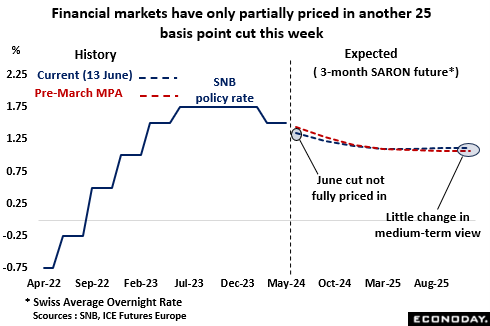

The SNB surprised financial markets with a 25 basis point cut in its policy rate to 1.50 percent in March so investors are all the more cautious going into this quarter’s Monetary Policy Assessment (MPA). In favour of another ease is inflation, which has remained well below 2 percent. Importantly too, earlier losses by the Swiss franc have recently been largely reversed. However, against that, price rises have accelerated since March and the economy has continued to grow at a modest pace. As a result, forecasters are quite evenly split between no change and a second successive 25 basis point reduction on Thursday.

On the whole, medium-term interest rate expectations in financial markets have changed little since the March cut. A 25 basis point ease is still not fully priced in for this month and at 1.15 percent, the year-end call is almost identical to that just before the last MPA. Indeed, rates are now seen only a few basis points firmer at 1.12 percent by December 2025. In contrast to many other central banks, there is only limited room for additional SNB easing even with inflation so low.

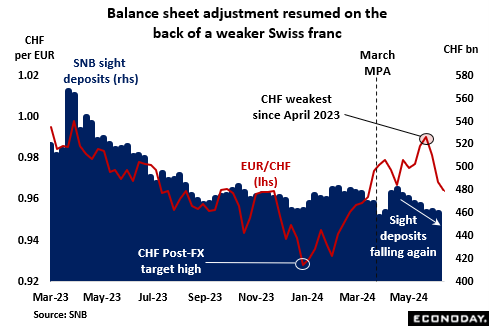

Meantime, the strength of the franc at the start of the year effectively curtailed the SNB’s efforts to shrink its balance sheet during the first quarter of the year. However, the subsequent slide in the unit meant that the bank was subsequently able to resume its asset sales programme and sight deposits have now fallen nearly CHF300 billion since September 2022. Still, the depreciation at one point was fast enough to prompt SNB Chief Thomas Jordan to say that the bank saw a small upside risk to its inflation forecast due to exchange rate weakness and warned that it might be forced to intervene and sell foreign exchange. His comments triggered a partial reversal and at EUR/CHF0.9663, the cross-rate is probably close to where the bank would like to see it. Even so, FX developments so far in 2024 underline the sensitivity of the SNB to exchange rate volatility in either direction.

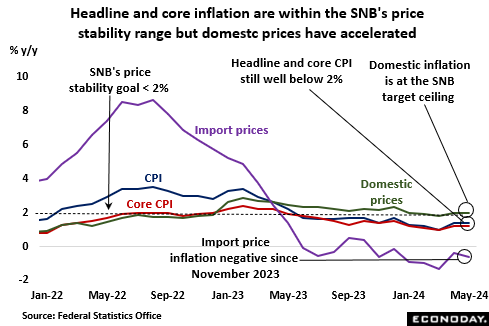

By international standards, inflation in Switzerland remains very low, not that that will be of any great interest to the SNB which is much more focused on domestic conditions. The May CPI report was generally favourable but still slightly mixed. The headline rate was stable at just 1.4 percent but still well above March’s 1.0 percent low. Much the same applied to the core measure which held steady at 1.2 percent, also a couple of ticks above its recent low. However, domestic prices were still rising at a 2.0 percent rate, at the top end of the bank’s definition of price stability. Moreover, private sector services were even higher at 2.2 percent.

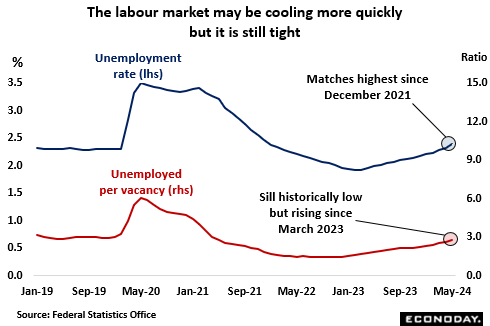

However, the labour market has shown signs of cooling more quickly than earlier in the year. Hence, the number of people out of work was up 2.1 percent in May, one of the steepest monthly increases seen since unemployment began rising back in March last year. At 2.3 percent, the unemployment rate matched its highest level since the end of 2021 while the unemployment/vacancy ratio climbed to its highest mark since April that year. That said, both measures remain well below their long-run average, indicating that overall conditions remain tight.

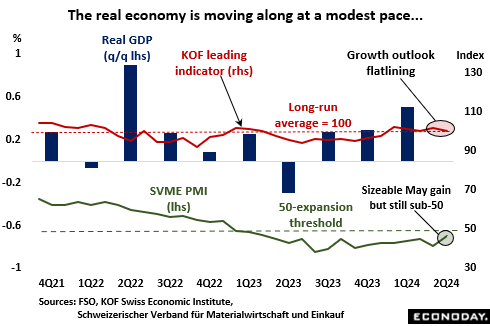

First quarter growth edged up a couple of ticks to a 0.5 percent quarterly rate, its best performance since the second quarter of 2022. However, final domestic demand rose a more modest 0.4 percent and business inventories (including statistical discrepancies) added fully 2.1 percentage points, potentially making for downside risk to the current period. Even so, by and large, the economy looks likely to expand at a modest, albeit probably slightly sub-par, pace over coming quarters with rising unemployment keeping a check on household spending and manufacturing struggling to move out of recession.

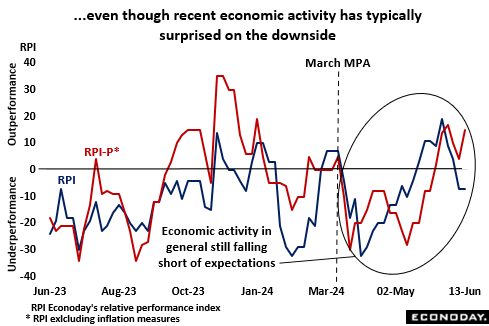

In general, economic data released since the March MPA have surprised on the downside. Over that period, Econoday’s RPI averaged minus 7 and its inflation-adjusted counterpart a marginally weaker minus 9. Neither reading is far enough below zero as to signal significant underperformance but note that CPI inflation surprised on the upside in two of the three months.

Against this backdrop, there is considerable uncertainty about what the SNB will decide this week. The fallout from the European Parliament elections may help to underpin the franc near-term, increasing the scope for another cut but domestic price pressures might have to ease further for the bank to pull the trigger. Whatever the bank decides, it seems likely that asset markets will react.