Edited by Simisola Fagbola, Econoday Economist

The Economy

Inflation

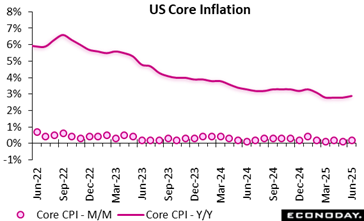

June’s warm US inflation data could be the start of the expected inflationary effects of higher tariffs (predicted to hit from mid-2025 onwards). This will bolster the Federal Reserve’s wait-and-see stance as it assesses if this report does mark the beginning of a broad and sustained inflationary impact from the tariffs.

The Consumer Price Index in June ramped up by +0.3 percent, following a 0.1 percent rise in May, and a 0.2 percent jump in April. The June CPI reading matches expectations for a 0.3 percent rise in the Econoday survey of forecasters. This ends the slowdown in the monthly pace of overall consumer price inflation seen between February and May.

Over the last 12 months, consumer prices are up 2.7 percent, compared to a 2.4 percent year-over-year rise in May. Expectations in the Econoday survey were for a 2.6 percent increase.

Core CPI, excluding food and energy prices, is up 0.2 percent, after rising 0.1 percent in May, and +0.2 percent in April. Consumer prices less food and energy rose 2.9 percent from June 2024, following a 2.8 percent year-over-year rise in May, and as expected in the Econoday survey.

After rising by 0.3 percent in May, shelter costs rose by 0.2 percent in June (and are up 3.8 percent year-over-year). Food prices increased by 0.3 percent, the same rate as in May, with grocery prices up 0.3 percent last month, and restaurant prices rising 0.4 percent.

Energy costs rebounded by 0.9 percent over the month, powered by a 1 percent rise in electricity as well as gasoline prices.

Energy prices are down 0.8 percent year-over-year, following a 3.5 percent slide for the 12 months ending May. Food prices increased by 3 percent compared to June 2024, following a 2.9 percent rise in May.

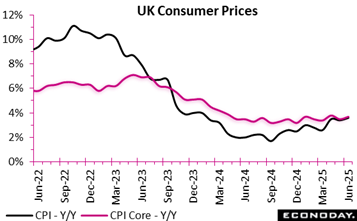

UK inflation ticked upward in June 2025, reflecting persistent pressures across both goods and services. On an annual basis, headline inflation accelerated to 3.6 percent from 3.4 percent in May, while core CPI (stripping out volatile items) edged up to 3.7 percent, signalling underlying inflationary momentum remains firm. Goods inflation increased from 2.0 percent to 2.4 percent, driven by rising fuel prices, while services inflation stayed elevated at 4.7 percent, underscoring the resilience of domestic cost pressures.

Meanwhile, CPIH, which includes owner occupiers’ housing costs, rose by 4.1 percent year-over-year, up marginally from 4.0 percent, with the monthly gain of 0.3 percent from 0.2 percent reflecting broad-based increases. Notably, core CPIH rose to 4.3 percent from 4.2 percent year-over-year, maintaining its upward trajectory despite a slight easing in services inflation (from 5.3 percent to 5.2 percent). Transport, especially motor fuel, was the primary upward driver of both the CPI and CPIH, partially offset by slower growth in housing-related costs.

Indeed, the latest updates suggest that the service sector is the key driver of inflation with a re-emergence of goods inflation, complicating the Bank of England’s path to easing. While headline rates may appear to stabilise, core indicators reveal that price pressures are still deeply rooted, suggesting continued caution in monetary policy adjustments.

Employment

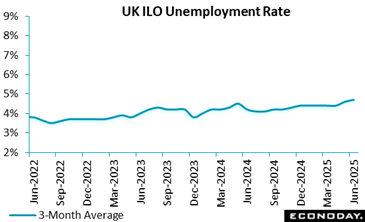

The UK labour market employee numbers are steadily declining, with 135,000 fewer workers between May 2024 and May 2025, and a further provisional drop of 178,000 by June 2025 over the year and 41,000 on the month. This downturn coincides with the 36th consecutive quarterly fall in vacancies, reflecting growing employer hesitancy in hiring or replacing staff.

Despite this contraction, the employment rate has slightly improved to 75.2 percent, while unemployment has risen to 4.7 percent, suggesting a possible lag between job losses and rising joblessness. Meanwhile, economic inactivity has edged down to 21.0 percent, hinting at modest labour market re-engagement.

