Little is expected from Thursday’s ECB announcement. Key interest rates are widely expected to be lowered over the course of the year but analysts see at most only a very slim chance of any move until there has been further evidence that underlying inflation is under control. Accordingly, the deposit rate (still the main benchmark rate due to the ongoing abundance of excess liquidity) is widely seen being left at the current 4.0 percent record high while the refi rate remains at 4.50 percent and the rate on the marginal lending facility at 4.75 percent.

However, the overall policy stance will continue to be tightened via QT. Net sales from the asset purchase programme (APP) were just over €9.0 billion in December, boosting cumulative disposals since last February (when partial reinvestment was introduced) to around €226 billion and leaving holdings at €3.03 trillion, their lowest level since the middle of 2021.

As it is, QT is set to become rather more restrictive over the second half of 2024. Last month the central bank indicated that the reinvestment of maturing assets acquired under the pandemic emergency purchase programme (PEPP) would be phased out by the end of the year. From July, the ECB has set itself an average monthly target of €7.5 billion for net sales through December. On the basis of average APP sales since last July, this would boost the overall liquidity withdrawal by almost 30 percent per month. The expiration of the final targeted longer-term refinancing operations (TLTRO-III) will also drain a further €490 billion or so in 2024.

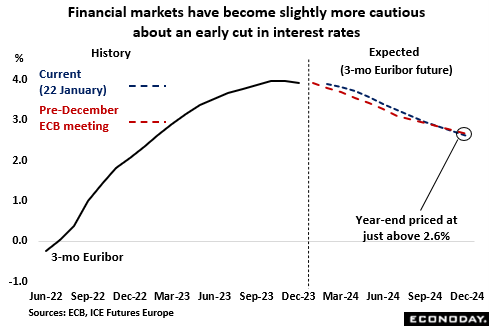

Following its December meeting, the ECB issued a battery of comments aimed at tempering speculation about prospective interest rate cuts in 2024. Financial markets have taken this on board but remain convinced that the first reduction is just a matter of time. A 25 basis point ease is fully priced in for early spring and by the end of this year, 3-month Euribor is seen at around 2.60 percent, a level almost certainly viewed as too low by the central bank unless inflation slows more quickly than anticipated.

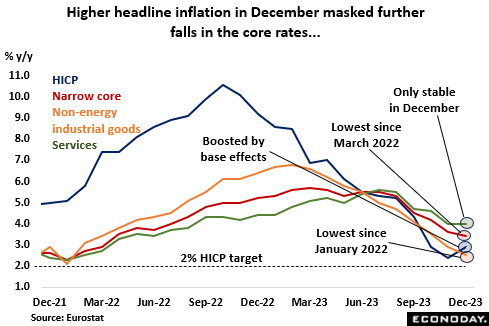

The December inflation data were mixed but that will have come as no surprise to the ECB and, crucially, the underlying picture continued to improve. At 2.9 percent, the headline rate was up 0.5 percentage points versus November but this essentially just reflected an unusual fall in prices a year ago. More importantly, the narrow core rate fell again, easing from 3.6 percent to 3.4 percent and its lowest mark since March 2022. Still, the Governing Council (GC) hawks will point to services where inflation only held steady at an unacceptably high 4.0 percent, double the target level. There will be increasing focus on this sector over coming months.

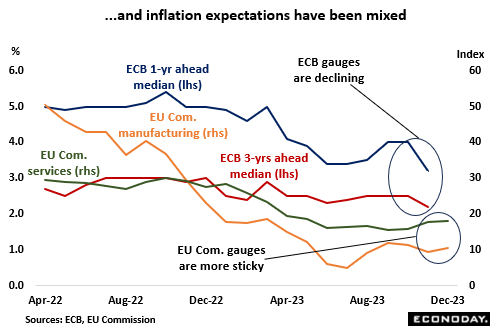

The bank pays a lot of attention to inflation expectations and here the news has been similarly mixed. According to the ECB’s own survey, household expectations for both 1-year ahead and 3-years ahead fell quite sharply in November; the former sliding from 4.0 percent to 3.2 percent and the latter from 2.5 percent to 2.2 percent. However, by contrast, the EU Commission’s wider ranging report found expected selling prices in December rising for a third straight month in services and for the third time in the last four months in manufacturing. Household expectations have also climbed well above last July’s low. Outside of services, the latest readings are not historically high but, with the Eurozone jobless rate (6.4 percent) currently matching its record low, the rises come at a time when around 40 percent of European workers will be entering 2024 wage negotiations. The outcome here will be a key input into the ECB’s future interest rate decisions.

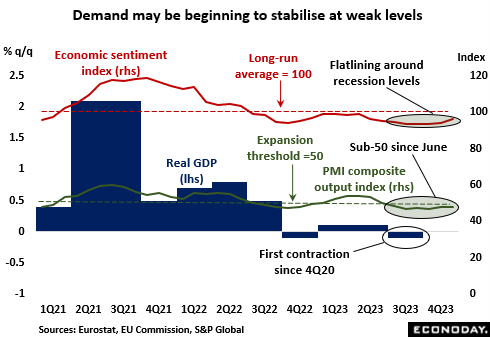

Confirmation of what is likely to have been a recession at the end of 2023 will have to wait for the preliminary flash fourth quarter GDP data due next week. However, even if the Eurozone managed to avoid a second successive contraction, the economy is clearly doing little more than flatlining. As of November, fourth quarter retail sales volumes were on course to post an eighth straight decline. November goods production dropped to its weakest level since October 2020, December’s services PMI (48.8) was below the 50-expansion threshold for a fifth successive month and exports have subtracted from growth every quarter so far in 2023. There have been some tentative signs that the fall in demand is beginning to tail off but there has been little in the data to offer any hope of a meaningful pick-up in activity over the first half of the year.

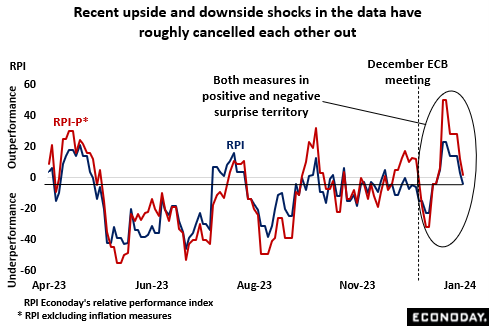

Even so, while the economic data released since the December ECB meeting have been generally weak, versus expectations surprises on the downside have been essentially matched by shocks on the upside. Indeed, at the time of writing, Econoday’s relative performance index (RPI) stands at minus 4 and its inflation-adjusted counterpart (RPI-P) at 2, both readings very close to zero. Consequently, at least in broad terms, the central bank’s view of the region’s economy is unlikely to have changed much. In itself, this suggests that the Governing Council (GC) is all the more likely to be content with the current policy stance.

In fact, at this stage, it seems unlikely that even a mild recession would force the ECB’s hand on interest rates. The bank must be cautiously happy with recent HICP reports but it knows that there is still some way to go before the core rate reaches 2 percent. It will also want to see at least some results from the current wage round while at the same time being alert to the potentially inflationary threat from escalating geopolitical instability, notably in the Middle East. Indeed, just last week Robert Holzmann, possibly the GC’s most hawkish member, even warned investors not to take lower interest rates in 2024 for granted. Accordingly, the best bet for Thursday’s announcement is probably a broadly unchanged policy statement accompanied by some rhetoric that reminds financial markets that the job is not yet done.