In the September 12 week, analysts will keep a close watch on the economic data to shape expectations for the September 20-21 FOMC meeting. Fed policymakers will be in their communications blackout period (midnight, September 10 through midnight, September 22). The coming week has the last two reports that are likely to have a noticeable impact as to whether the FOMC settles for a 50 basis point rate hike, goes big with 75 basis points, or even ratchets down to a 25 basis point increase. At the moment, Fed policymakers have enough evidence of a strong labor market that they can continue to focus on price stability. Much will depend on if inflation measures show ongoing improvement and if the pillars of economic growth do not look in danger of falling into recession, or at least not a deep one. In any case, absent a disruptive exogenous event, a rate hike is a near certainty.

The August CPI report at 8:30 ET on Tuesday should get more relief from declines in energy prices. The year-over-year increase was 8.5 percent in July after 9.1 percent in June. However, the core CPI was up 5.9 percent in July compared to a year ago, the same as in June. Consumer prices may have leveled off outside of volatile food and energy costs, but pressure is still elevated and the moderation is not enough to suggest that inflation is improving beyond a few narrow categories.

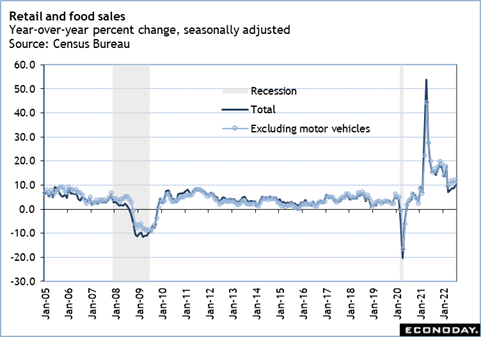

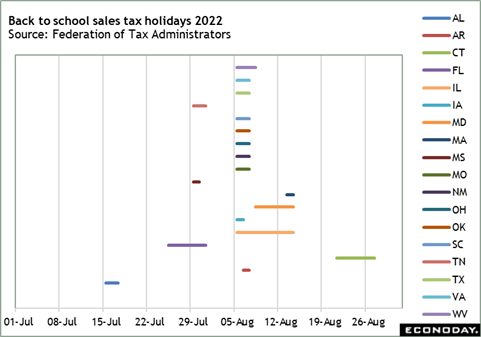

Retail and food services sales for August at 8:30 ET on Thursday won’t get a boost from the sale of motor vehicles and may not be held back by gasoline. Although the price of gasoline may be going down, volumes could be going up. Early August often has a boost in sales of goods related to back-to-school shopping, especially in those states that have a sales tax holiday. With the August and revised July data, the report should give a better idea of the state of consumer spending in the third quarter 2022.

Another couple of reports to keep an eye on are the NIFB small business optimism index at 6:00 ET on Tuesday and the University of Michigan consumer sentiment index at 10:00 ET on Friday. While businesses and consumers may feel some relief at signs of less upward price pressure, worries about a recession are on the rise again. Still, growth in the third quarter 2022 may be in narrow expansion territory after two negative quarters. Fed Chair Powell’s remarks at a Cato Institute event on September 8 indicated that Fed policymakers are expecting a period of below-trend growth until inflation is tamed.

Right now, the FOMC’s longer-run expectation for GDP is up 1.8 percent. This may see an update when the FOMC releases its next Summary of Economic Projections (SEP) on Wednesday, September 21 at 14:00 ET – the same time as the FOMC statement. The SEP has had some unusually large revisions and frequent revisions in the past few quarters.