The FOMC meeting of January 30-31 concluded with no change in rates and a hawkishly optimistic outlook for the dual mandate as well as good progress on price stability and a tight labor market, but greater confidence needed before a rate cut. The big upside surprise in the January employment report offers another dimension to the outlook for monetary policy. Will the FOMC have an incentive to keep rates higher for longer in order to ensure the economy doesn’t get too warm since the labor market is not cooling as forecast? There is a lot of significant data on the calendar between now and the March 19-20 meeting. The picture could change fundamentally by then. For the moment, the economic outlook is broadly positive.

There is almost nothing on the data calendar in the February 5 week that will affect that. Almost nothing.

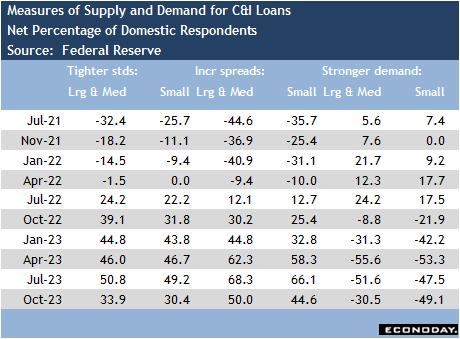

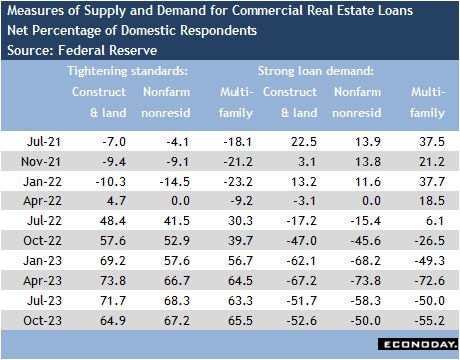

The Fed recently announced that its bank term funding program would cease issuing new loans as planned on March 11 and that the discount window would take up the slack if banks experience liquidity problems after that. This strongly suggests that Fed policymakers view the conditions that led to the collapse of Silicon Valley Bank in March 2023 are now considered as handled in terms of supervision and regulation. At the last FOMC meeting, policymakers got a look at the January Senior Loan Officer Opinion Survey of Bank Lending. It will be released to the public at 14:00 ET on Monday, February 5. The survey provides a lot of information about banks’ standards and terms for lending, and how much borrowing demand is present from both businesses and households. Of particular concern is conditions in the commercial real estate sector that fared poorly during the pandemic and afterward with changes in how much office space businesses need and due to the contraction in brick-and-mortar retail activity. The survey could include some special questions on this topic or other fundamentals in the credit market at most restrictive monetary policy in 18 years.

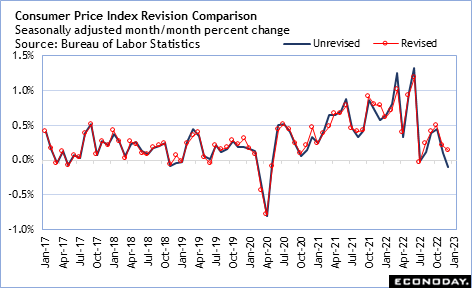

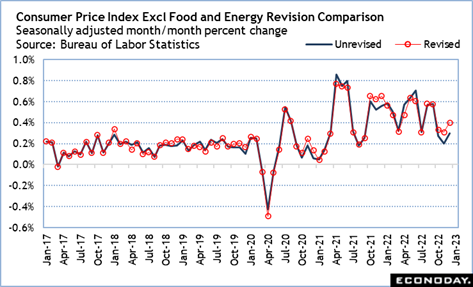

On Friday, the Bureau of Labor Statistics will release the annual revisions to the CPI which can include up to five years of revisions to the seasonally adjusted indexes. Normally the revisions are small and do not impact the underlying picture of consumer price changes, though the data released in February 2022 presented an unpleasant surprise with significant upward revisions that helped keep the FOMC on the path of tightening monetary policy. The revisions will be watched closely to see if there is a surprise in this year’s data as well – whether to the up or downside – which might affect the tone of forecasts in the FOMC summary of economic projections which will be updated at the March 19-20 meeting.