With the prospect of a government shutdown resolved – for now – the economic data calendar does not face any disruptions in the October 2 week. It is a week with plentiful data about the labor market in the US.

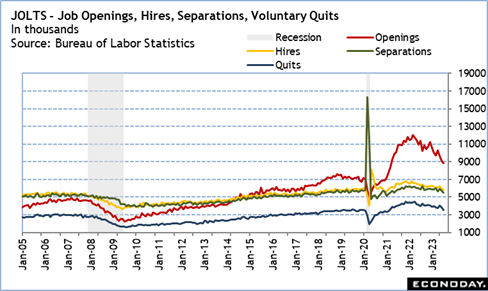

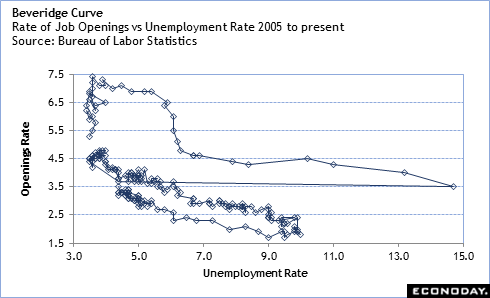

Critical to the outlook for monetary policy is how the cooling in the labor market is shaping up. The reports in the coming week should be consistent with slower hiring, relatively few layoffs, and elimination of unfilled positions. However, a cooler labor market is not a weak one. Conditions are likely to look as nearly normal as they have since the months before the COVID pandemic arrived. This will be most evident in the August report on job openings and labor turnover (JOLTS) at 10:00 ET on Tuesday. In particular, the Beveridge Curve should reflect the intersection of low unemployment rates and moderate numbers of job openings.

The ADP national employment report for September at 8:15 ET on Wednesday should show that private payrolls continue to expand while wage growth remains good but less a source of wage inflation. The Challenger report on layoff activity in September at 7:30 ET on Thursday is expected to reflect modest numbers of layoffs as businesses prepare for an uncertain future. What may be more interesting is if the hiring plans are consistent with anticipation of strong consumer spending over the holiday shopping season against a backdrop of improved labor supply.

Initial jobless claims for the week ended September 30 at 8:30 ET on Thursday will probably remain in line with recent weeks, although strike activity could boost the numbers a bit. Initial jobless claims are not generally affected by strikes initiated by large unions. Union workers usually get a stipend and are ineligible for benefits. It is workers in associated industries who face temporary layoffs unless it is a prolonged strike that causes businesses to shutter and/or workers to decide to seek new employment elsewhere.

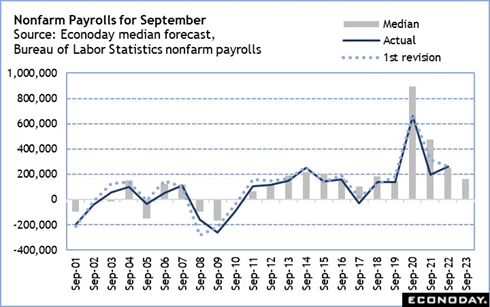

The week’s big report is the September employment situation at 8:30 ET on Friday. At this writing, the Econoday consensus is for an increase of 160,000. This is a solid gain. The September report has a 5 week reference period for the establishment survey ended on September 16. This means that it is likely to include some jobs that might not have been included in the August reference period which ended early in the month on August 12 and may encompass some late hiring for school services.

There’s more than usual strike activity right now, but it should not affect the September numbers too much. The UAW strike started on September 15. Because workers received pay during the reference period, the strike will not affect the count of jobs in the September data. If the strike is resolved before the October 14 end of the survey refence period and the workers are back on payroll, the strike will never show up in the data. The ongoing SAG-AFTRA strike affected the payroll numbers in August and will have no fresh impact for September. If an agreement is reached soon, the 16,000 workers in the motion picture industry will be added back in in the October payroll report on Friday, November 3. There were three smaller strikes settled in September that will bring 5,400 workers back into the payroll numbers.

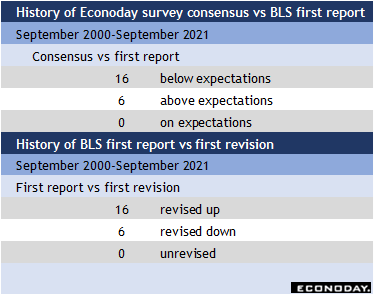

Historically, the September employment numbers strongly tend to come in below forecast, but also strongly tend to subsequently see an upward revision. Should the September change in nonfarm payrolls be a disappointment, it would be well to wait for the next month’s report before concluding that the labor market is softening more than previously thought.