Nothing on the week’s data calendar will compare in importance to the September Employment Situation at 8:30 ET on Friday. Fed policymakers are keeping a close watch on all the labor market data, but it is the September numbers on payrolls and the unemployment rate that will have the biggest influence on the monetary policy outlook. To all appearances, despite a noticeable slowing in some aspects of the US economy, the labor market remains healthy. Layoffs are few, job openings are plentiful, and wages continue to rise, if more slowly. However, there are also signs that some of the imbalance in labor supply and demand is improving.

September is a hard month to forecast depending on the timing of the start of local school years and when the Labor Day observance takes place. This year employers may not be laying off workers from the summer months because they were already understaffed. Some employers may be aggressively recruiting to ensure there are enough workers on hand for the winter holiday period.

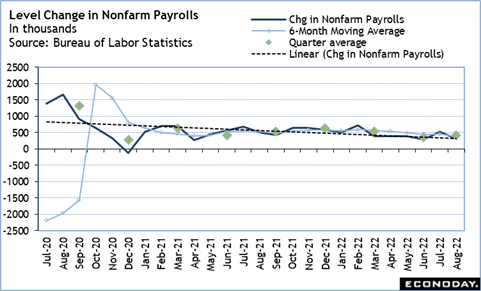

The September payroll numbers for the first two months of the third quarter are averaging 421,000 per month compared to 354,000 in the second quarter and 539,000 in the first quarter. Early estimates for nonfarm payrolls in September are running around 250,000. If this is about right, it puts monthly job gains right on track with the second quarter. This is a solid pace of job gains while suggesting that the labor market is coming into a better supply and demand balance.

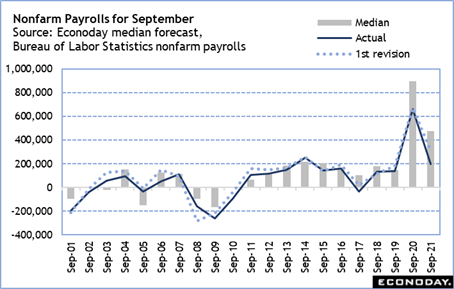

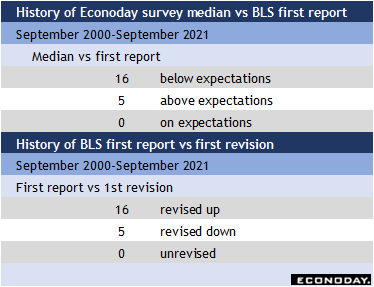

Historically, the forecast consensus for September payrolls strongly tends to come in below expectations and is just as likely to be revised higher in the October report.

The health of the labor market stands in contrast to uncertain expectations for growth in the third quarter. A series of softer reports for September that include ones like retail sales and housing data could pull forecasts into negative territory. After negative growth in the first and second quarter, it will increase the probability that the US has slipped into recession. The devastation from Hurricane Ian in September is likely to be another factor that will depress growth in the third quarter, although almost inevitably there will be a rebound with recovery efforts in the fourth quarter. It is hoped that supply chains for things like building materials will be able to cope with the additional strain and that it won’t cause another push upward for inflation in that sector.