The February 20 week is shortened by the Presidents Day observance on Monday. Stock and bond markets will be closed in the US.

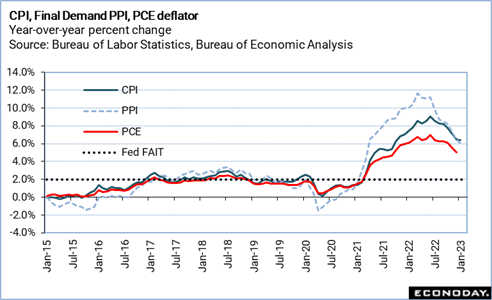

At this writing the dates of Fed Chair Jerome Powell’s semiannual monetary policy testimony have yet to be announced. This brings the minutes of the January 31-February 1 FOMC meeting into greater prominence when they are released at 14:00 ET on Wednesday. This was the last meeting before the winter appearance of the Fed Chair before the Senate Banking Committee and House Financial Services Committee. However, since the last FOMC deliberations the economic data have managed to surprise a few times with an exceptionally strong employment report for January, January consumer prices and producer prices coming in a little above expectations, and retail and food sales turning in a solid performance. Taken together, it indicates that the labor market remains strong for now, consumer spending is supporting the economy, and inflation is far from tamed. That sets the central bank up for further rate hikes in the near term and maintaining restrictive monetary policy for longer. Markets will have to set aside the idea that the Fed is going to lower rates any time soon. The risk of recession remains elevated, although the data show resilience in the face of higher rates. A recession may be avoided as long as people have jobs and/or wages are rising.

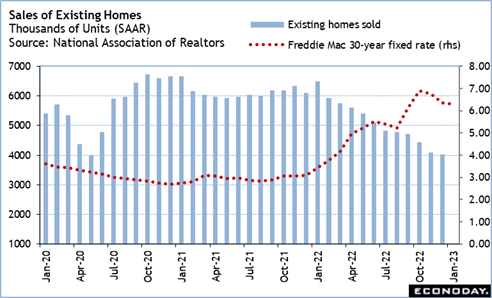

Among the economic data, sales of existing homes in January at 10:00 ET on Tuesday and new single-family home sales at 10:00 ET on Friday that could prove the most interesting. Declines in mortgage rates in December and early January may have sparked some homebuying. Affordability was slightly better and the market favored buyers who could qualify for mortgages. Overall home sales are weaker than a year ago when there was a rush to lock in rates before the Fed pushed rates up enough to seriously affect home affordability. Rates are starting to rise again. As a result, January and early February may be borrowing some sales for the spring months.

The second estimate of fourth quarter 2022 GDP is set for release at 8:30 ET on Thursday. Early forecasts suggest that little revision is expected from the up 2.9 percent in the advance estimate. As the end of February approaches, the first quarter 2023 is nearly 2/3 gone. The GDP Nowcasts tell two different stories. As of February 16, the Atlantia Fed’s GDPNow looks for growth at up 2.5 percent, while the St. Louis Fed Real GDP Nowcast is at down 1.10 percent as of February 17. An average of the two is for growth of up 0.7 percent. It is too early to put too much stock in either forecast with significant amounts of January and early March data yet to be reported.