For the first time in a long while, the combination of a weak real economy and slowing underlying inflation has left investors unsure about tightening prospects at this week’s ECB meeting. Forecasters are quite evenly split over yet another rate hike or a pause and, indeed, just last week, the central bank governors from France, Germany, and the Netherlands all indicated that the decision was still up in the air. Consequently, whatever happens, financial markets are likely to react. On balance though, the market consensus seems to be leaning towards no change, bringing at least a temporary end to a policy cycle that has seen nine successive interest rate rises in as many meetings. If so, the key deposit rate will remain at its current record-equalling high of 3.75 percent, the refi rate at 4.25 percent and the rate on the marginal lending facility at 4.50 percent. Cumulative tightening delivered since July 2022 would stay at some 450 basis points.

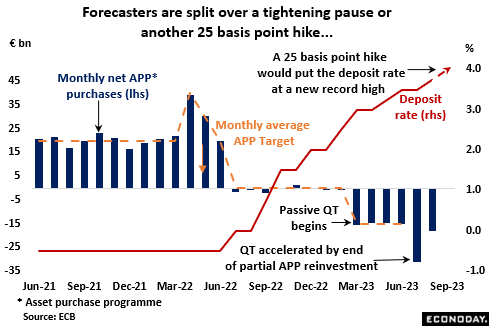

As it is, the pace of QT has been stepped up following the decision to terminate the partial reinvestment of maturing assets in the asset purchase programme (APP) at the end of June. At €24.7 billion, average net asset sales in July/August were well above the previous €15 billion monthly target and total disposals since February now stand at just over €117 billion. However, as of July, outright sales (active QT) had still not been discussed and will probably remain off the table this week. Even so, the main Governing Council (GC) hawks, notably Austrian central bank Governor Robert Holzmann, are keen to bring the pandemic emergency purchase programme (PEPP) into the QE fold. Full reinvestment of the near €1.7 trillion PEPP is still scheduled to run until at least the end of next year but calls for it to be phased out earlier are getting louder. Any move in this direction would be seen as another shift towards a more restrictive policy stance and might be a means of placating the hawks should Thursday’s meeting result in no change in interest rates.

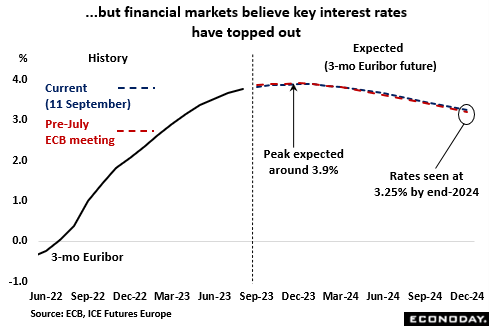

In recent weeks, financial markets have become increasingly convinced that key interest rates have peaked and that the next move will be down. At 3.90 percent, the high currently priced in for 3-month money rates is little changed from that seen just before the July meeting. Anticipated ECB easing in 2024 also remains essentially unrevised, putting rates at about 3.25 percent by year-end. However, that might well be too aggressive for the ECB.

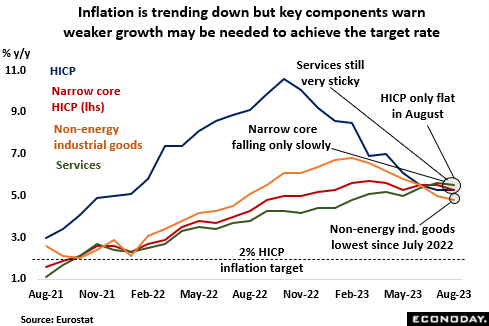

After a disappointingly strong July report, the flash HICP data for August were much better behaved. On the negative side, at 5.3 percent, headline inflation failed to slow for the first time since last October. However, the narrow core rate dropped a couple of ticks to 5.3 percent, matching an 8-month low, while the wider measure omitting just unprocessed food fell an unusually sharp 0.4 percentage points to 6.2 percent, its weakest print since September last year. Moreover, having accelerated almost every month so far in 2023, the service sector rate dipped a tick to 5.5 percent. Still, all the gauges remain far too high and, in particular, progress on reducing the underlying measures has been too slow to instil much confidence that the 2 percent target rate can be reached within an acceptable timeframe.

