There are three foci for the economic data in the October 17 week. These are the housing market, the surveys of manufacturing, and the Fed’s Beige Book. Expectations appear firmly in place for another 75 basis point rate hike at the November 1-2 FOMC meeting. Between the higher-than-expected data on inflation and the rhetoric of Fed policymakers, there’s little doubt that taming inflation will remain the FOMC’s priority. While interest rate-sensitive sectors like housing have responded rapidly to higher rates, upward pressures remain broad and persistent for some goods and most services.

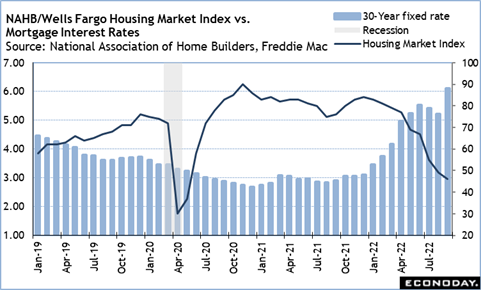

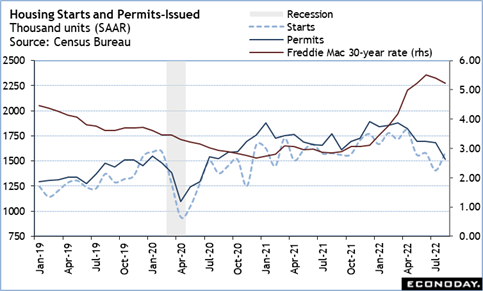

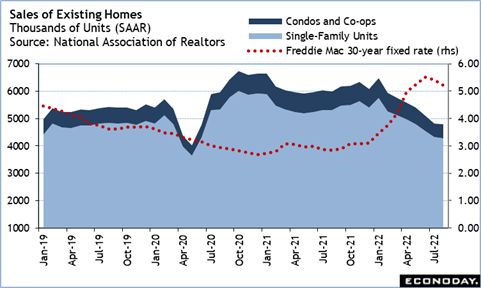

The data relating to the housing market are expected to continue to cool as mortgage rates rise. The NAHB/Wells Fargo housing market index for October at 10:00 ET on Tuesday should reflect even lower demand for new single-family homes. The number of starts of new homes for September at 8:30 ET on Wednesday will likely unwind the surprise increase of 12.2 percent in August, especially as most of that gain was in the volatile multi-unit sector; permits issued for new homes fell 10.0 percent in August and aren’t expected to rebound. Sales of existing homes in September at 10:00 ET on Thursday may not yet show the full effect of higher mortgage rates for those contracts inked in August when rates dipped a bit. It is entirely possible that the Freddie Mac report on mortgage rates on October 20 will see the 30-year fixed rate hit 7 percent, a high not seen in 20 years.

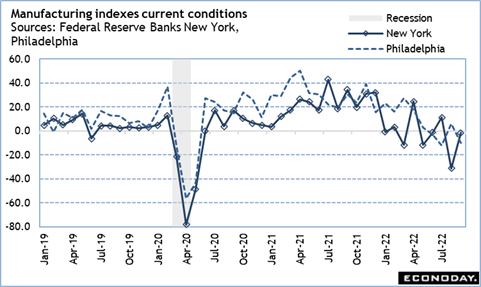

The two earliest surveys for the factory sector are from the New York and Philadelphia Feds. The New York empire state manufacturing survey for October is at 8:30 ET on Monday and the Philadelphia Fed manufacturing business outlook for October is at 8:30 ET on Thursday. Their respective current general business conditions indexes have been volatile in recent months as the factory sector continues to struggle with price inflation, higher wages and unfilled job openings, rising financing costs, a supply chain that has only partially recovered, dollar appreciation, and the increased threat of global recession. The October number for both may erase the mild improvement seen in September.

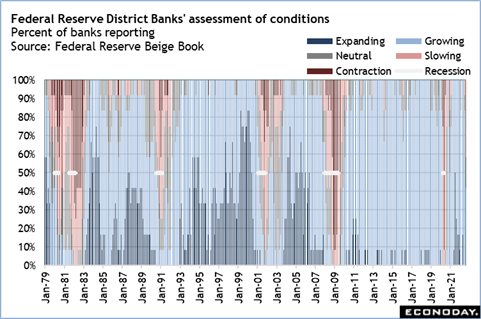

The Fed’s Beige Book at 14:00 ET on Wednesday will provide anecdotal evidence of economic conditions across the 12 District Banks between late August and early October. It could be the best evidence as to whether the US economy has indeed slipped into recession or is hanging on with below-trend growth at the start of the fourth quarter 2022.

Finally, the GDP Nowcasts from the St. Louis and Atlanta Fed’s will be the last pieces of data likely to have a major impact on the forecasts for third quarter GDP in the advance report at 8:30 ET on Thursday, October 27. The average of the two puts growth at around 2.0 percent. Of the two, the Atlanta Fed’s forecast has the better correlation (0.981) as compared to the so-so correlation (0.753) in the St. Louis forecast.