The communications blackout period around the March 19-20 FOMC meeting goes into effect at midnight on Saturday, March 9 and runs through midnight on Thursday, March 21. Fed speakers will be absent from the public engagement calendar in the March 11 week. Markets will have to rely on any comments made by Fed policymakers in the prior week and will give extra weight to Chair Jerome Powell’s comments at the two-day semiannual monetary policy testimony on March 6 and 7.

The bottom line on Powell’s testimony is that the FOMC remains optimistic about the prospect for inflation sustainably returning to the Fed’s 2 percent flexible average inflation target. He said that policymakers have “some confidence” that this is happening but want “greater certainty” before cutting rates. On the other hand, the labor market remains relatively tight in an economy where growth has been surprising to the upside against the backdrop of the most restrictive monetary policy since September 2007. The rebalancing taking place in the labor supply and demand is proceeding without much effect on the unemployment rate which has remained below 4 percent for two years. Fed policymakers won’t make the mistake of calling this a soft landing until they are certain, although the economy does seem to be normalizing from the effects of the pandemic and resulting injection of massive stimulus.

In this context, there are two reports in the coming week that could have some impact on the FOMC deliberations in the following week.

The February CPI report at 8:30 ET on Tuesday is expected to further dampen hopes of a rate cut sooner rather than later, although it won’t entirely rule out that possibility. Consumer prices in February should reflect recent increases in food and energy costs, although this may be a short-term rise. Outside of food and energy, shelter costs will still be elevated, and other services like insurance costs have been facing premium hikes.

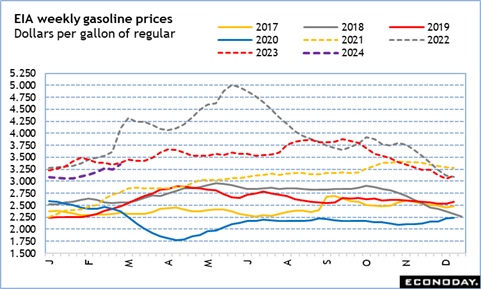

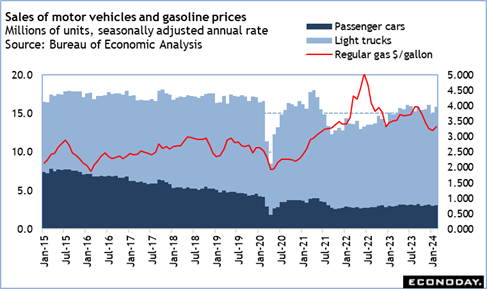

The February numbers for retail and food services sales at 8:30 ET on Thursday could rebound from the decrease of 0.8 percent in January. Although post-holiday shopping fell in January, February could see some renewed consumer spending. Certainly, the quickening pace of motor vehicle sales at 15.8 million units in February after 14.9 million units in January should provide a boost. Rising gasoline prices in February could also contribute to the dollar value of sales, although increases in gas prices are typical at this time of year and this may be muted by seasonal adjustments. Consumers may have a little more to spend as tax funds began arriving by mid-February. The varied weather picture across the US could mean that some areas saw last-minute demand for winter merchandise where others will be getting a head start on outdoor activities like gardening and home repair.

If consumer price inflation improvements are on hold in February, and consumer spending looks to be firming as the first quarter progresses, Fed policymakers will have challenges in balancing the risks in preparing their forecasts for the update to the summary of economic projections (SEP) that will take place at the March FOMC meeting.