While expectations are universal that the FOMC will remain on hold with interest rates at the April 30-May 1 meeting, there is a good possibility that it will elect to make an announcement about a change in balance sheet policy. At his March 20 press conference, Chair Jerome Powell signaled that the FOMC was prepared to adjust the pace of reductions in balance sheet reinvestment to slow the shrinking of the Fed’s holdings of US treasuries and agency mortgage-backed securities.

The intent is first to achieve a smoother transition for markets to avoid liquidity problems for money markets and to bring reserves down from a level that is “abundant” to one that is “ample”. The FOMC would like an ample reserve environment that is more like the pre-pandemic period, although the ultimate level of reserve holdings will be higher. Powell said, “It’s sort of ironic that, by going slower, you can get farther,” by reducing risks and reaching an “easy landing” in which “nonreserve liabilities grow organically, like currency” and balance sheet run off occurs and “you can effectively hold the balance sheet constant and allow nonreserve liabilities to expand.”

Adjusting the program begun in June 2022 is also a way to start moving the holdings back to an all-Treasuries composition, another explicit goal of the FOMC that is being taken into account.

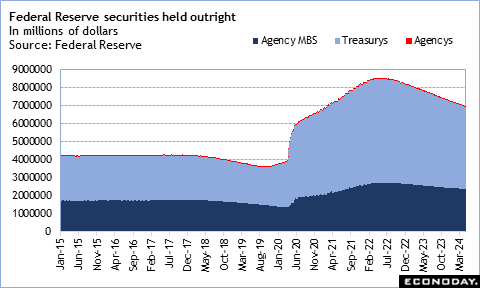

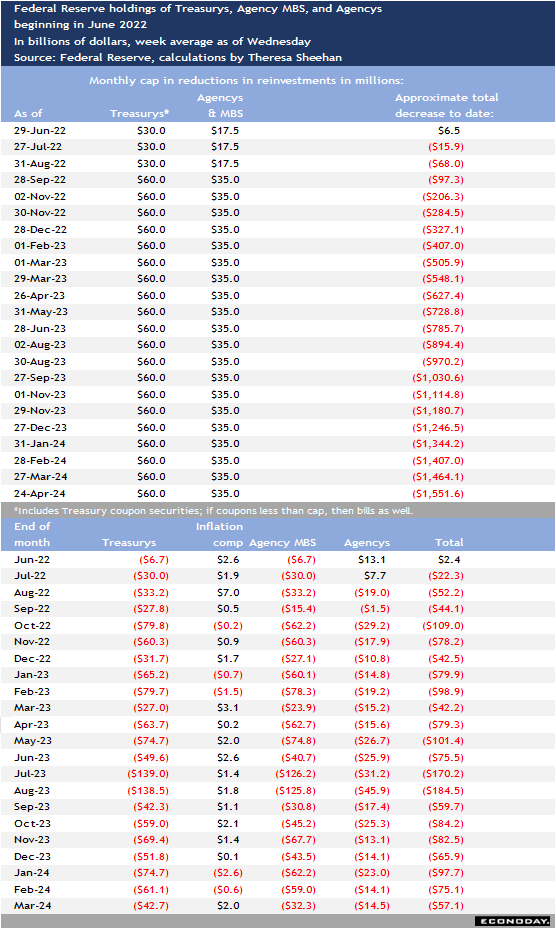

The minutes of the March 19-20 meeting included various considerations for slowing the pace of reducing the balance sheet. At the time of that meeting, the Fed’s holdings of US treasuries and agency MBS were down just under $1.5 trillion and are now about $1.55 trillion. In the past, Powell has called the pace of reductions “brisk”. The minutes said, “In light of the ongoing sizable decline in the balance sheet, and the prospect of a more rapid decline in reserve balances, participants agreed that their discussions at this meeting would help inform the Committee’s future decisions regarding how and when to slow the pace of runoff.”

There was no decision made at the time, but FOMC participants reviewed the experience of the 2017-2019 balance sheet reduction. The minutes said, “The vast majority of participants thus judged it would be prudent to begin slowing the pace of runoff fairly soon.” It would appear that there is little opposition to getting started. The argument is that a slower runoff would be prudent to allow the FOMC to assess the impact and give markets time to adjust to lower levels of reserve. However, “The decision to slow the pace of runoff does not mean that the balance sheet will ultimately shrink by less than it would otherwise. Rather, a slower pace of runoff would facilitate ongoing declines in securities holdings consistent with reaching ample reserves.”

All participants agreed on the importance of clearly communicating that this would not be a monetary policy decision or change in the FOMC’s stance on interest rate policy. It is strictly intended to manage reserves in a way that addresses market stresses.

A few FOMC participants continue to keep the current monthly reinvestment caps of $60.0 billion for US treasuries and $35.0 billion for agency MBS. This hints there could be a dissent in any vote on implementing a change in balance sheet policy, but not enough to prevent it should the majority decide to go forward.

The FOMC minutes gave a good indication of the shape of any changes in the current policy. The minutes said, “[P]articipants generally favored reducing the monthly pace of runoff by roughly half from the recent pace”. This does not mean that the size of the monthly caps for US treasuries and agency MBS could be cut equally. The minutes said, “With redemptions of agency debt and agency mortgage-backed securities (MBS) expected to continue to run well below the current monthly cap, participants saw little need to adjust this cap, which also would be consistent with the Committee’s intention to hold primarily Treasury securities in the longer run. Accordingly, participants generally preferred to maintain the existing cap on agency MBS and adjust the redemption cap on U.S. Treasury securities to slow the pace of balance sheet runoff.”

Half of the current total caps is $47.5 billion. It is unlikely that the FOMC would immediately implement a program that left the cap for agency MBS at $35.0 billion and brought the cap for US treasuries down to a mere $12.5 billion from $60.0 billion. Since the FOMC has indicated it will proceed with caution, most probable is a program of carefully gauged increments in the US treasuries cap over several quarters to allow markets to prepare for the long term. Based on past experience, increments of perhaps $10-$15 billion might be a comfortable choice.