Fed Chair Jerome Powell spent much of his November 1 press briefing hammering on the point that a pause in hiking rates for a second FOMC meeting in a row does not mean that the bank is done raising rates. While it seems increasingly likely that the fed funds target rate range has peaked at 5.25-5.50 percent, Fed policymakers remain data dependent. They will be carefully examining the incoming information in the period between now and the December 12-13 meeting. If inflation isn’t coming down and/or inflation expectations appear in danger of coming unanchored, the FOMC is prepared to hike rates again.

One of the pieces that the FOMC did not have for its deliberations was the October employment report which was released on Friday, November 3. The moderation in payroll growth and small uptick in the unemployment rate owe something to the ongoing strikes by the UAW and SAG-AFTRA. Nonetheless, Fed policymakers should find the numbers consistent with their outlook for the economy and inflation, and markets can be cautiously optimistic that the FOMC is done raising rates.

The economic release calendar for the November 6 week is sparse and has little that has market-moving potential. What may be the big news of the week is if markets accept the hawkish stance of the FOMC in terms of its determination to fight inflation with restrictive monetary policy. That may or may not include another rate hike this year. Given Powell’s comments about the FOMC being careful in setting policy until it has confidence that the inflation fight is won, markets could well reflect an anticipation that restrictive policy will not be eased any time soon.

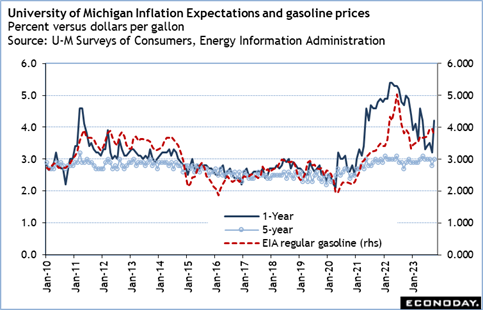

The most interesting report in the November 6 week is likely to be the University of Michigan Consumer Sentiment Index for early November on Friday at 10:00 ET. The final report for October put the index at 63.8 after 67.9 in September. The drop reflected a number of factors including geopolitical events that make the near future look less optimistic. Recent declines in gasoline prices, getting over the initial shock of the war between Israel and Hamas, and the end of the confusion around electing a new House speaker may increase consumer confidence. Also, year-ahead inflation expectations jumped to 4.2 percent in October from 3.2 percent in September, but this reading may decline given moderation in fuel costs. Five-year inflation expectations have been steady right around 2.8-3.0 percent for more than a year. It shouldn’t be much different in November 2023.