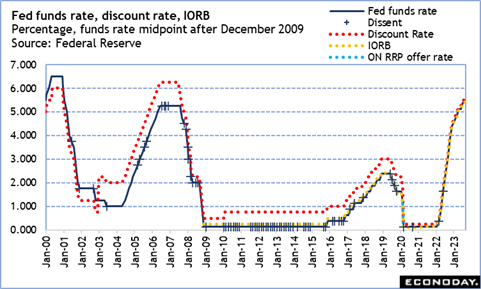

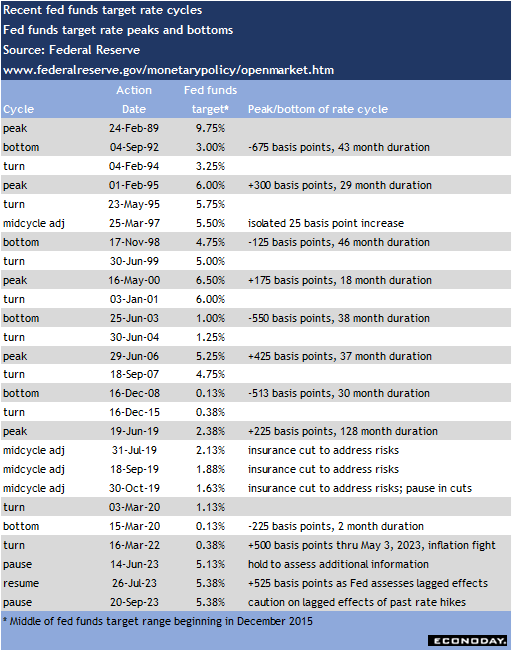

Attention In the December 11 week will be narrowly focused on the rate announcement out of the December 12-13 FOMC meeting at 14:00 ET on Wednesday, along with the quarterly update to the summary of economic projections (SEP). It is widely anticipated that the FOMC will hold the fed funds target rate at its current range of 5.25-to-5.50 percent. What is hoped for is a hint that the FOMC is inclined to let up on restrictive monetary policy sooner than previously thought. What is likely is that the FOMC statement will give no indication that members remain anything but cautious and hawkish in outlook. If they are willing to wait and see the impact of past rate hikes on the economy and financial conditions, they will pointedly reiterate their data-dependent stance.

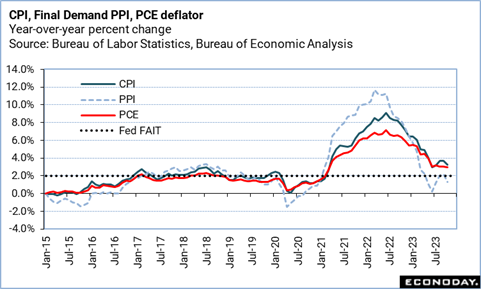

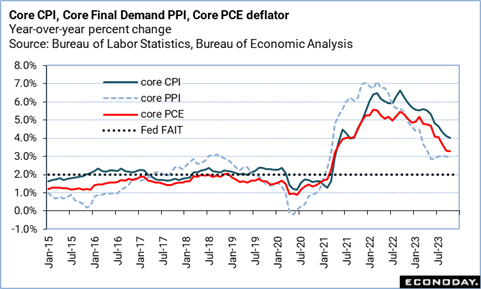

When Chair Jerome Powell gives his press briefing on Wednesday at 14:30 ET, he will elaborate these points, but the underlying message should remain the same. Fed policymakers may diverge somewhat in their outlook for rates, but unanimity prevails when it comes to looking for sustained evidence that the pace of inflation is moderating significantly — particularly at the core. The FOMC is working to return inflation to the Fed’s 2 percent objective and then staying within the bounds of the flexible average inflation target, and inflation isn’t there yet. The FOMC can be fairly confident that the maximum employment side of its dual mandate is being achieved without undo harm to the labor market. Inflation expectations are also cooperating in terms of remaining anchored and consistent with the credibility of the FOMC in its inflation fight. What remains is the performance of the major inflation measures like the CPI and PCE deflator.

In any case, between the SEP and Powell’s remarks, financial markets should gain some clarity about the rate outlook, even if it is not to the markets’ taste.

Fed policymakers will always say that no decision is made in advance of the meeting. The only critical piece of economic data expected before the decision is the November CPI at 8:30 ET on Tuesday. Early forecasts are centering around no change month-over-month for the all-items CPI and up 0.2 percent for the CPI excluding food and energy. If these are at or near the actual month-over-month percent changes, it will make no change in the fed funds rate a near certainty. However, with year-over-year all-items CPI percent change north of 3 percent and core CPI of around 4 percent, Fed policymakers will see some distance to go before lowering rates is dictated by the dual mandate.

Data on retail and food services spending in November will be posted on Thursday at 8:30 ET, after the FOMC meeting concludes. Policymakers won’t have this number as part of the deliberations. Softer motor vehicle sales and falling gasoline prices are probably going to cut into the total dollar value of sales, but it is possible that November could reflect a good performance for consumer spending elsewhere as they shopped and got out around the start of the winter holidays.