Edited by Simisola Fagbola, Econoday Economist

The Economy

Monetary policy

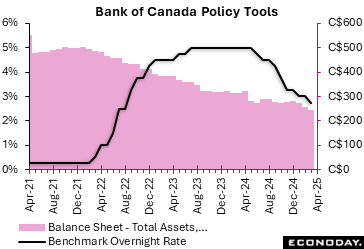

The Bank of Canada, as expected, left its target interest rate unchanged at 2.75 percent, as the central bank adopts a more cautious posture in the face of heightened risks to both its inflation mandate and the Canadian economic from the punitive tariffs imposed by the United States on Canadian imports.

“The major shift in direction of US trade policy and the unpredictability of tariffs have increased uncertainty, diminished prospects for economic growth, and raised inflation expectations,” the BoC statement said.

In a new addition to the statement, the central bank said it “will proceed carefully, with particular attention to the risks and uncertainties facing the Canadian economy.”

“These include: the extent to which higher tariffs reduce demand for Canadian exports; how much this spills over into business investment, employment and household spending; how much and how quickly cost increases are passed on to consumer prices; and how inflation expectations evolve,” it added.

The BoC noted that the tariff announcements and uncertainty are already a drag on both consumer and business confidence, which in turn is slowing down economic activity. “Consumption, residential investment and business spending all look to have weakened in the first quarter,” it said.

Meanwhile the trade tensions are also having a negative spillover effect in the labor market. “Employment declined in March and businesses are reporting plans to slow their hiring,” the statement said, adding, “[w]age growth continues to show signs of moderation.”

Starting this month, the BoC predicts that consumer price inflation will decelerate for one year due to the removal of the consumer carbon tax. Lower global oil prices will also dampen inflation in the near term.

“However, we expect tariffs and supply chain disruptions to push up some prices,” it added, and the extent to which this happens “will depend on the evolution of tariffs and how quickly businesses pass on higher costs to consumers.”

Short-term inflation expectations have risen, with higher costs expected from trade conflict and supply chain disruptions, while longer-term inflation expectations are little changed.

“Monetary policy cannot offset the impacts of a trade war,” the central bank said. “What it can and must do is ensure that higher prices do not lead to ongoing inflation.”

“Governing Council will be carefully assessing the timing and strength of both the downward pressures on inflation from a weaker economy and the upward pressures on inflation from higher costs,” the statement said.

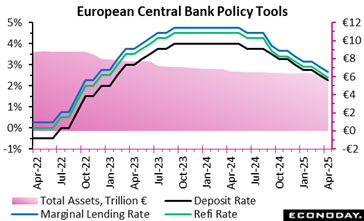

In April 2025, the ECB cut its three key interest rates by 25 basis points, lowering the deposit facility rate to 2.25 percent, the main refinancing operations to 2.40 percent, and the marginal lending facility to 2.65 percent. This move reflects growing confidence in the euro area’s disinflation trajectory, as both headline and core inflation—especially in services—have eased. Underlying inflation appears aligned with the ECB’s 2 percent medium-term target, aided by moderating wage growth and resilient profit margins that help absorb remaining cost pressures.

Despite inflation progress, the ECB faces new headwinds. Rising global trade tensions weaken growth prospects and fuel uncertainty, dampening consumer and business confidence. This and volatile market reactions could tighten financing conditions across the zone. Against this backdrop, the ECB is adopting a cautious, data-dependent stance, making interest rate decisions on a meeting-by-meeting basis.

Additionally, the ECB continues to scale back its Asset Purchase Programme and Pandemic Emergency Purchase Programme, reinforcing its shift away from crisis-era stimulus. Still, it remains committed to flexibility, with instruments like the Transmission Protection Instrument ready to safeguard monetary transmission and uphold price stability. This approach underscores the ECB’s commitment to stabilising inflation.

