There are two reports in the February 13 week that will be closely examined for hints about the direction of monetary policy and the state of the US economy.

First is the January consumer price index on Tuesday at 8:30 ET. There’s an ongoing gap between market expectations that the FOMC will lower short-term rates later this year and Fed policymakers’ rhetoric that rates are going to rise further – although not much – and stay restrictive for longer. The January CPI data, however, will not resolve this. Consumers are likely to see higher prices in the food and energy sectors – the most prominent examples of which are eggs and gasoline. Outside of the more volatile sources of inflation and the ones which have provided the most relief for the inflation trend, Fed officials are going to be looking at non-housing services prices (such as medical and transportation services). This is where inflationary pressures have proven the most persistent and where the most sustained improvement will have to happen before rates start to come down again.

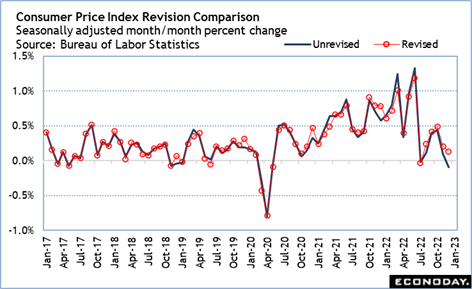

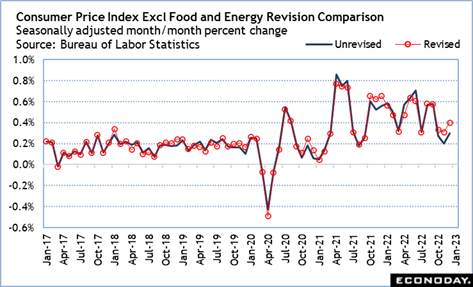

Note that the Bureau of Labor Statistics released annual revisions back five years on Friday, February 10. The last three months of 2022 were revised slightly higher in the seasonally adjusted data. Annual revisions for the producer price index will be released on Tuesday, February 14 and will also be for five years prior. The January PPI report is set for Thursday at 8:30 ET. The January report for import and export prices is on Friday at 8:30 ET, but these indexes are unadjusted and therefore not subject to annual revision.

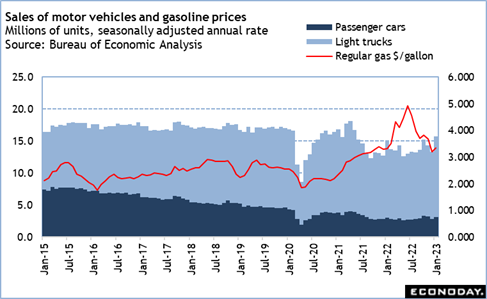

Second most important report in the week is the January numbers for retail and food service spending. The December numbers were a disappointment. It is possible there will be some upward revision as late-month spending is captured. January’s total is likely to be higher due to a jump in purchases of motor vehicles and an uptick in prices for gasoline. What will be more telling about consumer spending in January is the other categories. The available indexes for retail activity suggest that spending was sluggish at the start of the year as consumers considered the prospect of a recession and a more uncertain job market.

The Atlanta Fed’s GDPNow for the first quarter 2023 estimates GDP at up 2.1 percent. It is far too early to think that this forecast will hold up given that a significant amount of data have yet to be published. But it does point to the sort of subpar economic growth that Fed policymakers are talking about while the fight to tame inflation continues.