The central question of the June 12 week is if the FOMC will pause in the current rate hike cycle at the end of the June 13-14 meeting or will it decide on another 25 basis point increase in the fed funds target range?

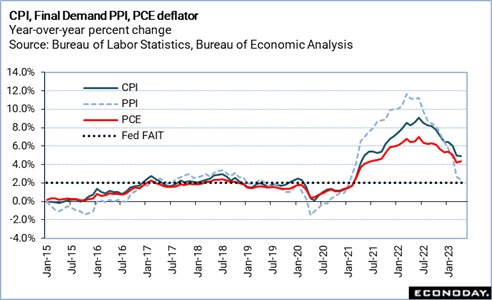

The answer greatly depends on what the May CPI report has to say at 8:30 ET on Tuesday. All FOMC participants would agree that inflation is too high and the Fed’s work is not yet done to tame it. Where unanimity fails is if it is time to wait to let some of those long and variable lags in the impact of past rate hikes – 500 basis points from March 2022 – show through in the data. Most policymakers would rather hike too much and/or leave restrictive policy in place longer than allow inflation to become entrenched. However, all would like to avoid erring on either letting up too soon or too late. Policymakers have been focused on core inflation measures – excluding food and energy – and more narrowly on non-housing services inflation which has proven less responsive than the demand side of inflationary pressures. If CPI core inflation points to another month of persistent inflation pressures at the core, then a rate hike is more likely. If there are signs of improvement, a pause becomes the more probable outcome.

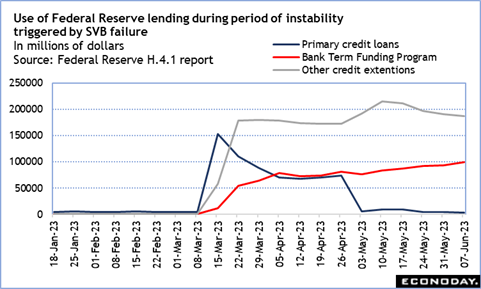

Also to be taken into account is if credit conditions have tightened sufficiently to do some of the work of another rate hike. The period of instability triggered by the failure of Silicon Valley Bank is not yet over if the lending data in the Fed’s weekly H.4.1 report is any indication. However, the data also indicate that banks are getting needed liquidity while they address their risk management problems. Other credit extensions – including loans to the FDIC – are falling, but not much, while use of the Bank Term Funding Program – implemented for this current problem – continues to see an increase in lending, albeit slowly.

Whatever the decision, Fed Chair Jerome Powell will face a grueling task in explaining the FOMC’s action and placing it within the context of the current economy and policymakers’ outlook. The statement will be posted at 14:00 ET on Wednesday, and he faces the press at 14:30 ET. There will be an update to the quarterly Summary of Economic Projections (SEP) at the meeting that will be released along with the statement. If there is no pause in rate hikes after the June deliberations, the collective forecast is likely to signal one for the near future. More interesting could be if the forecast suggests any alteration in the expected timing of the next downward rate move. Markets have been longing for a rate cut while Fed officials have pushed back on that hope with a consistent message that restrictive policy may be in place for some time.

The other important information in the week is the May data on retail and food services sales at 8:30 ET on Thursday. The FOMC will not have access to this in making their decision. Sales of motor vehicles declined sharply in May which will reduce the dollar value of total sales. Gasoline prices were also lower in May which could reduce the dollar value of sales at service stations, although there may be some offset if people were driving more. Recent upticks in home sales may benefit some sectors like home furnishings and appliances. But overall, retail spending will probably be on the soft side in May.