On pay, annual average earnings grew by 5.0 percent, with real wages also improving, 1.8 percent for regular pay and 1.7 percent for total pay (CPI-adjusted). This reflects ongoing cost-of-living pressures but signals some resilience in income growth. The public sector outpaced the private sector in regular pay growth (5.5 percent vs. 4.9 percent). Nonetheless, rising claimant counts and a sharp fall in recruitment activity suggest underlying fragility.

With 37,000 working days lost to labour disputes in May alone, industrial tensions further complicate the outlook, emphasising the need for cautious optimism amid persistent volatility.

GDP

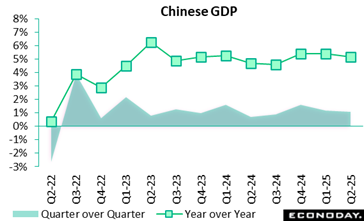

China’s GDP rose 1.1 percent on the quarter in the three months to June, little changed from growth of 1.2 percent in the three months to March, with year-over-year growth easing from 5.4 percent to 5.2 percent. Monthly activity data also published today showed solid growth in key activity indicators in June but another substantial decline in house prices.

In their statement accompanying today’s data, officials characterised the data as showing the economy "withstood pressure and made steady improvement despite challenges". Although officials refrained from explicitly referring to trade tensions with the United States, they noted a need to "coordinate domestic economic work and endeavours in the international economic and trade field" and to "cope with external uncertainties". Officials reiterated their commitment to "more proactive and effective macro policies" but provided no specific guidance about whether additional changes to policy settings will be considered in the near-term.

Demand

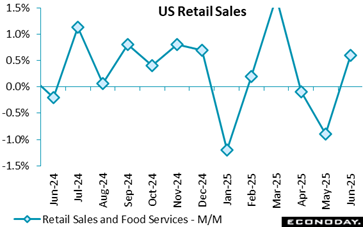

There was a stronger-than-expected recovery in US consumer spending in June, although not enough to offset May’s decline in consumption. The underlying data, however, show enough resilience for Federal Reserve officials to remain patient regarding the timing of the next rate cut.

U.S. June retail sales jumped by 0.6 percent, partially rebounding from the unrevised 0.9 percent monthly drop reported for May, and much greater than the +0.1 percent consensus in the Econoday survey of forecasters.

Core retail sales, removing autos and gasoline sales, also increased 0.6 percent last month following a revised flat reading in May (previously reported as -0.1 percent). Core retail sales are up 4.1 percent on an annual basis in June compared to a 4.6 percent y/y jump in May.

Auto sales rose 1.2 percent in June, not enough to erase May’s 3.8 percent decline, but is up 6.5 percent vs. last year. Activity appears to be recovering after dwindling following the pre-tariffs spike in March.

Summer spending is solid, not robust, with building materials, garden equipment and suppliers’ sales up 0.9 percent in June, while restaurants and bars’ sales increased 0.6 percent (and +6.6 percent from June 2024).

E-commerce sales slowed down to a 0.4 percent increase in June from +0.6 percent in May, and they are 4.5 percent higher than a year ago.

Compared to a year ago, June retail sales are up 3.9 percent, compared to May’s 3.3 percent jump.

Excluding gasoline, retail sales increased 0.7 percent, falling after May’s 0.8 percent drop, and jumped 4.6 percent from June 2024 vs. +4.0 percent on an annual basis in May.

Stripping out purchases of motor vehicles and parts, sales rose 0.5 percent compared to 0.2 percent drop (previously -0.3 percent) in May. On an annual basis, retail sales ex-autos are up 3.3 percent, a slowdown from May’s 3.6 percent pace.

Production

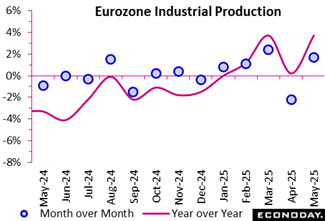

In May, US industrial production rebounded by 1.7 percent over the month after a revised decline of 2.2 percent in April. This revival was driven by surging demand for non-durable consumer goods, which soared 8.5 percent month-over-month, suggesting a shift in household consumption towards essentials amidst lingering economic uncertainty.

Energy production also saw a solid 3.7 percent uplift, reflecting possible seasonal or supply-side shifts, while capital goods rose by 2.7 percent, hinting at renewed investment confidence. However, the decline in intermediate goods (minus 1.7 percent) and durable consumer goods (minus 1.9 percent) suggests that some supply chain bottlenecks and consumer caution persist.

