By Theresa Sheehan, Econoday Economist

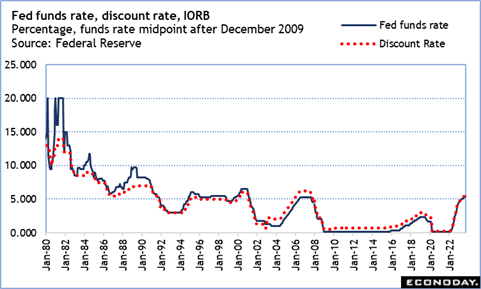

Chair Jerome Powell’s speech before the Economic Club of New York on October 19 was essentially the last word from Fed policymakers on the outlook for the October 31-November 1 FOMC meeting. The communications blackout period around the meeting goes into effect as of midnight on Saturday, October 21 and lasts through midnight on Thursday, November 2. Powell was careful to signal that policymakers remain hawkish in the battle against inflation, but also that they are cautious about future rate moves, especially to the upside. Powell thinks there is still “meaningful” impacts to come from the 525 basis points of rates hikes in the last 18 months. Additionally, a data-dependent Fed is seeing progress in disinflation, ongoing growth above FOMC forecasts, and a labor market that is coming back into balance without a surge in unemployment. Policymakers will take into consideration the possibility of a government shutdown on the horizon after mid-November, increased risks from geopolitical events, and major strike activity in the automotive industry. A pause in the rate hike cycle is likely for the second meeting in a row, but future rate hikes will be on the table.

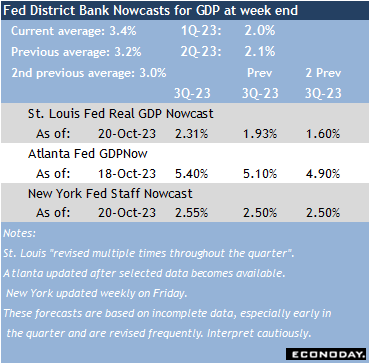

The advance estimate for third quarter GDP is at 8:30 ET on Thursday. The three GDP Nowcasts from the St. Louis, New York, and Atlanta Feds all point to growth above the Fed’s longer-run forecast of up 1.8 percent. Solid consumer spending is anticipated, although rising interest rates will probably put a damper on gross investment.