Edited by Simisola Fagbola, Econoday Economist

The Economy

Monetary policy

The Reserve Bank of Australia left its main policy rate, the cash rate, on hold at 3.85 percent at its policy meeting. This decision was a surprise, with the consensus expecting a second consecutive reduction of 25 basis points.

In the statement accompanying the decision, official noted recent declines in inflation and expressed optimism that risks to the inflation outlook remained balanced after they were more concerned previously about upside risks. They noted, however, that monthly inflation data indicates that quarterly inflation in the three months to June will be stronger than they had previously expected.

Having already cut policy rates by 50 basis points in recent months, this uncertainty about near-term inflation prospects means officials are cautious about loosening policy too aggressively. As a result, they judged today that they “could wait for a little more information to confirm that inflation remains on track to reach 2.5 per cent on a sustainable basis.”

The statement shows, however, that today’s decision was not unanimous, with only six of the nine members voting to keep policy rates on hold. In the post-meeting press conference, RBA Governor Michele Bullock advised that a majority of members "decided to wait a few weeks to confirm that we’re still on track to meet our inflation expectation", further noting that "the decision today was about timing rather than direction.” This suggests that there is a good chance that a majority of members could support a rate cut at the next meeting if data provide greater confidence about the inflation outlook.

Inflation

China’s headline consumer price index rose 0.1 percent on the year in June, up from a decline of 0.1 percent in May, and fell 0.1 percent on the month after dropping 0.2 percent previously. Food prices fell 0.3 percent on the year, but this was offset by price increases for non-food items, with core inflation at 0.7 percent. Producer price inflation data also published today showed ongoing weakness in price pressures.

China’s headline producer price index fell 3.6 percent on the year in June, weakening further from the 3.3 percent decline recorded in May. Headline PPI inflation has been in negative territory since late 2022 and this is the biggest year-over-year decline since July 2023. The index fell 0.4 percent on the month, as it did previously. Consumer price data also published today showed headline inflation remained close to zero in June.

Employment

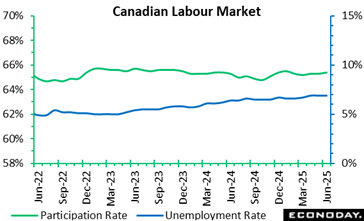

Surprise. The Canadian economy created a stunning 83,100 jobs in June, far more than the consensus expectation of 8,000 in an Econoday survey of forecasters. The economy hadn’t added that many jobs since December 2024. The unemployment rate ticked down to 6.9 percent while expectations had centered on an increase to 7.1 percent from 7.0 percent. This was the first unemployment rate decline since January. The participation rate edged up to 65.4 percent from 65.3 percent.

A 69,500 gain in part-time employment led the overall increase in June, although full-time was also up 13,500. Employment was driven by the private sector, which added 46,600 jobs, nearly twice as much as the public sector. Services increased 73,100 while goods-producing industries were up 10,100.

Layoffs rates are holding steady.

For those with a job, wage growth slowed to 3.2 percent year-over-year, down from an average hourly rate increase of 3.4 percent in May (unadjusted). Hours worked increased 0.5 percent on the month and 1.6 percent year-over-year.

Does this mean any Bank of Canada rate cut is off the table? Probably not, given ongoing trade-related uncertainty. The minutes from the June policy meeting showed "some diversity of views for the most likely path ahead" reflecting the diverging forces at play: on the one hand tariffs and uncertainty threaten growth and on the other hand they are a risk for inflation.

On the tariff front, uncertainty is still strong. Recently, U.S. President Donad Trump ended trade talks due to a digital tax that was about to come into effect. Canada responded by rescinding the digital tax that would have impacted large tech companies like Google and Amazon. This move by Prime Minister Mark Carney, while criticized internally, revived hopes for a bilateral agreement in July. However, Trump is now threatening 35 percent tariffs on Canadian goods starting August 1, reminding of the political volatility. The Canadian economy proved more resilient than expected in the first quarter, but the central bank expects a significant weakening in the second quarter. GDP growth contracted 0.1 percent in April and the advance estimate for May points to another contraction. On the inflation front, there was some easing in May, which, combined with the wage growth slowdown, provide some leeway to the central bank. But, core inflation remains quite a bit higher than the central bank’s target for comfort and likely in the “firmness” zone.

