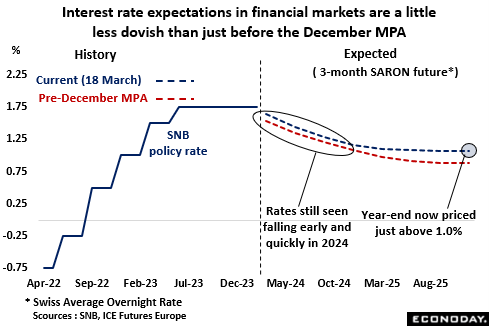

The consensus is no change but there is significant speculation that the SNB might announce a 25 basis point cut in its policy rate at Thursday’s Monetary Policy Assessment (MPA). Further falls in already low inflation combined with a strong Swiss franc would seem to have opened the door to what would be the first reduction in the benchmark rate since January 2015 when the central bank also abandoned its minimum exchange rate policy. Currently the rate stands at 1.75 percent, its highest mark in 15 years. However, probably more than most other major central banks, the Swiss monetary authority has acquired a habit of surprising forecasters and most investors seem far from convinced that an ease will come as soon as this week.

In fact, near-term interest rate expectations in financial markets are now rather higher than they were just before the December MPA when March rate cut hopes were close to their peak. That said, 3-month money rates are still seen coming down quite rapidly through 2024 and into early-2025 before flattening out close to 1.0 percent over the second half of next year.

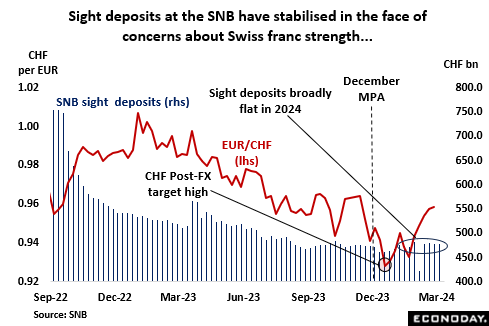

In terms of QT, the bank announced in December that it would no longer focus on foreign currency sales as it believed that the stance of policy was appropriate. This decision has been reflected in the bank’s balance sheet where, despite some inevitable monthly volatility, the level of sight deposits has hardly changed since the start of the year. This contrasts with the sharp decline seen from the September 2022 through the end of 2023 when the bank was actively seeking to dispose of assets.

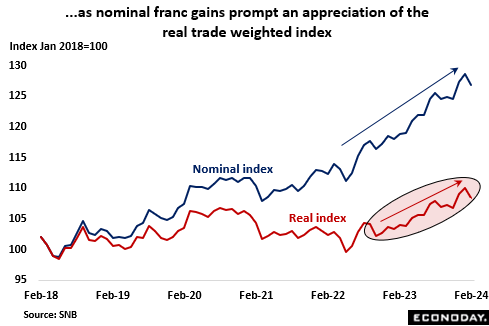

However, the exchange rate remains a major focus of policy. For some while now, the SNB has seen a nominal strengthening by the Swiss franc as a useful guard against possible imported inflation. However, more recently the bank has warned about the damaging effects of a real appreciation of currency on export competitiveness. Since the fourth quarter of 2022, the inflation-adjusted trade weighted index has risen by more than 6 percent. This suggests that while still favouring currency stability, the bank is less prepared to accept additional gains by the franc. To this end, any references to the currency markets in the policy statement could make for interesting reading.

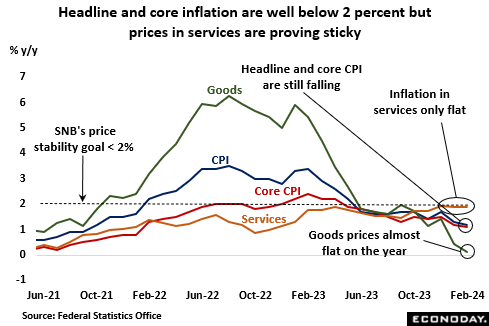

In the main, inflation developments since the December MPA have been favourable. Both the headline rate (1.2 percent in February) and the core (1.1 percent) have declined further, the two measures stretching their unbroken run below 2 percent to nine and 10 months respectively. The overall rate is set to undershoot the SNB’s first quarter forecast (1.8 percent) and the underlying gauge is now at its weakest level since January 2022. Still, the slide has been driven by the goods producing sector where prices last month were just 0.1 percent higher on the year. Inflation in services is another matter and since rising to 1.9 percent in December, the rate has held steady and well above the 1.5 percent low posted last September.

