In the October 24 week, much of the focus will be on the FOMC meeting on November 1-2 in the following week. Fed policymakers will not be making any comments regarding monetary policy this week while the communications blackout period is in effect (midnight Saturday, October 22 through midnight Thursday, October 27). Those who have commented in recent weeks have made it clear that the fight against inflation is ongoing and further rate hikes are expected. The consensus is 75 basis points at the next meeting.

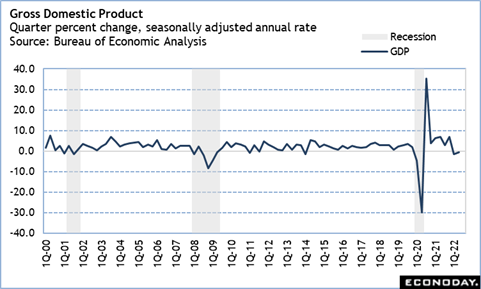

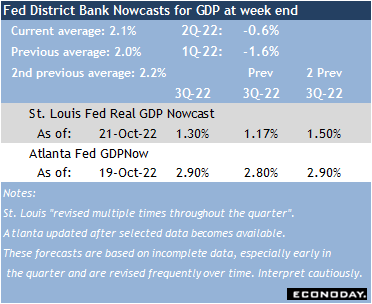

Against this backdrop is the concern that the rapid removal of accommodative monetary policy and the move to restrictive policy will send the U.S. into recession, if it isn’t there already. After two quarters of negative growth, the advance report on third quarter GDP at 8:30 ET on Thursday could decide the question. GDP Nowcasts are pointing to mild expansion of around 2 percent with the Econoday consensus at 2.3 percent. If realized, the economy may have avoided a substantive downturn for the moment.

The earliest data for the fourth quarter suggest this may be a brief respite. Further data for October will be for regional surveys in manufacturing and services. The Philadelphia Fed’s services index is at 8:30 ET on Tuesday, followed by the Richmond Fed surveys of manufacturing and services at 10:00 ET. The Kansas City Fed’s survey of manufacturing is at 11:00 ET on Thursday, and survey of services activity is at 11:00 ET on Friday.

Data for the housing market include the FHFA and Case-Shiller price indexes for August at 9:00 ET on Tuesday, new home sales for September at 10:00 ET on Wednesday, and the NAR pending home sales index at 10:00 ET on Friday. These data are sensitive to rising interest rates and should be in line with other housing reports released recently. Sales of homes are on the decline, elevated prices are giving way to falling demand, consumers are looking for bargains and/or smaller and less expensive homes, and more sales are being closed with adjustable-rate mortgages rather than fixed-rate notes.

The FOMC will get more inflation data at the meeting with the release of the employment cost index for the third quarter and the PCE deflator for September. Both are at 8:30 ET on Friday.

Finally, there are two major monthly reports on consumers’ perceptions of economic conditions in October. The Conference Board’s consumer confidence index is at 10:00 ET on Tuesday, and the final University of Michigan consumer sentiment index is at 10:00 ET on Friday. Consumers are still quite worried about inflation and household budgets and the indexes will reflect that.