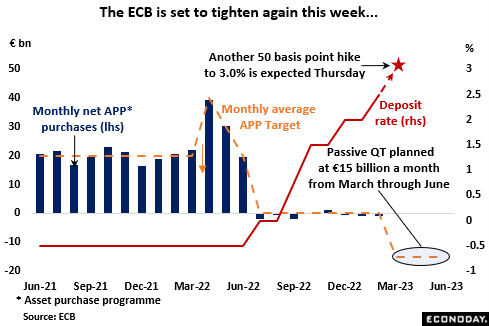

In terms of policy, Thursday’s announcement should be something of a damp squib. Although supposedly no longer offering forward guidance, the February statement made it clear that the ECB intends to raise its key interest rates by a further 50 basis points. This would put the (still key) deposit rate at 3.0 percent, the refi rate at 3.5 percent and the rate on the marginal lending facility at 3.75 percent. It would also boost the cumulative tightening since last July to some 350 basis points.

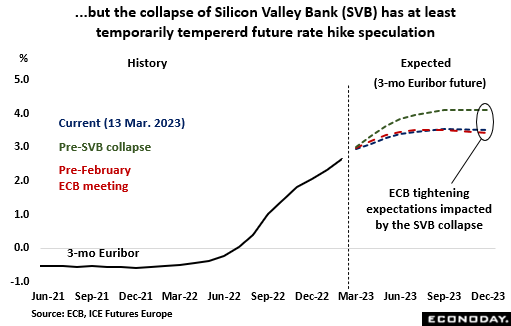

In fact, Governing Council (GC) members have recently been out in force and, for once, have been unanimous in expressing the need to tighten by a further 50 basis points this week. Beyond that though, there are wide splits over how high rates should go and how long they should be held at peak levels. Hence, while late last month the French central bank Governor François Villeroy de Galhau was saying that ECB rates were already in restrictive territory, his Bundesbank counterpart Joachim Nagel was insisting that current levels were still too low to put any brake on economic activity. Just last week, Austrian central bank chief Robert Holzmann called on the ECB to raise rates by 50 basis points at each of its next four meetings while his Italian counterpart Ignazio Visco insisted that decisions are only supposed to be taken on a meeting-by-meeting basis. Consequently, and particularly in the wake of the collapse of Silicon Valley Bank (SVB) last week, investors will be looking at the policy statement and President Lagarde’s post-meeting address for any additional forward guidance on what to expect at the next meeting in May.

Passive QT began at the start of March with the bank having already indicated that it would aim to reduce its balance sheet by an average €15 billion each month through the end of the second quarter whereupon it would determine the subsequent pace of shrinkage. Compared with its peak level in June 2022, the overall balance sheet has already shrunk by just over €1 trillion to €7.83 trillion. Of note, according to Chief Economist Philip Lane, the bank’s models estimate that reducing the asset portfolio by a total of €500 billion over 12 quarters should trim inflation by 0.15 percentage points and output by 0.2 percentage points. This shows that while interest rates remain the most important policy tool, at the margin, asset sales should help to reduce the extent to which they will rise over the current cycle. As regards the pandemic emergency purchase programme (PEPP), which was terminated last March, expect the bank to reaffirm its intention to fully reinvest maturing assets until at least the end of 2024.

Following the February meeting, market expectations for ECB tightening in 2023 became notably more aggressive. In fact, shortly before news about SVB, from then nearly 3.0 percent, futures saw 3-month money rates continuing to rise throughout the year to above 4.0 percent in December. That was more than 50 basis points higher than anticipated just before last month’s announcement. However, in the wake of SVB’s problems, such expectations have been trimmed and the future profile now looks little changed from February with rates again put at close to 3.5 percent at year-end. That said, the decline in 2024 is still shallower and even in June 2024, rates are seen around 3.3 percent. How long the SVB effects last remains to be seen but investors will be watching closely for any commentary on the subject on Thursday.

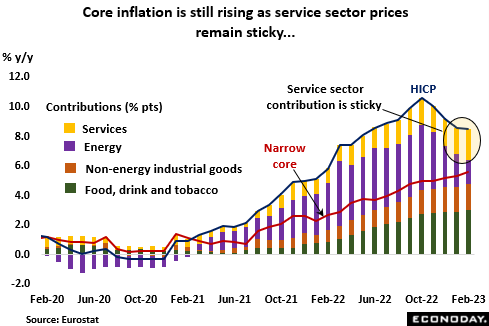

In any event, the outlook for interest rates remains inexorably tied to inflation. Absent another major energy price shock, the headline rate has almost certainly peaked. However, the underlying rate is a totally different matter. As the Executive Board’s Isabel Anna Schnabel is keen to point out, the broad disinflation process has not even started yet. Indeed, February’s flash HICP report showed the narrow core rate accelerating from 5.3 percent to 5.6 percent, more than double its level a year ago, and the broader index, which excludes just energy and unprocessed food, climbing from 7.1 percent to 7.4 percent. Both readings were new all-time highs. An increasing problem for the ECB is the services sector where prices are being underpinned by an apparent switch in consumer demand away from goods and, in this regard, the reweighting of the HICP basket in January has not helped matters. In previous years, changes to component weights have been only small and of little importance to the inflation trend but the broad shifts in household spending patterns caused by Covid has meant the 2023 adjustments are unusually large and have boosted the service sector share (now 43.5 percent).

