The November 28 week ramps back up to a full schedule as November closes out and December begins. The two standouts are likely to be the release of the Fed’s Beige Book on Wednesday at 14:00 ET and the November Employment Situation at 8:30 ET on Friday.

The next FOMC meeting on December 13-14 is almost universally expected to see another rate hike. The data in the coming week will help shape the size of the hike, and the outlook for future ones. There’s no inflation data, but there is a lot about the labor market.

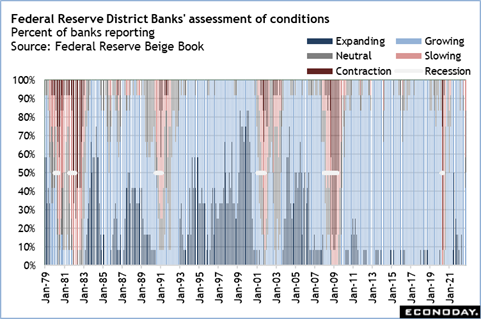

The Beige Book will look at anecdotal evidence about the economy between mid-October and late November. While these are not hard data points, the information is invaluable to Fed policymakers to judge economic current economic conditions and will be considered at the upcoming FOMC meeting. The report will influence the decision on the size of the next rate hike and the outlook for the intermeeting period before the January 31-February 1, 2023 meeting.

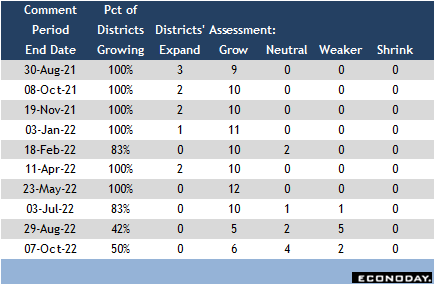

The content of the Beige Book is also an important indicator of when the US economy is slipping into or out of a recession. When less than 60 percent of districts are reporting growth, it is usually a good bet that a recession is on the near horizon or has begun. In the September and October reports, that share was down to 42 percent and 50 percent, respectively. However, no district reported outright contraction, and the economic fundamentals indicated that the labor market was still tight and supporting consumer activity. Much of the decline was attributable to higher interest rates and inflation. For the former, consumers and businesses were adapting. For the latter, there were signs of relief beginning to emerge. So, while growth was negative or sub-par, it wasn’t technically a recession.

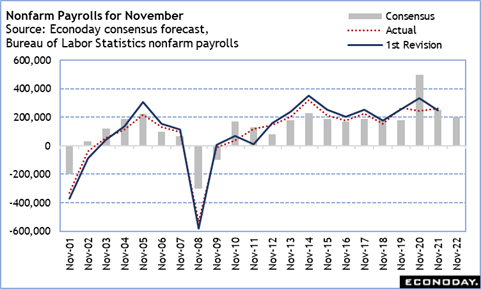

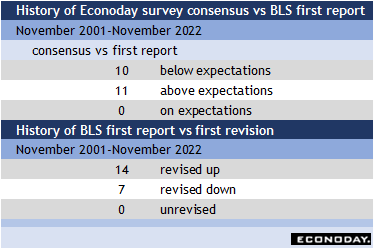

There are a number of labor market reports during the week that should reflect an easing in labor market conditions, from very tight to merely snug. Early estimates are a 200,000 rise for nonfarm payrolls and a 1 tenth uptick in the unemployment rate to 3.8 percent. This would represent a slowing in job gains, though still at a pace consistent with modest economic expansion and suggesting that the worst of the labor shortages are easing. Based on past results, Econoday’s nonfarm consensus is about as likely to come in above expectations as below, with the result subsequently revised higher.

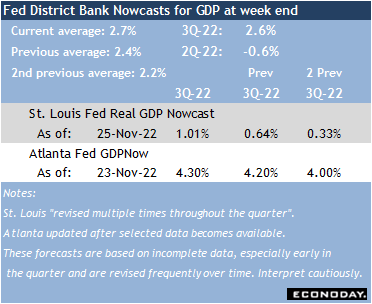

For the moment, at least, the outlook for growth in the fourth quarter looks similar to that in the third quarter. On Wednesday at 8:30 ET the second estimate of third-quarter GDP will be released. Markets will be interested in the result, but given that the fourth quarter is nearly 2/3 gone, unless the revision is significant, it will get only passive notice.