The US calendar in the September 19 week is dominated by the September 20-21 FOMC meeting. In recent weeks Fed policymakers have been sending strong and consistent signals that taming inflation remains the priority for monetary policy. The persistence of upward price pressures is more worrisome to policymakers than the possibility (however much they don’t want one) of triggering a recession. The saving grace for the economic outlook remains the labor market with its low levels of unemployment, few signs of mass layoff activity, and plentiful job openings waiting to be filled.

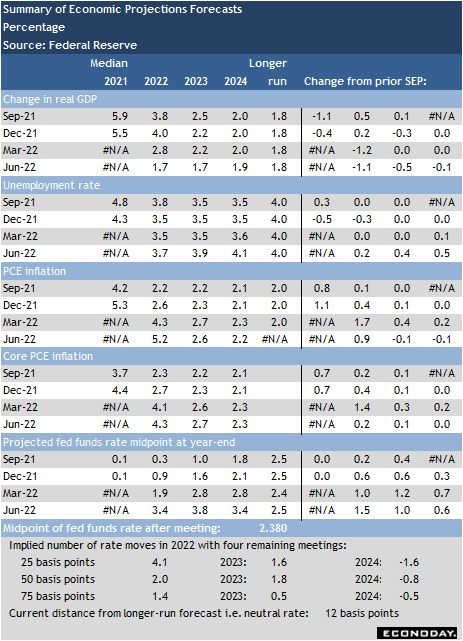

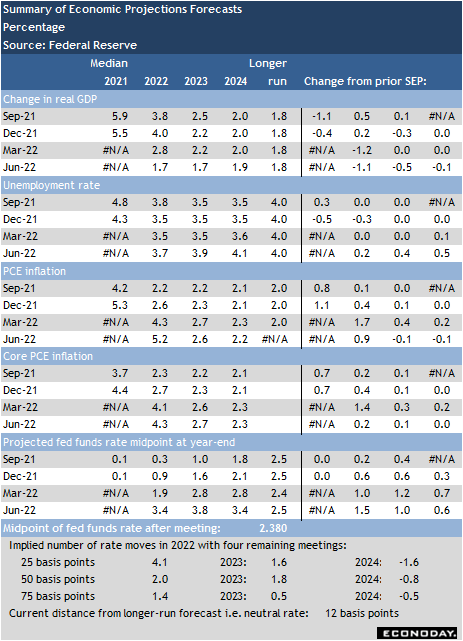

The FOMC statement and quarterly update to the Summary of Economic Projections (SEP) will be released at 2:00 p.m. EDT on Wednesday. The two questions to be answered: how big will the rate be and just how much have their forecasts for growth deteriorated?

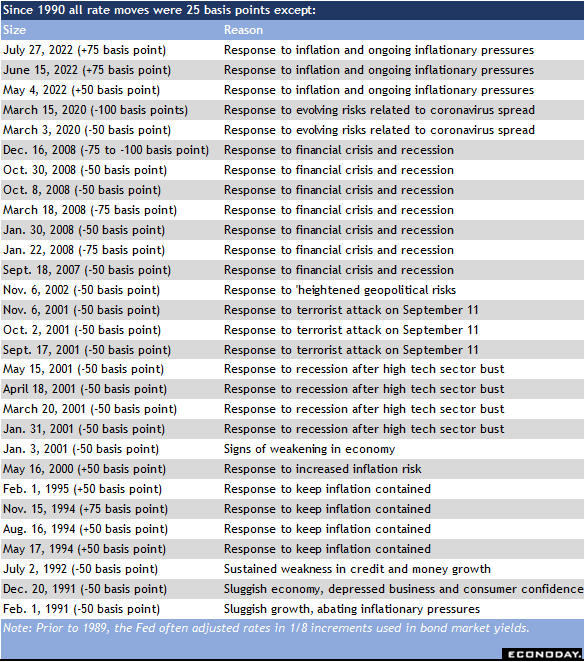

Forecast chatter ranges from 50-100 basis points, with 75 points the strong consensus. It is possible there will be a dissent in the vote this time around. At this stage, policymakers are threading the needle between enough is enough and too much: how much policy withdrawal will be needed to bring down inflation balanced against the risk of causing a recession.

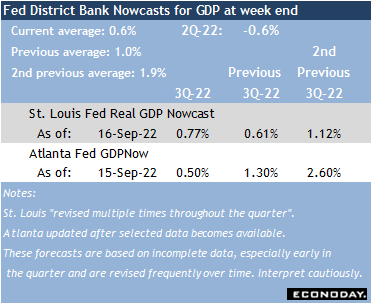

The most recent Beige Book pointed to slowing expansion in many of the Fed’s districts. Taking the anecdotal evidence into account along with moderation in high frequency economic data, the US may indeed be on the cusp of recession. GDP Nowcasts have been revised lower. If the September data soften further, a third consecutive quarter of contraction could be in the cards. The SEP is likely to feature downgrades in expectations for GDP in the last bit of 2022 and into 2023, as well as disappointment in how quickly inflation can be lowered.

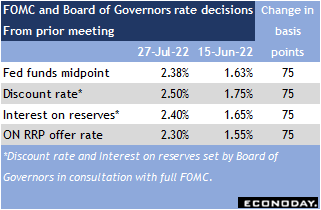

Most FOMC participants would agree that the current fed funds target rate range of 2.25-2.50 percent is around neutral – the June SEP put the longer run rate at 2.4 percent. Policymakers are talking about rates needing to be more restrictive to combat inflation and remaining restrictive for longer than previously thought. The SEP could show that even if rates plateau soon, they may not come down as early as previously forecast.

Whatever the FOMC’s decision, Fed Chair Jerome Powell will face close questioning at his 2:30 press conference on Wednesday. Reporters will ask the whys and wherefores of the decision, what’s in the near term outlook, and just how close the US economy is in fact to recession, if not already in one?