In addition to ongoing uncertainty, today’s employment data showed some vulnerability given that job gains were concentrated in part-time and that long-term unemployment increased.

Overall, the jobs report gives more reason to the central bank to wait and see, especially since one of the most at-risk sectors – manufacturing – saw a 10,500 gain in employment, which, together with a 7,600 increase in construction, drove gains in goods-producing industries in June.

Most of the June increase came from services, with a 33,600 surge in wholesale and retail trade and a 16,700 growth in health care and social assistance. Professional, scientific and technical services were up 11,900. Employment decreased in only two services sectors: transportation and warehousing (-3,400) and “other services” excluding public administration (-8,500).

GDP

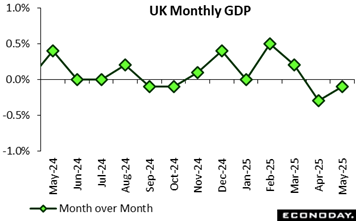

The UK economy contracted by 0.1 percent in May 2025, extending April’s decline and revealing a fragile recovery path. Despite a promising 0.4 percent growth in March (revised up), momentum has faltered over the past two months, suggesting an uneven economic landscape.

Still, the broader picture is more encouraging: GDP grew 0.5 percent in the three months to May, mainly supported by the services sector, which rose 0.1 percent in May and 0.4 percent over the three-month period. This signals ongoing demand from consumers and businesses, particularly in contact-intensive industries.

In contrast, production output plunged by 0.9 percent in May, continuing April’s slump. This indicates persistent weakness in manufacturing and energy-intensive sectors, likely due to input cost pressures or fluctuations in global demand. Meanwhile, construction dipped 0.6 percent in May, partly reversing April’s gain, though the sector still recorded a robust 1.2 percent rise over the quarter, possibly due to renewed infrastructure and housing investment.

Overall, while the quarterly trend remains positive, May’s contraction highlights underlying vulnerabilities. The divergence between resilient services and struggling production suggests that the recovery is imbalanced.

Demand

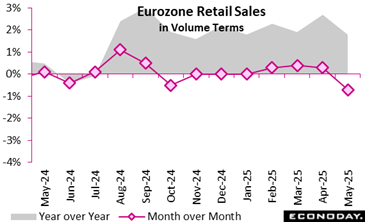

Retail trade in the euro area showed mixed dynamics in May 2025, reflecting the impact of consumer caution and shifting spending patterns. Compared to April, retail volumes declined by 0.7 percent, reversing the modest 0.3 percent growth recorded in the previous month. All major sectors experienced monthly contractions: food, drinks and tobacco dropped by 0.7 percent, non-food products by 0.6 percent, and automotive fuel by a sharper 1.3 percent, pointing to broader demand-side restraint possibly linked to cost-of-living concerns or volatile fuel pricing.

However, the annual picture was more encouraging. Compared with May 2024, retail trade rose by 1.8 percent, signalling a gradual recovery in consumer confidence. The most substantial growth came from automotive fuel (2.8 percent) and non-food products (2.4 percent), indicating rising mobility and discretionary spending. Even essential items like food and drink posted a modest 0.5 percent annual gain, underscoring some stability in household purchasing behaviour.

Overall, while monthly volatility suggests near-term headwinds, possibly influenced by inflationary pressures or subdued wage growth, the annual gains imply that retail activity is on a slow but positive trajectory. Policymakers may need to monitor household resilience, as further economic tightening could dampen fragile consumer momentum.