Year-over-year, the picture is even more optimistic: total industrial output jumped 3.7 percent compared to May 2024. Notably, non-durable consumer goods surged 11.6 percent, showing strong household resilience. Capital goods followed with a 4.5 percent rise, potentially pointing to long-term economic optimism. Yet, the annual fall in intermediate goods (minus 1.8 percent) might signal structural issues within production chains.

Regionally, industrial production on an annual basis rose in Germany (1.9 percent after minus 2.5 percent) and Spain (1.7 percent after 0.4 percent), while it slightly rose in France (minus 1.0 percent after minus 1.5 percent) but remained in negative territory for France. However, it fell in Italy (minus 0.9 percent after 0.1 percent) on an annual basis.

Summarily, May’s data show that industrial production is recovering, with strength in consumer essentials and investment signalling a stabilising industrial base in the euro area.

US Review

Fed’s Waller/Bowman: Signaling Fed Policy Shift?

By Theresa Sheehan, Econoday Economist

On July 17, Fed Governor Christopher Waller explicitly said he would support a 25 basis point cut in the fed funds target range at the July 29-30 FOMC meeting. He placed his view within the current available economic data and the expectation that inflation from tariffs would result in “one-off increases in the price level.”

Back on June 23, Vice Chair for Supervision Michelle Bowman said she would favor a rate cut at the July FOMC meeting if inflation pressures remained “contained”.

Since Both Waller and Bowman are appointees of the previous Trump administration, there will inevitably be a political context given to these views. Speculation about a power play within the Federal Reserve Board of Governors will rise now that President Donald Trump is clearly intending to find a way to get rid of current Chair Jerome even as he placates markets with denials. Rifts among members of the board are likely due far more to sincere differences of opinion than political maneuvering, although it would be naïve to dismiss it entirely.

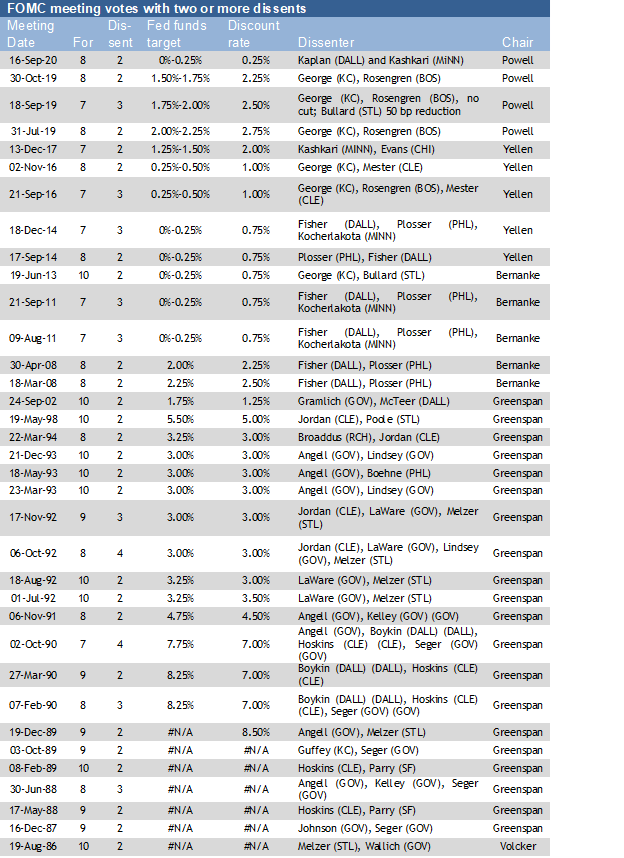

In any case, this sets up the next meeting as unusually contentious with the potential for at least two dissents in the vote. One dissent in the FOMC vote is not that uncommon, but two or more signal a bigger internal debate. And the dissents are likely from the governors where commonly it is the district bank presidents who dissent. The last time there was significant opposition by governors to setting restrictive monetary policy at a time of inflation was during the tenure of Paul Volcker.

Something the same may be happening here from the “tensions” in the dual mandate that Powell and other have mentioned recently. There are FOMC voters who will be focused on the weakening in the labor market and less concerned about a short-term rise in inflation. There are FOMC voters who will focus on the low unemployment rate and worry about allowing inflation to become an issue again along with rising inflation expectations for the longer-term.

A divergence of opinions on the FOMC that shows up as a dissent is often a signal of a shift in monetary policy. The wider the divergence, the more likely it is that policy is moving toward a change.