Employment

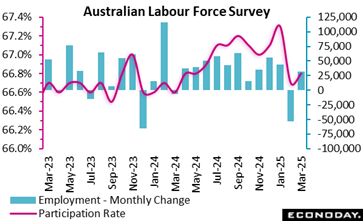

Labour market conditions in Australia rebounded in March, with employment increasing sharply from a previous decline and the unemployment and participation rates continuing to indicate very tight conditions. This will likely keep the focus of the Reserve Bank of Australia on risks to the inflation outlook despite concerns about the impact of global trade tensions.

The number of people employed in Australia rose by 32,200 in March, rebounding sharply from a fall of 52,800 in February and just below the consensus forecast for an increase of 33,000. Full-time employment rose by 15,000 persons after a previous fall of 35,700 persons, while part-time employment rose by 17,200 persons after a previous decline of 17,000 persons. Hours worked fell 0.3 percent on the month after an increase of 0.2 percent previously.

Today’s data also show the unemployment rate rose from 4.0 percent in February to 4.1 percent in March. The unemployment rate has been little changed from this level for a year. The participation rate rose from 66.7 percent to 66.8 percent, close to its recent high.

GDP

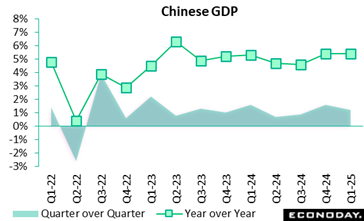

China’s GDP rose 1.2 percent on the quarter in the three months to March, moderating from growth of 1.6 percent in the three months to December, with year-over-year growth unchanged at 5.4 percent. Monthly activity data also published today showed stronger growth in key activity indicators but another substantial decline in house prices.

In their statement accompanying today’s data, officials characterised the data as showing the economy was “off to a good start” in 2025. Although officials did not explicitly refer to the recent escalation in global trade tensions and market volatility, they cautioned that the external environment is “complex and severe” and that drivers of domestic demand remain “insufficient”. Although they again pledged to “implement more proactive and effective macro policies”, officials provided no specific guidance about whether additional changes to policy settings will be considered in the near-term. Data published today were generally stronger than consensus forecasts.

Demand

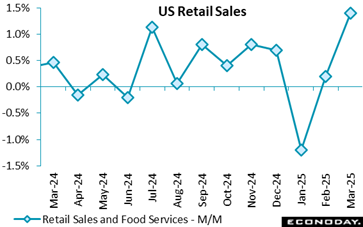

U.S. March retail sales jumped 1.4 percent, picking up the pace from the unrevised 0.2 percent monthly rise reported for February, and as expected in the Econoday survey of forecasters.

Core retail sales, removing autos and gasoline sales, rose 0.8 percent last month – compared to expectations for a 0.4 percent gain and a revised 0.8 percent rise in February (previously reported as +0.5 percent). Core retail sales are up 4.5 percent on an annual basis in March compared to a 4.2 percent (previously 3.5 percent) y/y rise in February.

Signs of the trade war’s drag on consumer spending won’t be reflected in the data until closer to the halfway point of the year, after prices have spiked.

There is clear evidence of ramped up spending ahead of the punitive tariffs now in place on most imported goods. Auto sales jumped 5.7 percent (+9.2 percent vs. last year).

There is also the expected surge in spending in certain sectors with severe winter weather now in the rearview mirror – building materials, garden equipment and suppliers’ sales are up 3.3 percent from February, while restaurants and bars’ sales increased 1.8 percent (+4.8 percent from March 2024).

There was just a 0.1 percent uptick in online sales, but they are still 4.8 percent higher than a year ago.

Compared to a year ago, March retail sales are up 4.6 percent, compared to February’s revised 3.5 percent jump (previously +3.1 percent).

Excluding gasoline, retail sales rose by 1.7 percent, speeding up from February’s 0.3 percent rise, and jumped 5.3 percent from March 2024 vs. +3.8 percent on an annual basis in February.

Stripping out purchases of motor vehicles and parts, sales increased 0.5 percent compared to a revised 0.7 percent increase (from +0.3 percent) in February. On an annual basis, retail sales ex-autos are up by 3.6 percent, a slowdown from February’s 3.8 percent (previously 3.1 percent).

