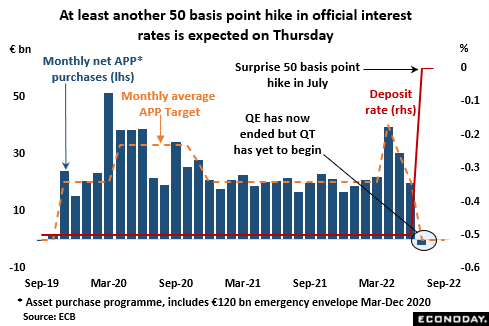

Having been surprised by the magnitude of the interest rate hike in July, the majority of investors now believe that the ECB is set on front-end loading its tightening policy as it tries to bring inflation back under control. Forward guidance went out the window with July’s 50 basis point move that was double what the central bank had pre-announced in June and Subsequently President Lagarde has indicated that policy will now be set on a month-by-month basis and adjusted according to the latest data. To this end, the market call is that Thursday’s announcement will include at least another 50 basis point rise and, following recent surprisingly hawkish comments by several Eurozone national central bank governors, quite probably even a record 75 basis point increase. Chief Economist Philip Lane still seems to favour an incremental tightening path but clearly some on the Governing Council (GC) want the monetary screw to be turned more quickly. The more aggressive approach would raise the deposit rate (the main policy rate due to the abundance of excess liquidity) to 0.75 percent, the refi rate to 1.25 percent and the rate on the marginal lending facility to 1.50 percent.

Meantime, although QE finally ended in July, QT has yet to begin. The bank is fully reinvesting maturing QE assets acquired under the asset purchase programme (APP) and in July indicated that it would continue to do so “for an extended period of time” after rates began to rise. For the PEPP, which was terminated in March, full reinvestment will remain intact until at least the end of 2024. Such action will help keep the ECB’s balance sheet broadly stable. However, with inflation moving further above target, some GC hawks are pressing to start talks about outright asset sales now and it may yet be that active QT begins a good deal earlier than seemed likely just a few weeks ago. Any move on this front would tighten policy still further.

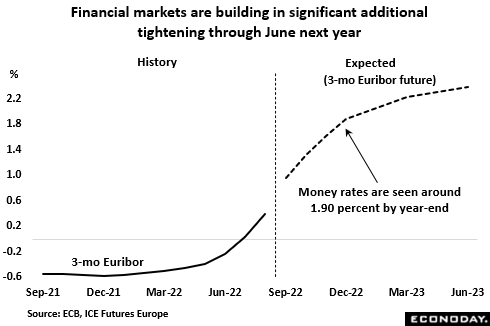

In any event, financial markets are convinced that key interest rates have some way to climb yet. From 0.76 percent currently, futures markets see 3-month money rates at around 1.90 percent by year-end and almost 2.4 percent by the middle of 2023. Rising short-term borrowing costs will continue to put upside pressure on bond yields, particularly those in the higher indebted countries so investors will be listening out for any additional information on the Transmission Protection Instrument (TPI). This was introduced in July and is specifically aimed at limiting bond spreads to strengthen financial stability and ensure the smooth transmission of policy across the region. So far, the bank has indicated that the scale of any TPI purchases will be conditional upon meeting a range of fiscal and other criteria and will depend on the severity of the risks being faced. Importantly though, purchases are not restricted ex ante.

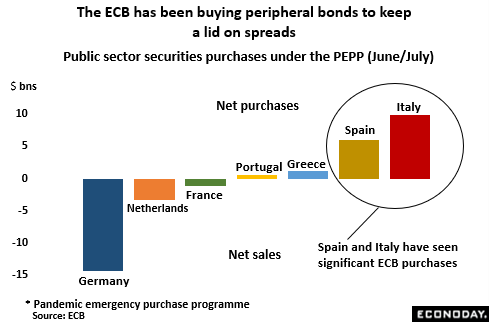

As it is, the ECB has been busy behind the scenes adjusting the composition of its pandemic emergency purchase programme (PEPP) to protect the more vulnerable markets. Indeed, reinvestment from the PEPP remains the first line of defence and the bank has felt obliged to buy sizeable amounts of Greek, Portuguese and, in particular, Spanish and Italian bonds using the proceeds from sales of their maturing German, Dutch and French counterparts. Information is only available on a bimonthly basis but data for June and July put net Italian purchases at some €9.8 billion and net Spanish buying at €5.9 billion. The acquisitions were largely funded by net German sales of €14.3 billion so as not to add to QE. Of note, Italy could soon offer a sterner test of the ECB’s ability to control market volatility as snap elections, due on 25 September, are expected to see a swing to the populist parties. Such an outcome could potentially jeopardise the attainment of key fiscal policy targets and so restrict the ECB’s ability to buy BTPs as well as risking stalling the disbursement of vital EU recovery funds.

