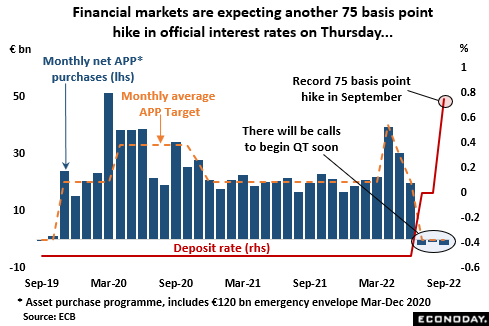

Financial markets are convinced that Thursday’s ECB announcement will include another sizeable increase in key interest rates. In line with the last move in September, the only uncertainty is about the magnitude. The consensus is for another record-equalling 75 basis point hike that would put the deposit rate (still the main policy rate due to the abundance of excess liquidity) at 1.5 percent, the refi rate at 2.0 percent and the rate on the marginal lending facility at 2.25 percent. However, 75 basis points is not a done deal as last month a number of Governing Council (GC) members wanted just a 50 basis point increase on the grounds that a possible recession would reduce inflationary pressures of its own accord. And more and more members are now talking up the likelihood of (at least a) limited downturn in 2023. That said, an increasing number are also stressing the need for rates to be raised above the neutral rate, typically thought to be in the 1.5-2 percent range, so whatever the final decision, it will surely not be unanimous.

This week’s gathering will almost certainly involve some discussion of QT. Currently, the bank is committed to fully reinvesting maturing QE assets acquired under the asset purchase programme (APP) “for an extended period of time” after interest rates began to rise. For the PEPP, which was terminated in March, full reinvestment is scheduled to remain intact until at least the end of 2024. However, the ongoing rise in inflation has prompted some of the more hawkish members (notably Bundesbank President Joachim Nagel) to break ranks and call for QT to begin much sooner. An immediate move on this front is still unlikely, especially given recent volatility in the Eurozone bond markets, but there might be some hints about moving in that direction early next year.

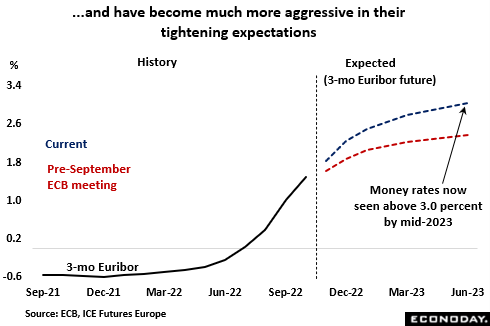

QT or no QT, financial markets have become all the more convinced that key interest rates are nowhere near their peak. From currently just above 1.50 percent, futures markets see 3-month money rates climbing to around 2.30 percent by year-end, about 30 basis points higher than expected just before September’s policy meeting. By the middle of 2023, rates are put above 3.0 percent implying significant monetary tightening still to come. If correct, pressure on bond spreads is unlikely to go away. As it is, the first week of the month saw investors dumping Italian BTPs at the fastest pace since the Covid pandemic first struck and such sales temporarily increased the 10-year spread over German bunds to around 250 basis points, probably about as wide as most ECB members would regard as acceptable. Such concerns may help to limit just how far and how quickly future tightenings are delivered. That said, specifically designed to cap bond spreads, recall that the new Transmission Protection Instrument (TPI) provides a fallback option should serious fragmentation become a real risk.

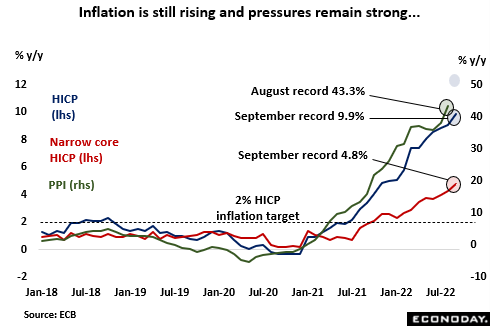

There has been little good news for the ECB regarding inflation. In fact, the September data were especially poor with yearly rates for both the headline HICP (9.9 percent) and the narrow core (4.8 percent) climbing surprisingly sharply and registering yet more all-time highs. To make matters worse, the steep upward trend in producer prices has shown no sign of easing. The August report included a near-record 5.0 percent monthly increase that lifted the annual inflation rate to an unprecedented 43.3 percent, a rise of nearly 30 percentage points from a year ago. Inevitably, overall HICP inflation continues to be heavily influenced by the energy market and recent developments here have been mixed. Worries about slowing global growth saw benchmark oil prices begin to slide in early June and, at $74 a barrel in late September, West Texas Intermediate (WTI) was trading well below the $80 a barrel mark seen just before Russia invaded Ukraine. However, OPEC+’s decision to cut supply by fully 2 million barrels a day earlier this month seems to have at least partially stabilised the market and put a floor under WTI prices above $80 a barrel.

