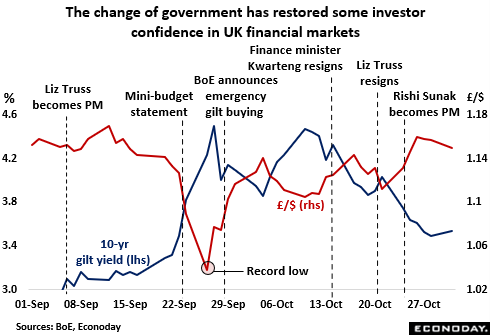

At one point it seemed that the economic and political chaos prompted by the Truss government’s mini-budget in September would completely upend the BoE’s plans for monetary policy. However, the subsequent succession of fiscal policy U-turns and, ultimately, the PM’s own resignation seem to have restored some semblance of normality to financial markets and mean that both official interest rates and the QT programme can resume something close to the paths that the bank originally envisaged. That said, the revolving door at No.10 Downing Street that has seen three prime ministers pass in and out in seven weeks has clearly damaged UK’s international standing. At the same time, fiscal policy will still be more stimulative than before the mini-budget. Consequently, not only over the medium-term are domestic bond yields now likely to be higher than they would otherwise have been but the bank is also widely expected to step up the pace of its tightening on Thursday.

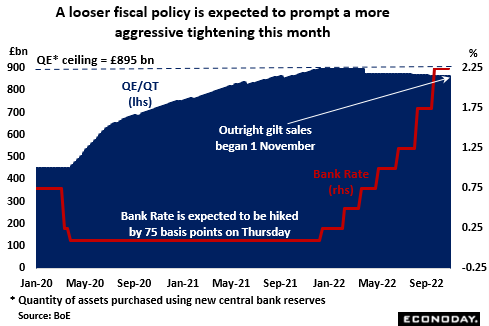

The previous government’s proposals amounted to unfunded net tax cuts of some £45 billion a year through fiscal 2026/27 and the bank was quick to indicate that their inflationary implications would require a significant monetary response. As it is, most of the measures have been either abandoned or at least tempered and gilt yields are now back down to the levels seen just prior to the mini-budget. However, the remaining fiscal black hole is still thought to stand somewhere close to £35 billion. This implies a reduced boost to economic activity (and hence, prices) versus earlier plans, but a boost nonetheless. Consequently, market expectations are for a more aggressive move from the MPC this week. Since the current tightening cycle began last December, Bank Rate (currently 2.25 percent) has been raised at every MPC meeting, initially by just 15 basis points, then 25 basis points and most recently by 50 basis points in both August and September. The consensus for Thursday is a larger 75 basis point hike to 3.00 percent. If correct, this would match the steepest increase since September 1992’s so-called “Black Wednesday” and put the benchmark rate at its highest level since 2008. That said, the MPC’s Swati Dhingra wanted only a 25 basis point move last time while some of the more hawkish members might well want a full 100 basis points. Accordingly, nothing can be taken for granted and another split vote is very likely.

Meantime, having been delayed by a collapsing market that forced the bank to buy bonds (QE) last month. active gilt sales (QT) finally began today. However, for the time being, the auctions, of which there will be eight this quarter, will be limited to the short-and medium-maturity sectors, the longer-end having been hardest hit during the upheaval and so presumably still seen as being vulnerable. The goal remains selling £10 billion of the gilts every quarter which, with around £40 billion of redemptions also falling due, would shrink the balance sheet by £80 billion over the year. In addition, the bank will also look to offload October’s emergency purchases. Even so, there appears to be no rush and the Executive Director for Markets, Andrew Hauser, has warned that it could take the best part of five or 10 years to fully unwind QE. Note too, that the Temporary Expanded Collateral Repo Facility (TECRF), announced on 10 October to help address possible liquidity issues, will remain available until its planned closing date of 10 November.

With the economy and inflation moving in different directions, the bank’s policy decision this week will not be an easy one. However, at least the financial backdrop is now looking much less of a constraint than it did a month ago. Following the appointment of Jeremy Hunt as the new Chancellor of the Exchequer and the subsequent decision to replace of PM Liz Truss with the fiscally prudent Rishi Sunak, both the pound and the gilt market have largely recovered their earlier losses. In fact, the pound, which slumped to a record low against the dollar on 26 September, is currently trading close to 6-week highs. Nonetheless, while investors seem prepared to give the new administration the benefit of the doubt for now, the upcoming Autumn Statement due on 17 November will need to show government borrowing falling significantly over the medium-term or there will be a sizeable negative reaction. As it is, even the promise of a reduced amount of planned fiscal stimulus has still left financial markets expecting interest rates to be raised somewhat further than before the mini-budget. Futures prices currently put 3-month money rates at just under 4 percent at year-end before peaking at close to 4.75 percent in the middle of 2023. Just ahead of the September MPC meeting, next year’s high was seen at only 4.5 percent.

