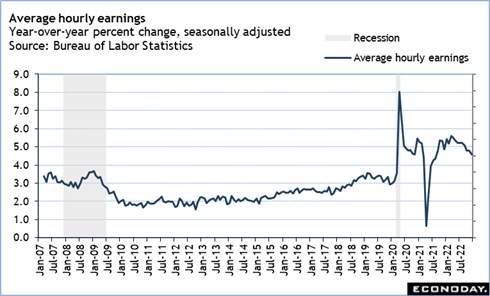

The January 9 week has a light data schedule. There will be time to consider the implications of the December jobs report from Friday, January 6 on the direction of monetary policy when the FOMC next meets on January 31-February 1. With the labor market showing no sign of improvement in the imbalance of supply and demand for workers, attention will turn to what is going on in the inflation front. The December year-over-year change for average hourly earnings cooled by 2 tenths to 4.6 percent, moderation that marks a positive development for Fed policymakers as they work to bring about a soft(ish) landing for the economy. But what about price inflation?

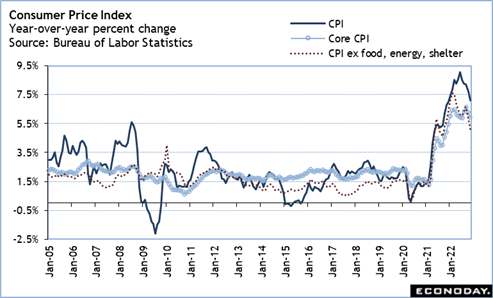

The highlight of the economic data calendar will almost certainly be the December CPI at 8:30 EST on Thursday. The total CPI was up 7.1 percent year-over-year in November and has been on the decline since the near-term peak of up 9.1 percent in June. The core CPI was up 6.0 percent in November, coming down from its near-term peak of up 6.6 percent in September. It is expected that the December report will see a little more easing in upward price pressures. Nonetheless, the pace will still be deemed too high by Fed policymakers. Do not expect even a below expectations report to change the outlook for yet more rate hikes. Sources of inflation for items that deeply affect consumer nondiscretionary spending – food, energy, and shelter – are still uncomfortably high and there are other sources among non-housing services that are contributing.

The course of inflation is interconnected with business and consumer confidence, both of which have been posting still weak readings. Given worries about a recession, confidence is going to improve much. The NFIB small business optimism index for December at 6:00 EST on Tuesday may well give back some of November’s meager gain to 91.9. The preliminary University of Michigan consumer sentiment index for December at 10:00 ET on Friday should do a little better than the final reading of 59.7 in November, but remain soft.

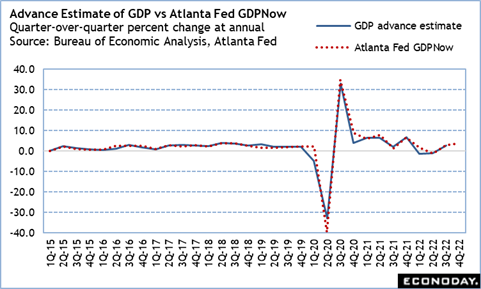

Now that the December economic data reports are coming in, the GDP nowcasts are starting to firm up. At present there is only one Fed district bank that has a GDP forecast – Atlanta. Fortunately, Atlanta’s GDPNow has a good correlation (0.981) with the advance GDP estimates. On Thursday, January 5, the Atlanta estimate was 3.8 percent for the fourth quarter 2022. The BEA’s advance estimates of fourth quarter GDP will be released at 8:30 EST on Thursday, January 26.