The economic data release schedule is crowded in the November 13 week. There are three reports that should stand out, or would if not for a looming government shutdown on November 17.

First is October’s CPI at 8:30 ET on Tuesday. The runup in gasoline prices in the summer months has given way to seven straight weeks of declines from the end of September. This easing should contribute to a resumption of the downward trend for the year-over-year percent change in the all-items CPI. More in question will be if shelter costs continue to ease and if non-housing services are making progress. These latter two components are lagging behind the rapid declines in commodities prices as the FOMC raised rates to cool consumption and bring inflation back to the 2 percent objective.

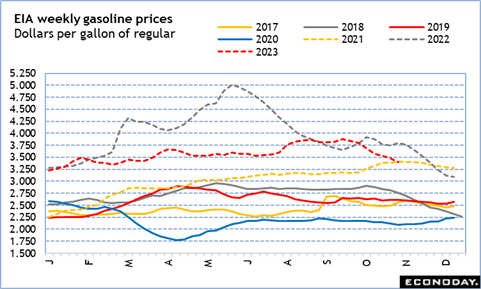

Second is the data on retail and food services sales in October at 8:30 ET on Wednesday. Falling gasoline prices will be a factor here as well. The EIA average price for a gallon of regular gasoline was about $3.89 at the start of October and fell to about $3.47 per gallon at month end. The decline is enough that it will noticeably reduce the dollar value of sales at service stations even if the volume of sales remains the same as the prior month. Sales in the nonstore retailer component should get a boost from the presence of Amazon’s Prime Day – and the competing events of its rivals – in the second week of October. The question here is if consumers decided to do their holiday shopping early and online, and if there is any momentum going into the November/December shopping period.

Third is the NAHB/Wells Fargo housing market index for November at 10:00 ET on Thursday. The index has declined rapidly from a recent high of 56 in July to 40 in October as mortgage rates passed the 7 percent mark. The Freddie Mac rate for a 30-year fixed rate mortgage averaged 6.85 percent in July and has risen from there to an average of 7.65 percent in October. The early weeks of November put the rate a tad lower at 7.63 percent, suggesting hope that the FOMC is done raising rates, but not that these are coming down any time soon. In any case, although homebuilders’ confidence is diminished and may edge down further in early November, the narrow supplies of existing homes means the index is not likely to reach the low of 31 seen in December 2022 when the 30-year fixed-rate was at 6.36 percent. Many qualified and motivated homebuyers are switching to adjustable-rate mortgages to reduce initial monthly payments. All mortgage borrowers are hoping for mortgage rates to decline sufficiently that they can refinance at a lower rate sometime in the not-too-distant future.

One final note: the BLS will release its annual report on the cost of quality adjustments for passenger cars and light trucks in conjunction with its October Final-Demand PPI report at 8:30 ET on Wednesday. It isn’t a market mover, but it is an interesting look at one factor driving prices for motor vehicles.