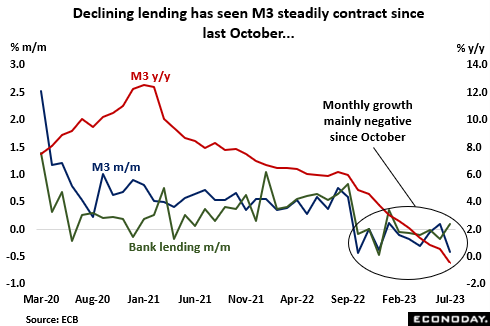

Inflation may be well above target but increasingly restrictive financial conditions have contributed towards a sharp deceleration in the ECB’s main monetary aggregate. Annual M3 growth has slowed from a peak of 12.6 percent at the start of 2021 to minus 0.4 percent in July, its first sub-zero post in some 13 years. Strongly negative base effects have been an important factor but, significantly, monthly growth has also been negative in five of the last six months. Sharply higher borrowing costs and tighter bank credit standards have depressed borrowing by households and non-financial corporations and the ongoing phasing-out of the ECB’s targeted longer-term refinancing operations (TLTROs) has made bank funding all the more expensive. Declining liquidity will add to downside pressure on economic activity.

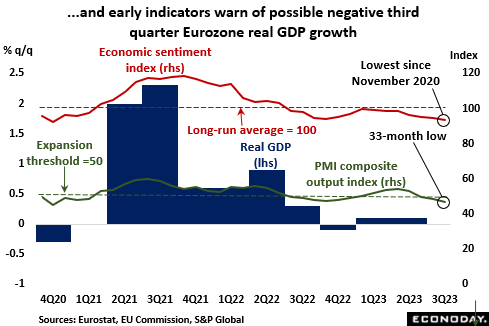

As it is, the Eurozone real economy has barely grown since the third quarter of 2022. The fourth quarter of that year saw a 0.1 percent quarterly contraction and, following the latest round of revisions, both the first and second quarters of 2023 GDP a minimal 0.1 percent gain. Even then, last quarter’s minimal headline advance masked a contraction in Italy (0.4 percent) and another poor quarter for Germany (0.0 percent). The Netherlands and Estonia are both in technical recession and even a solid-looking performance by France (0.5 percent) was essentially just attributable to net exports and inventory accumulation. Early data for the third quarter warn of extended weakness in manufacturing and a declining contribution from services. Consumer confidence is soft – and would be weaker but for a still tight labour market – and overall economic sentiment is at its lowest level since November 2020, during Covid. The August PMI composite output index registered a 33-month low and slumping residential building permits warn of a renewed fall in housing investment. Against this backdrop, the region’s third quarter GDP could easily post an outright decline.

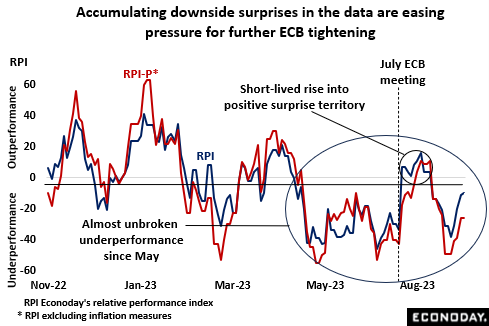

In fact, Eurozone economic activity in general has been disappointingly soft for some time. Apart from a brief rally above zero in mid-August, Econoday’s relative performance index (RPI), which measures how the overall economy has fared versus market expectations, has been consistently in negative surprise territory since May. And the ongoing accumulation of downside surprises is clearly troubling some GC members. It is not as if forecasters were optimistic about the economic outlook in the first place; rather, even predictions of sluggish activity have turned out to be overly positive. All of which must increase the chances that, even if it has yet to begin, a sustainable trend decline in core inflation is not too far away.

For Thursday’s announcement, much will depend upon the ECB’s updated economic forecasts. In June, the projections showed both headline and core inflation above 2 percent through 2025, implicitly conceding that policy was still not restrictive enough. These will need to be trimmed if interest rates are not to be hiked again, particularly since, as the July minutes made plain, most on the Governing Council believed it preferable to tighten monetary policy further than to not tighten it enough. This view may well still hold come Thursday and some members will certainly want to press on with tightening. However, it seems that many, possibly most, members now believe that at least a pause in the cycle is justified. That said, note that even if policy is left on hold, the ECB will almost certainly want to stress that a pause should not be seen as a peak and early rate cuts are simply not an option.