The January 16 week starts with a federal holiday on Monday to observe Marin Luther King, Jr. Day. There will be a full close for both the bond and stock markets. There will be little impact on the data release schedule for the week, although Treasury offerings and auctions will see some shifts.

The two big reports to look forward to are December numbers on retail sales at 8:30 EST and the Fed’s Beige Book at 14:00 EST, both on Wednesday.

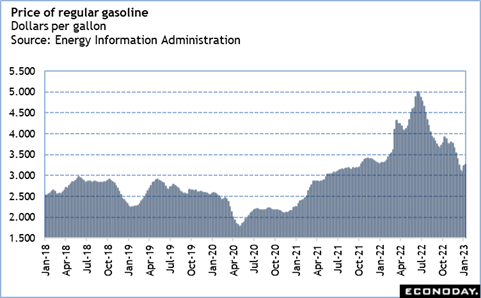

The December report on retail and food services sales will seal the outlook for personal consumption expenditures when the advance estimate of fourth quarter GDP is released at 8:30 EST on Thursday, January 26. Consumers got a break on gasoline prices in December which could boost discretionary spending in other categories. Holiday travel may also have increased, boosting the volume of gasoline sales which could mean the dollar value at gas stations won’t drop as much as lower prices might imply. Unit sales of motor vehicles declined in December, so that component will probably drag on the overall total. Softness in the housing market may mean that components like furniture and appliances will be down, although it is possible that anticipation of holiday entertainment added some sales. Consumers probably went out to eat more in December though food price inflation may have increased the dollar value of sales without increasing the volume. Finally, it remains to be seen if holiday gift shopping picked up for other types of merchandisers, whether brick-and-mortar or online.

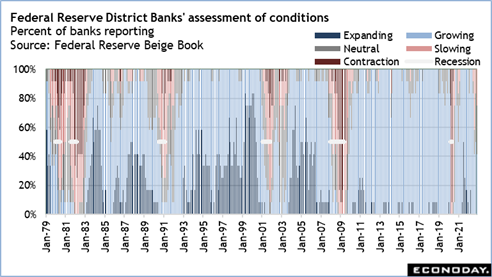

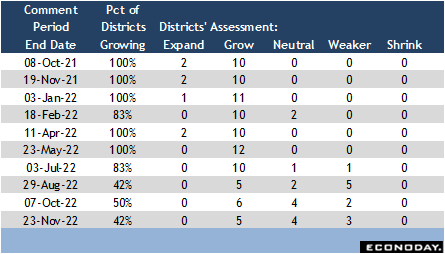

The Fed’s Beige Book will provide anecdotal evidence of economic conditions across the 12 District Bank for the period between late November and early January. The tone of the last three Beige Books has strongly suggested that the US economy is in recession, or at least in a period of marginal growth. There may be evidence of how the FOMC’s aggressive string of rate hikes is affecting activity outside of the impacts already seen for the housing sector, and prices paid. It will also have something to say about labor market conditions and if these have eased at all since the last report. The tone of the report could mean the difference between a 25 or 50 basis point rate hike at the January 31-February 1 FOMC meeting.