The May 29 week starts with the Memorial Day observance on Monday when US debt and equity markets are closed. The four-day workweek has a concentration of economic reports related to the labor market. However, unless and until negotiations about raising the federal debt limit come to a successful conclusion with an increase, the data will be secondary. The focus will be on getting a deal in place prior to when the federal government runs out of borrowing room and money to pay its obligations. The exact deadline isn’t known – and may not be for a few days yet. Thursday, June 1 seems to be the working date. At a guess, there will be an 11th hour temporary suspension of the debt limit or small increase that will allow the government to get to the June 15 tax payment due date while negotiations for a more lasting agreement continue.

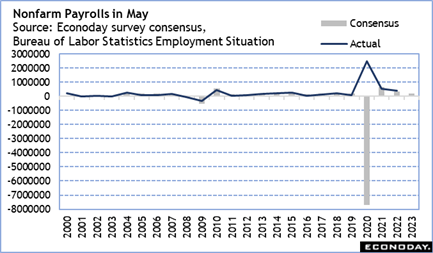

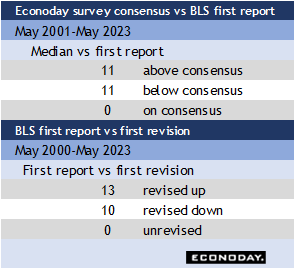

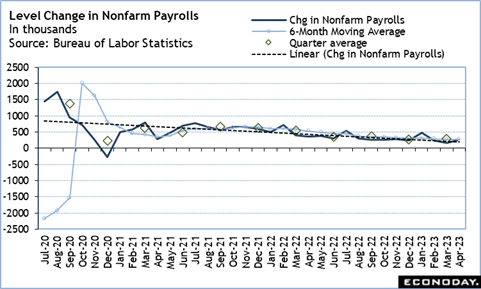

In any case, the highlight of the week is likely to be the employment situation for May at 8:30 ET on Friday. Early forecasts anticipate the unemployment rate to tick up a tenth to 3.5 percent. This remains a very low rate and consistent with a tight labor market. However, the tightness in the labor market is more from employers holding on to current workforces (despite concerns about an economic slowdown) than it is about robust hiring. The early consensus for nonfarm payrolls is roughly for a 175,000 increase. The challenge in forecasting payrolls in May is whether spring graduates are being brought on board before receiving their diplomas, or if actual hiring will wait until June. This is also the time of year when some seasonal businesses, like home and garden centers, add employees before vacation season starts.

Fed policymakers are going to watch the labor market numbers carefully to determine if conditions are strong enough to withstand another rate hike at the June 13-14 FOMC meeting. While there has been some progress on curbing inflation, the FOMC has stressed that the job is far from done. The question is whether the committee’s majority will think that tighter financial conditions are sufficient to do some or all of the work of another rate hike, and/or be willing to wait to see if some of the long and variable lags in the transmission of monetary policy become evident.

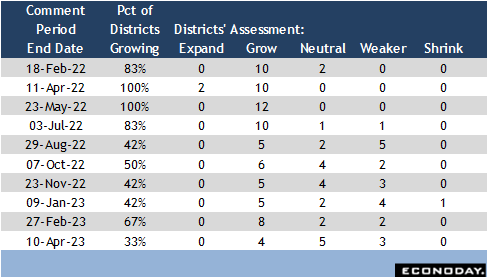

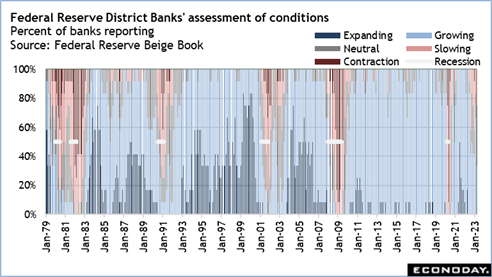

To help in making that assessment, the next Beige Book is at 14:00 ET on Wednesday. The compilation of anecdotal evidence about economic activity across the 12 Districts will help add nuance to what the hard numbers have to say.