Monday, October 9 is a federal holiday to observe Indigenous People’s Day/Columbus Day in the US. However, this holiday is not universally observed. Bond markets are closed in the US, but stock markets are open. Government offices will be closed, but private businesses will mostly be open.

After the big upside surprise in the data on nonfarm payrolls in September, all eyes will be on the September CPI report on Thursday at 8:30 ET, and to a lesser extent the PPI for September at 8:30 ET on Wednesday. With labor markets experiencing good hiring and few layoffs, and early forecasts for third quarter GDP looking for brisk expansion (as of October 5 the Atlanta Fed’s GDPNow is up 4.9 percent for the third quarter), it is the unknowns about inflation that will shape the outlook for Fed monetary policy.

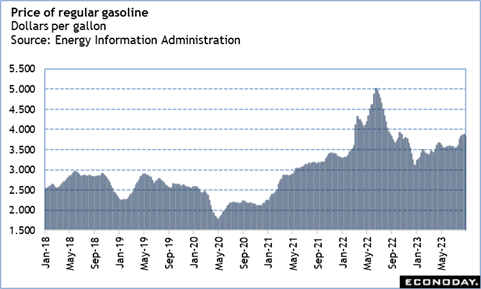

Recent increases in energy costs are likely spilling into underlying inflation, but other inflationary pressures may be easing. September should provide more evidence about the lagged effects of past rate hikes that Fed policymakers have been watching for. If inflation measures reflect more broad-based improvement in inflation, it is possible that the FOMC could extend the pause in rate hikes after the October 31-November 1 deliberations after doing so at the September meeting. However, this does not mean that another hike could not happen this year. There remains the December 12-13 meeting and a few more data points to consider in the intermeeting period.

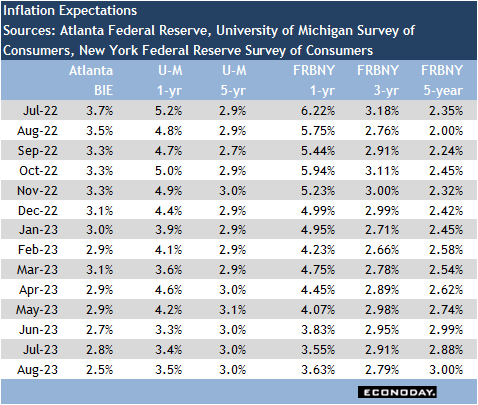

There will also be a look at early September inflation expectations in the Atlanta Fed’s business inflation expectation report at 10:00 ET on Wednesday, the University of Michigan survey of consumers at 10:00 ET on Friday. Recent months have seen some minor ups-and-downs in the numbers, but generally expectations are consistent with inflation coming back toward the Fed’s two target over time, but it may be a longer process than previously thought.