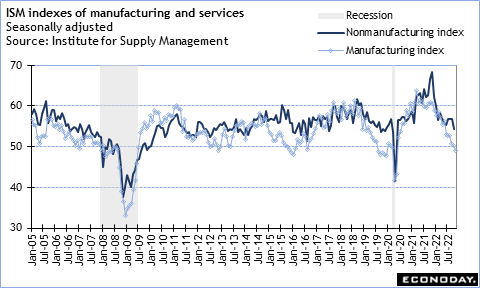

The release of the ISM Manufacturing Index on December 1 showed a drop to 49.0 in November. This isn’t a recessionary number for the factory sector, but it is an uncomfortable reading in regard to concerns about an economic downturn. The ISM Services Index at 10:00 ET on Monday is expected to maintain its mildly expansionary tone and should offer some reassurance that a recession isn’t immediately in the works. Note that Econoday’s Consensus Divergence Index has been running positive in the mid-single digits, indicating that U.S. data have been coming in a bit stronger than expected.

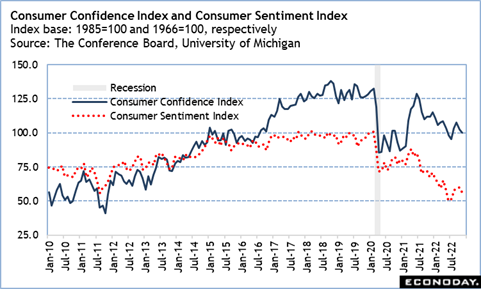

The preliminary University of Michigan Consumer Sentiment Index for December at 10:00 ET on Friday could manage to improve over November’s tepid 56.8. Consumers continue to fret about inflation – with good reason – and are unhappy about rising interest rates that have affected major spending decisions. However, gasoline prices – one of the big drivers of consumer confidence – are retreating steadily and retailers are offering discounts that could help cushion other areas of price increases.

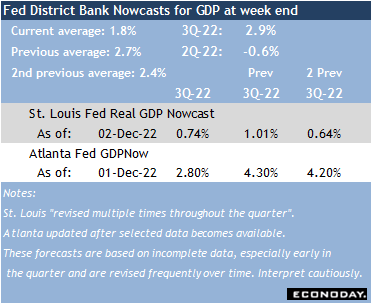

It remains too early to call whether GDP Nowcasts for the fourth quarter will remain positive as the release of November data progresses. The November employment report was a solid one that shows the labor market is in decent shape – so far. But both Nowcasts from the St. Louis and Atlanta Feds point to a less optimistic forecast than in recent weeks. The next report likely to heavily influence forecasts is the November retail sales report on Thursday, December 15 at 8:30 ET.