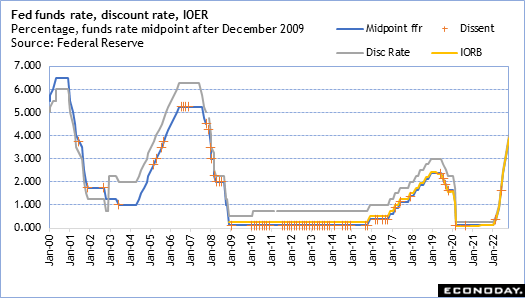

The January 30 week will see a laser-focus on the outcome of the January 31-February 1 FOMC meeting. It is not in question as to whether FOMC voters will raise the fed funds target range after their deliberations. What is unsure is by how much – the probable 25 basis points or less likely 50 basis points – and if the Committee will signal a slower pace of hikes or even a pause to wait for the data to catch up with prior rate increases.

The Fed will release the FOMC meeting statement and implementation note at 14:00 EST on Wednesday. There will be no official update to the Summary of Economic Projections (SEP) at this meeting. Given the uncertainties around current economic conditions and the risks facing the near future, there could be a dissent in the vote, although I consider it a remote possibility. Fed policymakers are united in their determination to tame inflation.

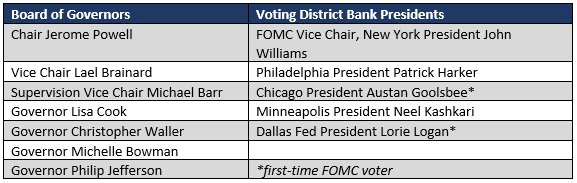

This meeting will see the rotation of voting district bank presidents. The voters in 2023 and through the first meeting in 2024 are:

Few of the voters on the FOMC have explicitly said they are leaning toward a 25 basis point rate hike. Waller and Harker have done so. Most of the rest have indicated a slower pace of hikes is on the table, which implies 25 basis points after the 50 basis point hike in December. What should not be inferred is that even if it is signaled that the probable February increase is expected to be the last for a while – by no means a certainty – is that the FOMC is not going to leave monetary policy restrictive for an extended period. Anticipation of a reversal of rate hikes is premature. Of course, it will depend on the economic data. But unless Fed policymakers have solid evidence that inflation is sustainably down, monetary policy will remain tight.

Powell will hold his press conference at 14:30 EST. I would expect that he will defer most questions about the outlook for monetary policy for the March 21-22 meeting when the FOMC officially updates the SEP. He will be peppered with questions about the easing in financial conditions despite higher interest rates, and how this will affect the outlook for monetary policy. He may be asked questions similar to those he will face in the February semiannual monetary policy testimony that is expected to take place in mid- to late February after it is scheduled with the House Financial Services Committee and Senate Banking Committee. He will be asked about the threat of recession in light of recent weaker economic data.

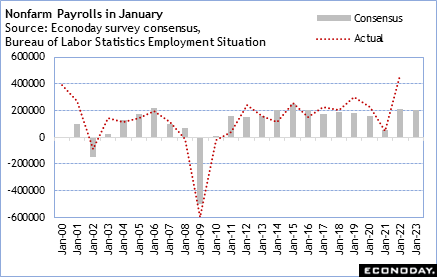

Once the FOMC meeting is out of the way, attention will turn to the January employment situation report set for release at 8:30 EST on Friday. This report will include annual revisions to the establishment survey; annual revisions to the household survey were released last month. There are concerns that revisions to what have been strong payroll gains could be drastically lower than previously reported, and thus cast the pace of hiring in a much weaker light. Nonetheless, the unemployment rate, which is based on the household survey, should remain consistent with a tight labor market. As an aside, the FOMC will not have this data when it meets earlier in the week. The rate decision may encompass caution about the tone of the labor market data in the wake of the report.

The January payroll data is difficult to forecast due to the timing of the annual revision. A rough early consensus is for up 200,000, a bit slower than the recent trend. However, look for a wide range of forecasts that will try to account for the possible large downward revision in the 2022 data. It is not unusual for the forecast consensus to miss, and miss big.