The November 14 week has a busy data release schedule that could have some good news and some less good news. The three things that markets will be looking for are: 1) the pace of retail sales in October for early indications on the start of the holiday shopping season; 2) whether the PPI and import price index echo the improvement seen in the October CPI numbers; and 3) if the housing market is still sliding downward as mortgage interest rates continue their climb.

It will be retail and food services sales for October at 8:30 ET on Wednesday that will get the most attention, and rightfully so.

Available data – anecdotal and hard numbers – point to a slowing in consumer spending as unconfident consumers have less discretionary income in the current inflation environment. Many retailers and wholesalers tried to get a jump on the holiday shopping season in October. While spending on Halloween merchandise was likely good, that for the upcoming Thanksgiving and Christmas period may not meet the hopes of merchants. Nonetheless, retailers and wholesalers are hiring for their seasonal workforce where they can find applicants.

It looks like spending at brick-and-mortar locations may not have been as good as desired. However, the presence of an Amazon Prime Day around the Columbus Day weekend and Amazon’s online competition may have had a better month. Yet another wave of Covid infections and high gasoline prices may have sent consumers to the internet for both convenience as well as comparison shopping for the best bargain.

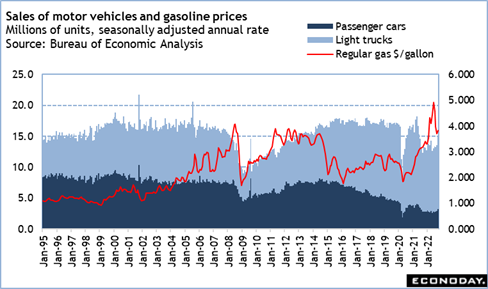

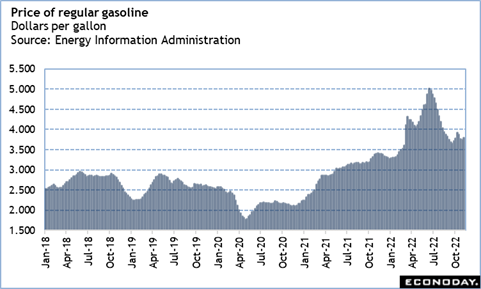

Outside of spending at brick-and-mortar stores, the report will see the influence of changes in gas prices and sales of motor vehicles. Regular gasoline prices averaged around $3.82 per gallon in October, up from $3.70 in September. Higher gasoline prices mean cutbacks in household budgets for other items. Along with higher food prices, this could depress overall sales.

On the other hand, motor vehicle unit sales rose to 14.9 million units at an annual rate in October after 13.6 million units in September. The dollar value of sales should reflect the rise in unit purchases.

Finally, spending on building materials and garden supplies could be good. Homeowners have been consistently investing in home repair and renovation. October is the time of year when homeowners make preparations for the colder months and finish up their outside garden work.

The Econoday consensus forecast for total retail sales is up 1.0 percent in October within a range of up 0.4 to 2.0 percent. I think this is about right after balancing the pluses and minuses going into the report. It will get the fourth quarter of 2022 off to a decent start for personal consumption expenditures.

Expectations are for moderation in the October PPI at 8:30 ET on Tuesday as well as the import and export price indexes for October at 8:30 ET on Wednesday. Some of the easing will be in energy costs, but wider inflationary pressures may be a bit softer.

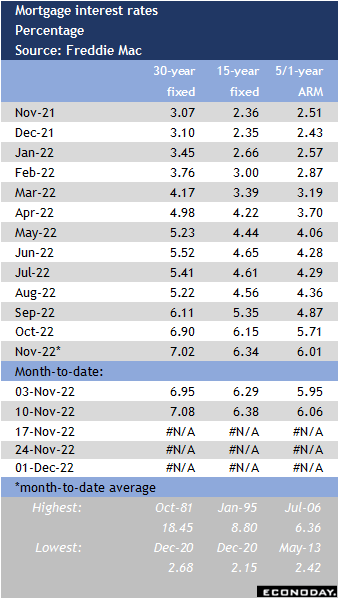

The NAHB/Wells Fargo housing market index for November at 10:00 ET on Wednesday should reflect the ongoing climb in mortgage rates that have decreased home affordability and pushed some homebuyers out of the market despite moderation in prices. Homebuilders have responded by reducing projects and focusing on more entry-level, less expensive units. This is also due to the limited inventories of existing units on the market as current mortgage holders – especially those who bought or refinanced in the last few years – are reluctant to sell even though home values have increased rapidly.