Monday is the 22nd anniversary of the terrorist attacks of September 11. It is not a federal holiday observance on the calendar. Stock and bond markets will be open. However, expect the day to have the tone of solemn remembrance and heightened security alerts.

Fed policymakers will be silent – at least about monetary policy – during the communications blackout period around the September 19-20 FOMC meeting. It will begin at midnight on Saturday, September 9 and run through midnight on Thursday, September 21.

There are two reports on the week’s economic data calendar that have the potential to alter the outlook for the next FOMC meeting.

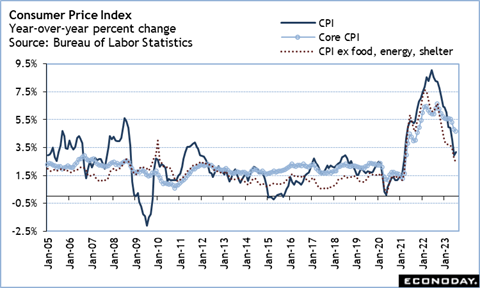

Should the August CPI data at 8:30 ET on Wednesday sound any alarm bells for renewed inflation pressures, it might change the tone of the policy debate. At this writing the data for the economy and labor market suggest that things are developing broadly along the lines that the FOMC has previously forecast. Most analysts are looking for a pause in interest rate hikes at the September FOMC meeting. However, policymakers’ unanimity about bringing persistent inflation down – especially at the core, and narrowly in non-housing services – could shift in favor of another hike sooner rather than later if the data look unfavorable.

The CPI report will also include the August CPI-W index which is used in calculating the cost-of-living adjustment for social security benefits. The final percent change won’t be known until the September data becomes available (end of government’s fiscal year). However, the average of the July and August reports should provide a pretty good idea of what it will look like in in January 2024.

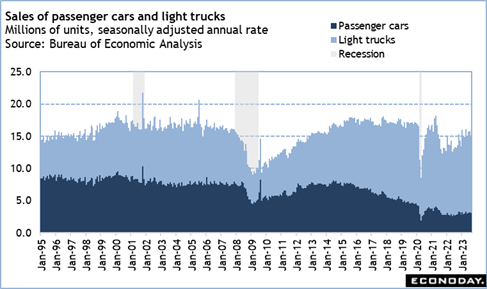

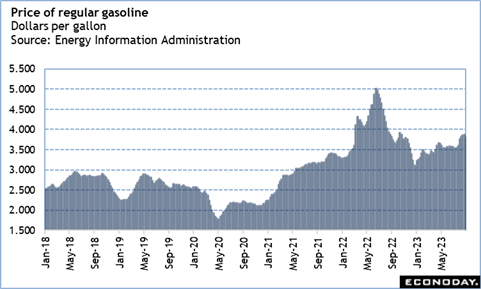

The numbers for retail and food services sales in August at 8:30 ET on Thursday should clarify if consumer spending is going to support third quarter GDP growth and play a part in keeping the US out of a recession. Much will depend on whether consumers were buying back-to-school items, getting a jump on autumn merchandise which was appearing on shelves, and clearing out summer inventories. Unit sales of motor vehicles (previously released) decelerated in August and should bring down the dollar value of total sales. On the other hand, the cost of a gallon of gasoline was up in August, which should contribute to increased dollar value in sales even if vacationers did not drive more.