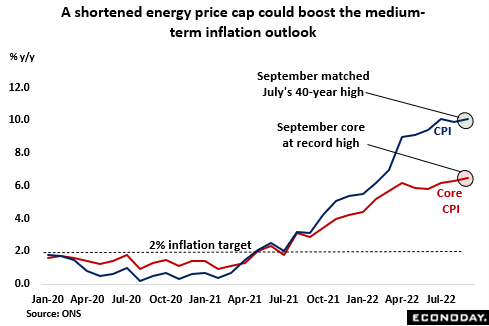

Thursday will also see the BoE update its economic forecasts in a new Monetary Policy Report (MPR). It will do so having seen headline inflation in September regaining July’s 40-year high (10.1 percent) and, more ominously, the core rate (6.5 percent) going one better and claiming a new all-time peak. In fact, the inflation outlook remains highly uncertain. On the positive side, last month the market regulator (Ofgem) introduced the latest energy price adjustment but, courtesy of the Truss government’s Energy Price Guarantee (EPG), average household energy bills will now be capped at £2,500 per year rather than the £3,549 ceiling previously envisaged. This is still an increase of 80 percent or so on the year but means that the boost to inflation will be much less than expected before. To this end, the BoE now seems to think that headline inflation in October will be about 11 percent, several percentage points less than before the new price freeze came into effect. However, against that, the new chancellor has made the medium-term picture more complicated by shortening the duration of the EPG from 24 months to just six. The government will review it next April but, unless extended, energy market developments might mean inflation starts to climb again when, under the former 2-year plan, it would most likely have been coming down.

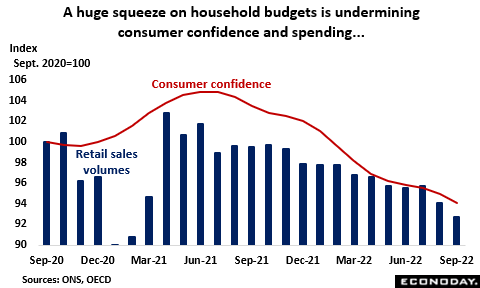

In any event, high and rising inflation is having a significant impact on consumer spending. Retail sales volumes fell in six of the seven months to September with purchases of food, where prices have climbed more than 14 percent on the year, losing ground every month since January. The downturn reflects an ongoing deterioration in consumer confidence that, according to the OECD’s measure, has worsened steadily since the middle of last year and saw yet another record low in September. Weakness in household spending will have been a factor in a probable contraction in real GDP last quarter and will no doubt play a major role in tipping the wider economy into recession by year-end. Total output in August fell for the second time in the last three months and was only unchanged from its level in February 2020, just before the arrival of Covid.

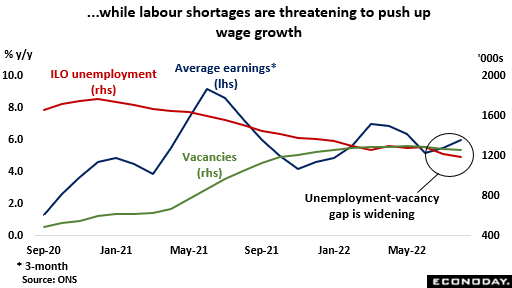

Still, crucially for the bank, a weakening economy has yet to have any real impact on the labour market which remains very tight. Payrolls rose a monthly 69,321 or 0.2 percent in September, extending the unbroken run of gains that began back in March 2021. At the same time, joblessness is still trending down and while at a slower pace than earlier in the year, the ILO unemployment rate has still eased to its lowest reading since the three months ending February 1974. As a result, the shortfall between available workers and vacancies has continued to increase. In turn, this is helping to boost wage growth which, at currently 6.0 percent, stands at its highest mark since May and, more importantly, well above what the BoE MPC would consider as consistent with meeting the inflation target on a sustainable basis.

Nonetheless, for those on the MPC who believe that a looming recession could be more disinflationary than others suppose, they will be concerned that the economic data released since the September meeting have generally been weaker than expected. The UK ECDI, which measures how recent overall economic activity has performed versus market expectations, has spent most of its time below zero and so in negative surprise territory. More of the same would increase the risk of the downturn proving steeper than anticipated, in turn potentially lessening the need to raise Bank Rate. This may be of limited importance to policy with inflation currently so high and will not stop additional tightening but it could quicken the pace at which interest rates are cut as and when the policy cycle finally turns.

In sum, the recovery in domestic financial markets to something more akin to normal trading conditions over the last couple of weeks has made the November BoE MPC’s job a lot simpler than seemed likely in late September. Even so, the bank still faces an added fiscal stimulus at a time when the labour market is tight and inflation already in double digits. Consequently, another increase in Bank Rate on Thursday looks to be nailed on. The majority vote will probably favour 75 basis points but expect dissenters on either side to underline the heighted level of uncertainty that continues to surround the economic outlook in general.