The November 21 week is essentially a 3-day week. The Thanksgiving holiday on Thursday is followed by Black Friday on which many people take off or which businesses offer in exchange for working Veterans Day. There are full market closures on Thursday and early closes on Friday. Additionally, Wednesday is a ½ day for many as they prepare for travel and entertainment. As a result, the data releases – and most of the important ones are scheduled for Wednesday morning – will get only a quick look to ensure there’s nothing that needs a deeper read.

There are two reports that will be released on a different day than usual. The weekly initial jobless claims numbers will be released at 8:30 ET on Wednesday, not Thursday. The final University of Michigan Consumer Sentiment Index is at 10:00 ET on Wednesday, not Friday.

There are probably no market movers among the data on the schedule. Claims will be watched to see if tech layoffs are showing up yet. The consumer sentiment index was a dismal 54.7 in the preliminary report. It would take a substantial upward revision, which is not expected, to meaningfully change that picture. The data that will most likely catch market attention will be the October advance report on durable goods orders at 8:30 ET on Wednesday. The 26 aircraft gain in Boeing commercial orders to 122 in October should help keep the transportation component as a positive contributor, but other sectors may not be doing as well.

The minutes of the November 1-2 FOMC meeting will be released at 14:00 ET on Wednesday. These will be carefully scrutinized for hints of any substantive change in monetary policy. However, the minutes will be three weeks old and not include knowledge of the October reports for the employment situation, the CPI, the PPI, and retail and food services sales. What we should get is a sense that the FOMC is carefully watching the data, hopeful that previous rate hikes (375 basis points since March) will have begun to cut into inflationary pressures and prepared to adjust their actions based on the latest information. There may be a hint of diverging opinions among policymakers about the need and/or size of further rate hikes. For the moment, though, look for unanimity that at least one more hike in December is on the table even if it may be smaller after four 75-basis point increases in a row.

On Friday, with nothing else on the economic data schedule in the U.S., expect a heavy focus on retail activity for Black Friday sales, although many businesses have already begun that promotion more than a week before.

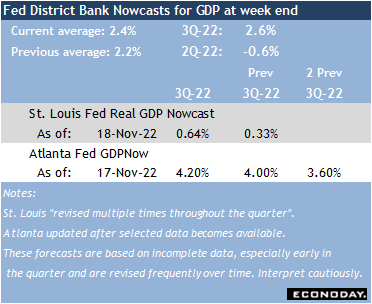

Markets will be watching carefully for any indication that economic growth will hold up during the fourth quarter. The earliest GDP Nowcasts are broadly positive, but could turn in either direction depending on the tone of the data for November and December.