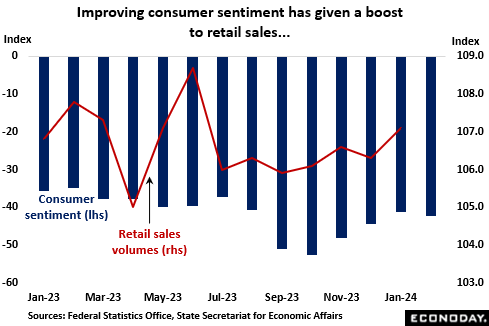

The real economy was mixed at the end of last year. A respectable 0.3 percent quarterly rise in real GDP matched the previous period’s gain and was led by stronger household spending (also up 0.3 percent). The recent improvement in consumer sentiment seems to have had a positive impact. However, gross fixed capital formation (minus 1.8 percent) contracted for a third consecutive quarter to stand at its weakest level since the early days of Covid. Overseas, net foreign trade provided a moderate boost and, despite official concerns, with non-monetary gold exports (up 0.5 percent) having avoided contraction for nearly three years, showed little evidence of the Swiss franc being significantly overvalued.

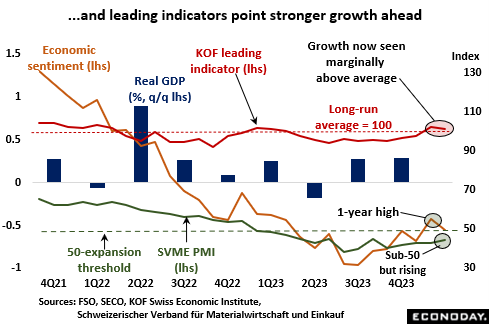

Leading indicators point to a slightly faster pace of growth to come. The KOF’s closely watched measure has moved back above its long-run average and although the February manufacturing PMI was still sub-50, it at least achieved a 5-month high. At the same time, its service sector counterpart has been above the growth threshold for the last seven months and in January SECO’s economic sentiment gauge posted its strongest reading in a year. Importantly too, although the labour market is now cooling as unemployment rises on the back of declining job vacancies, it continues to do so only slowly. Last month’s (seasonally adjusted) jobless rate was just 2.2 percent, still some 0.8 percentage points below its long-run average. Accordingly, pressure from the real economy for an early cut by the SNB is relatively limited.

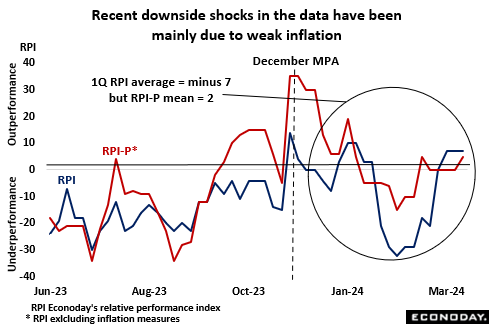

On balance, economic data released since the start of the year have surprised slightly on the downside. Hence, Econoday’s relative performance index (RPI) has averaged minus 7 over the period to date. However, with the mean value of its inflation-adjusted counterpart (RPI-P) standing at 2, the real side of the economy has evolved much as forecast. Rather, the overall underperformance can be largely attributable to the unexpected weakness of prices which, in itself, should be seen as increasing scope for the SNB to ease.

In summary, there a real chance that on Thursday the SNB will become the first of the larger central banks to reduce official interest rates. With sustained low inflation and a strong local currency, it could quite easily justify a 25 basis point cut. However, the Swiss authorities never take price stability for granted and before his departure in September, SNB Chief Thomas Jordan will want to be sure that inflation is sustainably where it is supposed to be. Consequently, it may be slightly more likely that the policy rate will be left on hold for another quarter.