The June 26 week closes out the second quarter 2023 with little economic data likely to cause any surprise in the days leading up to what will be for many the long Independence Day weekend (Saturday, July 1 through Tuesday, July 4). The reports on the calendar will probably only affirm what is already known.

There should be nothing to freshen the outlook for Fed monetary policy after Chair Jerome Powell’s two-day appearance for the semi-annual monetary policy testimony (House Financial Services Committee on June 21, Senate Banking Committee on June 22). Between the holiday next week and the start of the communications blackout period around the July 25-26 FOMC that begins at midnight on July 15, there’s only a small window which Fed officials could use to update their thinking. However, Powell’s characterization of the FOMC’s current meeting-by-meeting approach to monetary is likely to stand. Forward guidance isn’t likely to emerge any time soon.

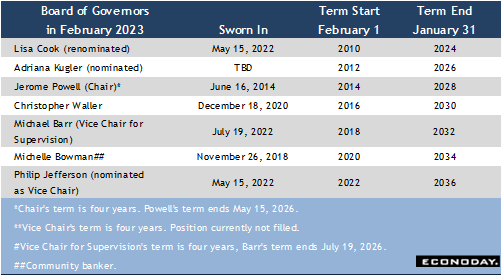

On a side note, it will be interesting to see how quickly the Senate Banking Committee makes its recommendations on Board of Governor nominations for which it held hearings on June 21, and how soon after that the nominees receive a vote. Governor Philip Jefferson has gotten the Biden Administration’s nod to become Vice Chair. Governor Lisa Cook is currently a governor with a term set to expire on January 31, 2024. She has been renominated for a full 14-year term. Finally, Adriana Kugler has been nominated to fill an unexpired term ending January 31, 2026. None of these are controversial nominations, although it is possible that politics will make it more difficult to confirm. Also, the search for new president at the Kansas City Fed has not yet resulted in an announcement of a choice.

The third and final estimate of first quarter GDP is set for release at 8:30 ET on Thursday. The second estimate put growth at 1.3 percent, and probably won’t see much, if any, revision. The pace of expansion was below trend, as Powell likes to say, but somewhat of an upside surprise given the headwinds to the US economy. The Fed district bank GDP Nowcasts are pointing to another soft reading in the second quarter, but the data are too incomplete to make a reliable prediction. Likely the most important conclusion is that at least so far, with the aid of a strong labor market, the US economy is sufficiently resilient to remain out of recession despite the aggressive series of rate hikes begun in March 2022 to fight inflation.

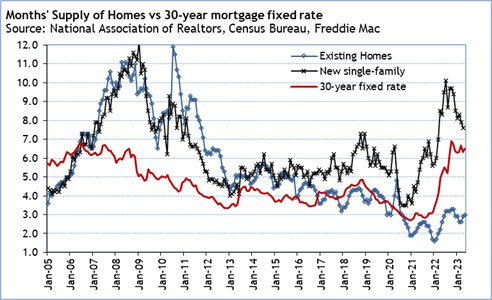

The other data reports to keep an eye on are those related to the housing market. Recent numbers suggest that housing bottomed out in late 2022 and regained some ground in early 2023 when there was a dip in mortgage interest rates. Potential homebuyers are still uncomfortable with higher borrowing costs where anything above 6 percent on a 30-year fixed rate mortgage feels massive compared to the historic lows in 2021 and 2022. However, the latest data point to lack of supply of existing homes at an affordable price as keeping sales numbers down. If higher rates have cooled the housing market, lack of supply means that those still looking to buy a home are in fierce competition for the more sought-after units.