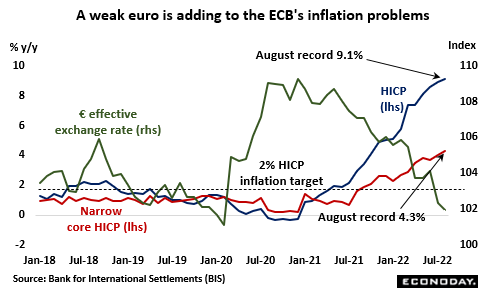

With Russia having steadily reduced and now, essentially cut, gas supplies to Europe, inflation developments since the July meeting have been disappointing. The flash August HICP hit a 9.1 percent yearly rate, up from July’s final 8.9 percent and yet another record high. At 4.3 percent, the narrow core rate gained an even larger 0.3 percentage points and similarly achieved a fresh all-time peak. Moreover, according to the bank’s own July survey, inflation expectations are on the rise too with households seeing the total 3-year ahead rate at 3.0 percent, up from 2.8 percent in June. Not helping matters is the weakness of the euro, a development that the minutes of the July meeting highlighted as being of increasing concern. Measured against a basket of currencies the euro has lost about 7 percent since the start of last year and, more importantly for inflation, just yesterday saw its weakest level versus the dollar in two decades. Exchange rate weakness at a time of rising global inflation has made the ECB’s job all the harder and it would not be surprising to hear President Lagarde makes some comments to the effect that current levels are not seen favourably.

Thursday’s announcement will be accompanied by updated inflation forecasts. Previously these have formed a key part of the forward guidance on interest rates but, as noted in the July minutes, the central bank’s projections have been well wide of the mark in recent quarters. As a result, it seems that actual inflation will now be given greater weight in policy decisions. In fact, more important than the new forecasts anyway may be the outcome of the EU’s emergency meeting of energy ministers on Friday. This will seek to find a way to decouple electricity charges from gas prices as part of a major overhaul of the European energy market. News of the meeting last week saw European benchmark natural gas prices initially fall sharply even though any significant changes are only likely to be delivered slowly. Some member states have already launched price reduction measures of their own but Brussels believes a unified approach would be more effective.

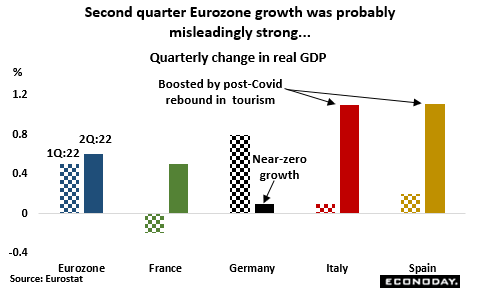

Meantime, despite signs of possibly sharply slowing growth, the Eurozone real economy appears to have been relegated to a back seat in the policy-making process. Indeed, less than two weeks ago Isabel Schnabel, the head of the ECB’s market operations, said that policy should stay on the normalisation path even in the event of a recession. Headline second quarter GDP was surprisingly strong but benefitted from a rebound in tourist inflows into the main holiday destinations, notably Italy and Spain where international tourist spending was up more than 500 percent on the year as Covid restrictions were lifted. Quarterly growth in Germany was just 0.1 percent and a seemingly respectable 0.5 percent rate in France was dominated by exports. Since then, the cost-of-living crisis has become much more acute and borrowing costs have climbed sharply along the entire yield curve on the back of actual and expected ECB tightening.

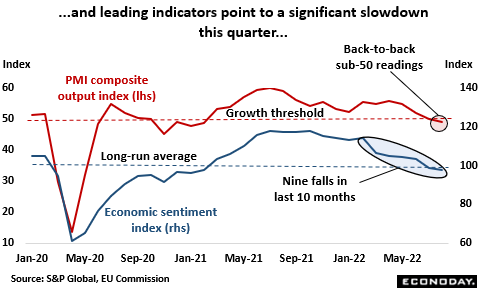

Not surprisingly then, the EU Commission’s closely watched measure of Eurozone economic sentiment has continued to fall and in August posted its worst reading since January 2021 in the midst of the Omicron wave. In a similar vein, the August PMI composite output index chalked up its first back-to-back sub-50 outcome since January/February last year. Business confidence is low and consumer sentiment has slumped to levels well below those seen during the global financial crisis. Record and still accelerating inflation is now clearly negatively impacting consumer spending – discretionary retail sales volumes have declined in four of the last five months – and higher interest rates will further erode disposable income and undermine investment plans. As such, the near-term outlook for private sector domestic demand looks decidedly grim.

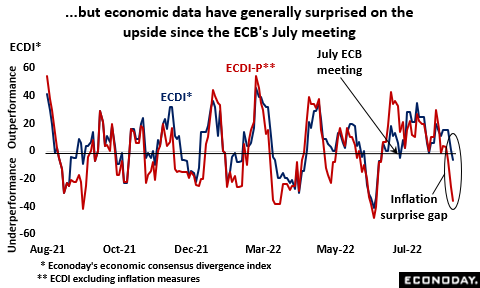

All that said, not only is the ECB now much more focused on tackling inflation than bolstering growth but the Eurozone economic activity has actually been outperforming market expectations anyway. Since the July meeting, Econoday’s economic consensus divergence index (ECDI) has been almost wholly in positive surprise territory. Its inflation-adjusted counterpart (ECDI-P) has largely followed suit although very recently has fallen below zero. However, the unusually wide gap here simply highlights the fact the main positive data surprises have been with inflation and, as the hawks will be keen to emphasise, that is what the ECB policy is all about.

The risk of a recession in Europe is steadily rising and if the impending ECB tightening is as aggressive as financial markets now anticipate, it will be hard to avoid. However, recession or not, the ECB has had enough of overshooting inflation which it clearly now sees as a threat to monetary policy credibility, public trust and, the longer-term economic outlook. Only a short while ago any talk of a 75 basis point hike in key interest rates would have been met with incredulity but desperate times call for desperate measures and anything less now may be seen as simply not enough.