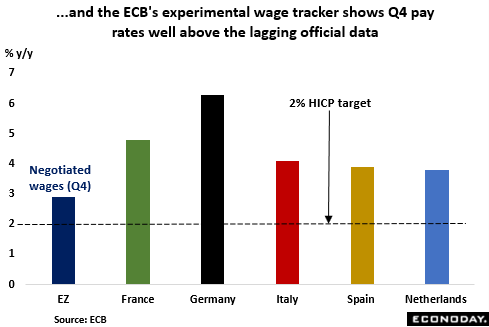

Meantime, the ECB is keeping a very wary eye on wages in what continues to be a very tight labour market – at 6.7 percent, the January jobless rate was just a tick above last October’s record low. Official data from Eurostat put annual wage growth last quarter at 2.9 percent, unchanged from its third quarter reading and in itself, no obvious threat to inflation. However, the central bank’s own experimental wage tracker shows the larger Eurozone countries running at significantly faster rates and the central bank has warned that wage growth over the next few quarters is likely to be very strong compared with historical patterns. Just last month the Bundesbank said that the second-round impact of strong wage growth would probably keep Eurozone inflation above target for an extended period. The ECB has also made noises to the effect that it is worried about firms using the umbrella of high inflation to mask price rises aimed at boosting profits. This is an issue that will get increasing attention over coming months. More optimistically, the ECB’s own January survey found household inflation expectations dipping for the coming 12 months from 5.0 percent to 4.9 percent and, for the next three years, falling quite significantly from 3.0 percent to 2.5%. However, both gauges remain well above the 2 percent HICP target.

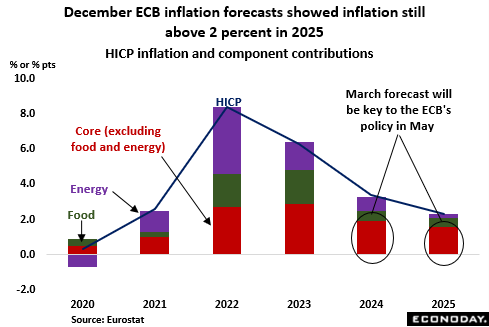

In its December forecast, HICP inflation was projected to average 8.4 percent in 2022, before decreasing to 6.3 percent this year, 3.4 percent in 2024 and 2.4% in 2025. Excluding food and energy, the rate was seen falling from 4.2 percent in 2023 to 2.4 percent in 2025. In other words, both measures ended the forecast horizon still above target. The new projections will have a big say in upcoming policy decisions and will probably need to be clearly lower if the bank is to feel comfortable limiting any hike in May to just 25 basis points.

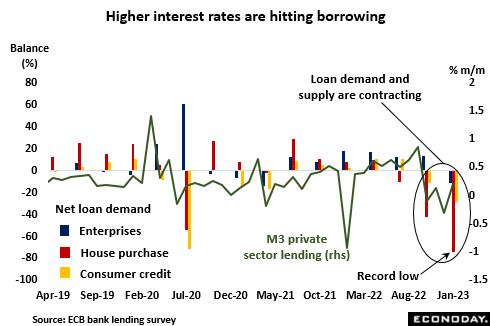

Even if current interest rate levels are not yet having the desired impact on inflation, they are feeding through into private sector lending. According to the ECB’s latest bank lending survey, loan demand from enterprises and households contracted last quarter for the first time since the first quarter of 2021, in the midst of the pandemic. Indeed, demand for home loans fell by the most on record. Reflecting this, average monthly growth of M3’s private sector lending counterpart slowed from 0.7 percent in the third quarter of last year to minus 0.1 percent in the period just ended. Tighter financial conditions will hit economic activity in general over coming months and will ultimately help to drive inflation down.

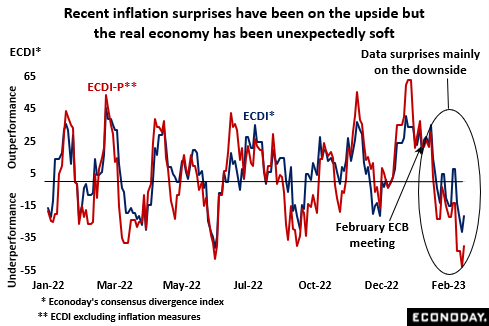

In fact, outside of positive inflation shocks, economic indicators released since the February ECB meeting have typically surprised on the downside. Econoday’s consensus divergence index (ECDI), which measures how overall economic activity has been performing versus market expectations, has been below zero for most of the time. Indeed, the latest reading (minus 21) would be significantly more negative but for the buoyancy of inflation. Hence, the ECDI-P, which omits inflation surprises, now stands at minus 40, only just above its record low. However, while this makes for downside risk to first quarter GDP, an underperforming real economy will not overly trouble a central bank so focussed on achieving its price stability goals.

Much of the ultimate inflation impact of the ECB’s tightening measures to date is still in the pipeline. Even so, with inflation so far above target and underlying trends still rising, further hikes in interest rates would seem unavoidable. However, subject to the fallout from the failure of SVB, perhaps even more than usual, their future profile will have to reflect an increasingly uneasy compromise between the doves and the hawks.