Few data reports are likely to be market movers in the March 25 week. Some of the data will close out early looks at conditions for the manufacturing and service sectors in the first quarter 2024. Some will take the temperature of consumers’ optimism – or pessimism – for March and hint at whether consumer spending could support growth in the first quarter. Some will only provide data for February for an incomplete picture of the housing sector in the first quarter.

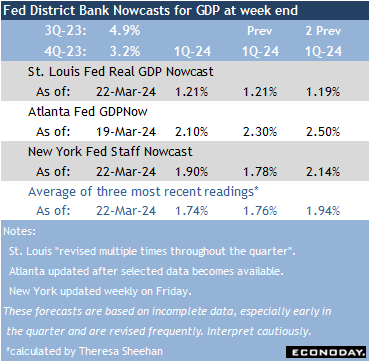

GDP data set for release at 8:30 ET on Thursday will be the third and final estimate of growth for the fourth quarter 2024. We won’t get the advance estimate for the first quarter 2024 until Thursday, April 25 at 8:30 ET. There shouldn’t be much in the way of substantial revisions for the fourth quarter where GDP growth was pegged at 3.2 percent in the second estimate. Early estimates for first quarter growth suggest another positive quarter at around the Fed’s longer-run forecast of 1.8 percent.

The release of the PCE deflator for February in the report on personal income and spending at 8:30 ET will be Friday’s highlight. It would not be a surprise if the index came in above the 2.4 percent year-over-year reported for January, or the core index about the 2.8 percent in the prior report. While the PCE deflator is the Fed’s preferred measure of inflation, the readings of the past couple of months are not enough to inspire the “greater confidence” policymakers want before easing monetary policy by lowering rates. Overall, Fed officials would rather stay the course a little too long than loosen policy too soon and risk a return to higher inflation.