Production

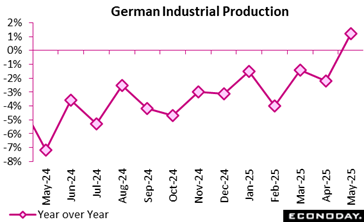

Germany’s manufacturing sector showed signs of resilience in May 2025, with production rebounding by 1.2 percent compared to April, reversing the revised 1.6 percent decline seen the previous month. Year-over-year, production was 1.2 percent higher. The surge was driven largely by the automotive industry (4.9 percent) and a remarkable boost in energy production (10.8 percent), while pharmaceuticals also contributed strongly with a 10.0 percent rise. However, the construction sector dragged on overall growth with a 3.9 percent drop.

When excluding energy and construction, core industrial production rose by 1.4 percent, with capital goods leading the way (4.1 percent), followed by consumer goods (0.5 percent). Nonetheless, intermediate goods production fell by 2.1 percent, reflecting lingering supply chain bottlenecks or weaker demand in upstream sectors.

A concerning trend is the continued contraction in energy-intensive industries, which declined by 1.8 percent in May alone and stood 4.8 percent below their May 2024 levels. This suggests that elevated energy costs or structural shifts in energy policy are weighing heavily on these segments.

Overall, the sector is showing a tentative recovery, but the uneven performance across sub-sectors points to fragility and the need for policy support to sustain momentum.

US Review

FOMC Continues Watch for Labor Market Weakness Vs. Inflation Threat

By Theresa Sheehan, Econoday Economist

As the release of the minutes of the June 17-18 FOMC meeting reinforced, Fed policymakers are faced with the problem of judging the risks associated with a weakening labor market versus renewed upward price pressures from tariffs.

The June employment report released July 3 showed slower hiring and a smaller labor force. In assessing labor market conditions, the FOMC will have to determine if a still low national unemployment rate of 4.1 percent is an accurate reflection of the jobs market. If the US economy is heading into a recession, rising unemployment may not be the red flag it usually is when the economy enters a downturn. Does the lack of a rising unemployment rate mean no recession on the horizon? Or will the FOMC take more note if payrolls stop growing enough to absorb new entrants and the unemployed in the labor force?

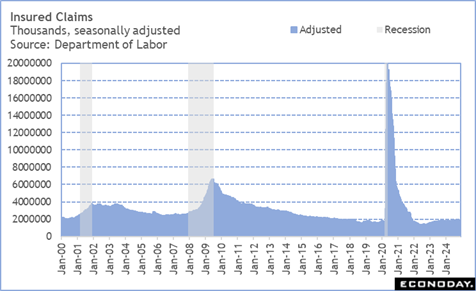

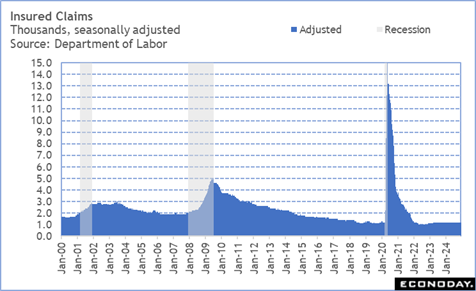

And are there any signs that payrolls will start shrinking due to layoff activity? At present, weekly jobless claims remain low in the historical context. New claims are down 5,000 to 227,000 in the July 5 week in the latest report. However, the seasonal adjustment factors for early- to mid-July anticipate a lot of short-term layoffs, mostly in the auto sector for the annual retooling period. This may not be happening on the scale it usually does, so new claims are going to look soft for another week or two.

There’s a hint of lengthening periods of unemployment in the insured claims data as it settles into a new trend level just below the 2.0 million mark. The insured rate of unemployment is now trending a bit higher than in the prior two years with a reading of 1.3 percent for the past five weeks.

The changes are small, but then history tells us that among those applying for unemployment and those receiving it, the peak numbers occur when a recession is already well in place.