In terms of domestic pressures, Eurozone wage data are only available quarterly and are tardy at best. However, the latest, for the April-June period, showed a 4.1 percent yearly rise, up from 3.7 percent in the first quarter and about double the long-run average. This will not sit well with the ECB which remains very alert to the possible second-round effects of sustained high inflation. The acceleration here is consistent with a labour market that, despite the increasingly sluggish real economy, remains very tight. So far in 2022, joblessness across the region has fallen by nearly 600,000 or 5 percent, in turn reducing the unemployment rate to a record low of 6.6 percent. At the same time an ongoing shortage of available workers has seen the vacancy rate increase in each of the last eight quarters, reaching an all-time high of 3.2 percent in the April-June period.

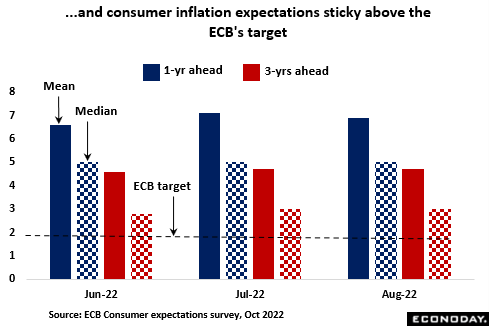

Just as worrying for the ECB, there has also been little evidence that higher interest rates have had much impact on how households perceive future inflation. According to the ECB’s latest consumer expectations survey (CES), inflation over the coming year (median 5.0 percent) and in three years’ time (median 4.7 percent) is seen remaining very sticky around the levels anticipated before interest rates were first hiked. As such, they are still well above target. This view was broadly supported by the EU Commission’s economic sentiment survey which found household expectations last month climbing back to around their levels in June. Expected selling prices in manufacturing and services similarly picked up and all gauges were markedly higher than their respective historical norms.

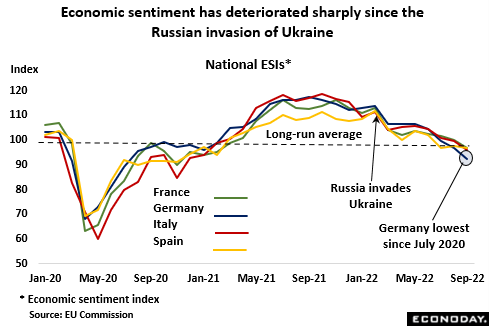

However, the same survey also points to a sustained, sharp, and widespread, deterioration in Eurozone economic sentiment. For the region as a whole, the composite index has fallen every month since Russia moved into Ukraine and in a number of cases the declines have been amongst the steepest seen outside of the Covid period. Indeed, confidence in September hit its lowest level since November 2021 at the start of the Omicron wave. All of the larger four member states have seen marked falls with the slide in Germany, now at its weakest level since July 2020, particularly acute. Third quarter Eurozone GDP might have kept its head above water but with the flash October PMI survey finding private sector business activity contracting at the fastest rate in 23 months, the fourth quarter is very likely to see total output post an absolute decline. In any event, aggressive ECB tightening combined with possible energy shortages over the winter must make for downside risk.

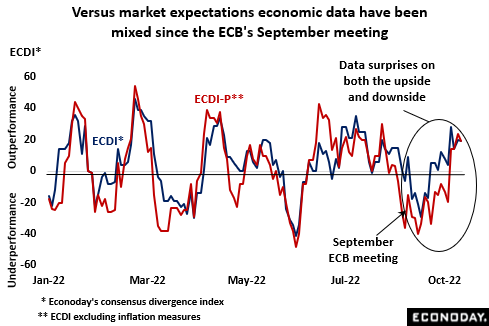

That said, at least since the September meeting there has not been any sustained downside bias to the surprises in the economic data. Econoday’s consensus divergence index (ECDI) which measures how recent economic activity in general has performed versus market expectations, has been both positive and negative. This indicates that the forecasters have broadly got the big picture right in which case any recession should not be significantly deeper than currently discounted. Inflation is clearly the brightest blinking dot on the central bank’s radar currently but any signs of a surprisingly sharp downturn in the real Eurozone economy would probably at least dampen the appetite for large interest rate hikes over coming months.

The economic outlook remains heavily dependent upon the energy markets. On the bright side, helped by falling demand, natural gas storage sites in the EU are now around 92 percent full and, in Germany, even achieved a 95 percent November target in mid-October. Nonetheless, winter will be a serious test of the region’s energy policies and severe weather would only add to the risk of power cuts or blackouts. Ultimately, such an eventuality might even trigger an unexpectedly sharp fall in inflation and reduce the terminal level of interest rates. However, for now, a near-double digit pace of price rises is simply unacceptable. Recession or not, the ECB will feel obliged to move aggressively again on Thursday and anything less than another 75 basis point hike would be a surprise.