The two high points of the April 29 week are the FOMC meeting on Tuesday-Wednesday and the April employment report at 8:30 ET on Friday. For the former, no change in the fed funds target rate range of 5.25-5.50 percent is expected. For the latter, the outlook is for ongoing firmness in hiring and low unemployment.

The FOMC meeting statement is scheduled for 14:00 ET on Wednesday and will not be accompanied by an update to the summary of economic projections. With no official update to the FOMC projections due until the June 11-12 deliberations, the FOMC will have to rely on the meeting statement and Chair Jerome Powell’s press briefing at 14:30 ET on Wednesday for any message it wishes to convey.

The statement isn’t likely to see a lot of alteration from the prior version. Fed policymakers will want to say that the US economy is growing modestly and that a slowdown in the expansion is in line with their forecasts. The advance estimate of first quarter GDP at up 1.6 percent after up 3.4 percent in the fourth quarter, with personal consumption expenditures leading the expansion. They may want to tweak the language on inflation now that there is evidence that progress has stalled, but the fundamental approach to monetary policy remains the same. The FOMC will interpret incoming data cautiously and avoid overreacting to what may be short-term movements in the numbers. The committee will make their interpretation in the context of the dual mandate, and carefully assess the risks to the outlook. Policymakers continue to lean toward keeping rates tight as potentially less damaging to the economy than loosening too soon and allowing inflation to become entrenched.

If there is any real news in the FOMC statement and/or Powell’s remarks, it is likely to be in balance sheet policy, not a change in interest rates. Markets have already internalized the notion of no rate cut in June, probably none in September, and maybe not even in December. However, Powell has previously signaled that a change in balance sheet policy could be soon. In past episodes related to managing the balance sheet, the FOMC has prepared the way well in advance so markets could be ready. The minutes of the March 19-20 meeting suggest that the FOMC was close to a decision. The timing of an announcement now would be about right to begin adjusting the program in June. Coincidently but not meaningfully this could occur around the second anniversary of when the program to reduce the Fed’s reserve holdings of US treasuries and agency MBS began in June 2022.

The FOMC won’t have Friday’s employment data for April to consider when it meets. However, there are plenty of other labor market data to suggest that there has been no widespread deterioration in conditions. Hiring may have slowed, but it is far from sluggish. Layoff activity is modest and not accelerating. The rebalancing of labor market supply and demand continues to improve.

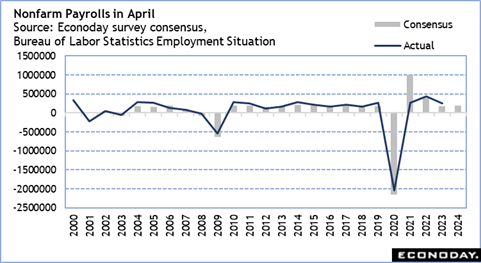

Econoday’s forecast for the change in nonfarm payrolls in April is a rise of 225 ,000. This sort of gain is consistent with a healthy labor market well able to absorb those unemployed or just entering the workforce. However, it is notable that the April nonfarm payroll change has a strong tendency to come in below market expectations and also to be subsequently revised down. Whatever the month-over-month change in April, it will need to be considered in the context of the revisions to the prior two months. March saw an increase of 303,000 and February was up 270,000. The average monthly gain for the first quarter 2024 was 276,000. It is probable that April will not nearly match that pace at the start of the second quarter.

The only special factor that might have an impact on the April employment data is the variable timing of the Easter observance and spring-break periods for educational staffing. The early Easter on March 31 means that many schools timed spring break with the holiday. Schools likely laid off support staff for a week or so, and some businesses may have brought on some temporary staff to accommodate the heavy travel period. However, since this occurred between the end of the establishment survey reference periods of March 16 and April 13, the effect should be minimal.