Edited by Simisola Fagbola, Econoday Economist

The Economy

Monetary policy

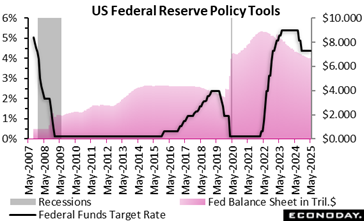

As expected, the US FOMC left the fed funds target rate range at 4.25 to 4.50 percent at the end of the May 6-7 meeting. The post-meeting statement highlights the increased uncertainty and risks to the economic outlook, although the assessment of current economy activity remains for a “solid pace” of expansion and “somewhat elevated” inflation. The statement did not mention inflation expectations, which have swung higher in the last few months.

The key language in the statement said, “The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Uncertainty about the economic outlook has increased further. The Committee is attentive to the risks to both sides of its dual mandate and judges that the risks of higher unemployment and higher inflation have risen.”

The tone of the statement tries to balance the current economic data which shows underlying growth continuing with a healthy labor market and progress in disinflation against the effects of unsettled government policies which are likely to affect the economy but to an unknown extent.

There was no dissent in the 12-0 FOMC vote. Minneapolis Fed President Neel Kashkari voted as an alternate for Cleveland’s Jeffrey Schmid.

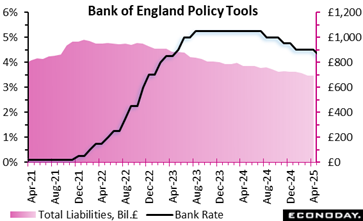

In May 2025, the Bank of England’s Monetary Policy Committee (MPC) voted by a narrow majority (5–4) to cut the Bank Rate to 4.25 percent, reflecting steady progress in disinflation, though uncertainty remains. Two members pushed for a deeper cut to 4 percent, while two preferred to hold at 4.5 percent, highlighting diverging views on inflation risks. CPI inflation eased to 2.6 percent in March, down from 2.8 percent in February, nearing the 2 percent target. Falling energy prices and cooling wage pressures have contributed, but a temporary rise in inflation to 3.5 percent is expected in the third quarter due to lagged energy effects.

Economic growth has slowed since mid-2024 and the labour market is softening, which supports a cautious loosening of monetary policy. However, global trade uncertainty and market volatility, triggered by renewed US tariffs and retaliatory measures, pose downside risks. The MPC is not on a fixed path and continues to assess whether inflation pressures stem more from persistent domestic costs or weakening demand.

In essence, the rate cut signals a shift toward easing, but the Committee remains vigilant, maintaining a restrictive stance to ensure inflation falls sustainably to target in the medium term.

Employment

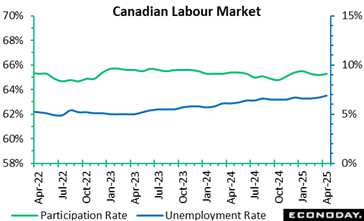

The Canadian economy added 7,400 jobs in April, not enough to make up for shedding 33,000 in March, but better than expectations in Econoday’s survey of forecasters for a decline of 3,000. The unemployment rate rose from 6.7 percent in March to 6.9 percent in April, higher than expectations for 6.8 percent.

April’s anemic employment numbers follow’s March’s decline in employment (the first since January 2022), and February’s flat employment reading. Before then, “the employment rate had increased for three consecutive months from November 2024 to January 2025, driven by strong employment gains amid slower population growth,” StatsCan said.

Compared to a year ago, employment is up by 268,800 (+1.3 percent) in April.

The data underlines the slowing pace of economic activity, with the trade war between Canada and the United States weighing on business confidence. This report, however, might add to the case for the Bank of Canada to remain on hold while it assesses the impact of the tariffs on economic conditions and inflation risks.

For April, employment fell in manufacturing (-31,000 or -1.6 percent) and wholesale and retail trade (-27,000; -0.9 percent) – industries with direct exposure to trade uncertainty.

Private sector jobs fell by 26,800 in April after a decline of 48,000 in March and a 10,200 rise in February. Public sector employment jumped 22,900 following March’s decline by 3,000, and +7,600 in February. Self-employment increased by 11,200, after rising by 18,000 in March.

The participation rate was 65.3 percent in April, vs. 65.2 percent in March and 65.3 percent in February. The participation rate is down 0.4 percentage points compared to a year ago.

Total hours worked rose 0.4 percent, the same as in March, and are up 0.9 percent from a year ago. Average hourly wages are up 3.4 percent year-over-year after the annual growth rate was +3.6 percent in March, and up 3.8 percent in February.

Demand

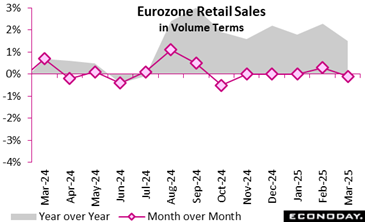

On a monthly basis, Eurozone retail trade volume dipped slightly by 0.1 percent, following a modest revised gain of 0.2 percent in February, indicating a pause in consumer momentum. Sector-wise, food, drinks, and tobacco sales edged down 0.1 percent, while non-food products also saw a 0.1 percent decline-perhaps signalling a tightening in discretionary spending. However, automotive fuel sales offered a modest lift, rising by 0.4 percent, possibly driven by increased mobility or seasonal factors.