Production

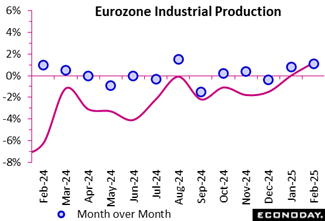

Euro area industrial production showed renewed momentum in February 2025, rising by 1.1 percent compared to January, outpacing the previous month’s 0.6 percent growth. This rebound suggests short-term resilience despite mixed sectoral performances. Non-durable consumer goods led the monthly expansion with a sharp 2.8 percent rise, indicating robust consumer demand for everyday items. Capital goods also posted a solid 0.8 percent increase, reflecting moderate investment activity, while declines in energy (minus 0.2 percent) and durable consumer goods (minus 0.3 percent) hint at ongoing caution and subdued long-term consumption.

On a year-over-year basis, Euro area industrial output grew only slightly by 1.2 percent, driven almost entirely by a remarkable 9.7 percent surge in non-durable consumer goods. All other major categories contracted: intermediate goods (minus 2.7 percent), capital goods (minus 1.8 percent), and durable consumer goods (minus 2.3 percent), signalling persistent structural weaknesses.

Regionally, industrial production fell across the top four-euro economies, with the largest falls experienced in Germany (minus 3.7 percent after minus 2.3 percent), Italy (minus 2.7 percent after minus 0.8 percent), and Spain (minus 1.7 percent after minus 1.4 percent). France (minus 0.3 percent after minus 1.0 percent) experienced the mildest annual fall.

While February’s monthly gains suggest modest recovery and consumer resilience, the annual trends reflect deeper sectoral imbalances and uneven demand, raising questions about the sustainability of industrial momentum across the euro area.

Sentiment

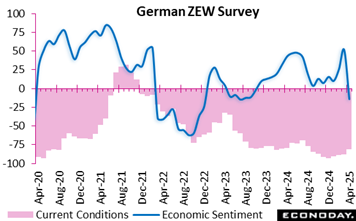

The April 2025 German ZEW economic sentiment indicator plunged to minus 14.0 points, marking a dramatic 65.6-point fall from the previous month—Germany’s steepest drop in expectations since the onset of the Russia-Ukraine conflict in 2022. This sharp downturn reflects growing anxiety among financial experts, triggered by unpredictable shifts in US trade policy and looming tariff threats fueling global uncertainty.

While sentiment has nosedived, the assessment of Germany’s current economic conditions remained in deep negative territory but showed slight improvements, rising by 6.4 points to minus 81.2, 4.8 points above the consensus. The deep negative reading continues to highlight the fragility of the recovery. Export-heavy sectors, including automotive, chemicals, and engineering—previously showing optimism—are now particularly vulnerable to rising trade tensions. Sentiment across the euro area echoed Germany’s gloom, with the outlook tumbling to minus 18.5 points and current conditions at minus 50.9.

Though inflation risks are not currently viewed as pressing, this has opened the door for potential interest rate cuts by the ECB. However, uncertainty remains high, particularly around whether the US Federal Reserve will follow suit. Overall, April’s data signals renewed pessimism and rising volatility in the eurozone’s economic narrative.

US Review

Underwhelming Retail Sales Points to Sluggish Q1 GDP

By Theresa Sheehan, Econoday Economist

The most important piece of US economic data in the April 18 week was the March report on retail and food services sales. Although total sales rose 1.4 percent in March and ended the quarter on an up note, sales were up only 0.2 percent in February and down 1.0 percent in January. The quarter as a whole isn’t that strong a performance for consumer spending and probably won’t be a standout for personal consumption expenditures beyond the durable goods components. Consumers are bringing forward purchases of big-ticket hard goods to avoid expected price increases from tariffs and/or possible shortages along the supply chain which was one of the reasons for the recent inflation episode. The advance estimate of first quarter GDP is set for release at 8:30 ET on Wednesday, April 30.

The big movers in the March retail data were the jump of 5.3 percent in sales of motor vehicles and parts and 3.3 percent in building materials. In some instances, the increase probably got a lift from the arrival of tax refunds which could be used as downpayments on some purchases or stretch the budget for outdoor maintenance after the winter months.