On an annual basis, the picture was more encouraging. Retail trade rose by 1.5 percent compared to March 2024, buoyed by a 2.3 percent rise in non-food product sales and a 0.6 percent increase in food and drink purchases. Automotive fuel sales also rose by 0.9 percent, suggesting overall consumer demand remains more robust than monthly figures alone imply.

Despite revised February data showing a slightly weaker performance, the broader trend hints at cautious consumer confidence. The modest monthly dip may reflect ongoing economic uncertainty, while the annual growth points to underlying resilience in euro area consumption.

Production

In March 2025, Germany’s manufacturing sector saw a robust revival, with new orders rising by 3.6 percent month-over-month and 3.7 percent year-over-year, signalling a rebound in industrial demand after a flat February. Excluding large-scale orders, growth remained solid at 3.2 percent, suggesting broad-based improvements rather than one-off spikes.

Sectors such as pharmaceuticals (17.3 percent), electrical equipment (14.5 percent), and other transport equipment (13.0 percent) were key drivers, reflecting strong demand for high-tech and infrastructure-related goods. While the three-month trend still showed a 2.3 percent decline compared to the previous quarter, the exclusion of large-scale orders revealed a modest gain (0.5 percent), hinting at underlying momentum.

Foreign demand played a critical role, with euro area orders surging by 8.0 percent, reinforcing Europe’s importance to Germany’s export-led economy. Consumer goods orders also jumped (8.7 percent), potentially signalling improving household confidence. Meanwhile, manufacturing turnover increased by 2.2 percent in March, a welcome shift after modest gains earlier in the year. However, annual turnover remained slightly below March 2024 levels (minus 0.4 percent), suggesting some lingering caution. Indeed, the data paints a cautiously optimistic picture of manufacturing recovery in early 2025, driven by international demand and sector-specific dynamism.

Business Surveys

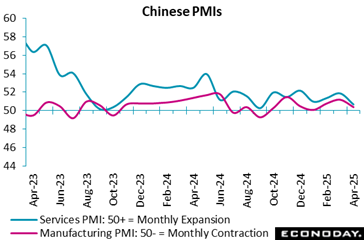

The S&P Global China manufacturing PMI showed slower expansion in the sector in April, with the headline index advancing to a four-month high of 51.2 from 50.8 in February. Official PMI survey also published today showed renewed contraction in the sector in April.

Respondents to the S&P PMI survey reported output, new orders, and new export orders all rose at a slower pace in April, with the latter increasing at the slowest pace in seven months. Respondents cited the impact of the increase in global trade tensions as a significant factor weighing on external demand. Payrolls were also reported to have cut in April after they had been increased for the first time since mid-2023 in March, and the survey’s measure of business confidence fell to tis third-lowest level on record, with respondents again citing concerns about trade tensions. The survey also shows input costs fell for the second month in a row and that firms cut selling prices for the fifth consecutive month.

The S&P Global PMI composite index for China fell to 51.1 in April from 51.8 in March, providing further evidence that the escalation in global trade tensions and market volatility the start of April has had an impact on conditions. The business activity index for China’s services sector fell to 51.1 from 50.7, while the headline index for the manufacturing PMI survey, published last week, also indicated conditions weakened in the sector. Official PMI survey data showed deterioration in both the manufacturing and the non-manufacturing sector in April.

Respondents to today’s service sector survey reported weaker growth in output and the smallest increase in new orders in more than two years April, though new export orders were reported to have risen at a slightly faster pace. The survey showed the fourth reduction in payrolls in the last five months and its measure of confidence fell to its lowest ever recorded level excluding February 2020, at the start of the Covid pandemic. Respondents also reported a marginal increase in input costs and another small reduction in selling prices.

The services index comes in a bit better than expected at 51.6 in April as it remains in expansion, up from 50.8 in March and the expected weaker 50.2. The better showing reflects gains in news orders, employment and supplier deliveries. The only discordant note is an increase in prices to 65.1 from 60.9. Employment remains negative at 49.0 in April versus 46.2 in March. Services continue to outperform manufacturing where contraction deepened in April from March.

US Review

FOMC: In the Fog of Trade War

By Theresa Sheehan, Econoday Economist

While the FOMC is always obliged to set the interest rate policy with a certain number of unknowns, the statement from the May 6-7 meeting highlights just how much those unknowns are challenging the committee’s work. The statement said, “The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Uncertainty about the economic outlook has increased further. The Committee is attentive to the risks to both sides of its dual mandate and judges that the risks of higher unemployment and higher inflation have risen.”

Fed Chair Jerome Powell’s press briefing was largely a reinforcement of the statement contents. Current underlying economic conditions are reasonably good with “solid” growth, stable unemployment, and still “somewhat elevated” inflation. The problem the FOMC faces is that the things that are likely to slow growth and reduce employment are in many ways the things that could raise prices.

For the moment, Fed policymakers see a resilient US economy in the face of chaotic and evolving policies out of the White House. But the downstream impacts of unsettled conditions are only just becoming visible. The sharp worsening of the trade deficit is only the first directly attributable to tariff policy as businesses and consumers acted in advance of expected higher prices. Now it remains to be seen if those higher prices are felt in the broad measures of inflation, and, if so, if these are short-term effects or will be more entrenched.

In any case, prices that go up are unlikely to come down again. While consumers and businesses will have to spend for essentials, discretionary spending probably will decline and with it the pace of GDP growth.