Inflation might have fallen since the SNB’s September Monetary Policy Assessment (MPA) but the central bank has made it very clear that it wants to see yearly price rises sustainably back below 2 percent and that it believes that policy is still overly accommodative. To this end, investors anticipate what would be a third successive increase in official interest rates on Thursday. The policy rate was unexpectedly hiked by 50 basis points in June and by a record 75 basis points in September as the bank made a U-turn on its FX strategy to incorporate Swiss franc strength as a key tool in achieving its price stability goals.

The market consensus is a 50 basis point increase which would put the policy rate at 1.0 percent, its highest level in more than a decade and implying a cumulative 175 basis points of tightening since rates were first raised. Financial markets also expect interest rates to continue climbing in 2023 but, amid signs that inflation might have peaked, tightening speculation has been pared back somewhat and 3-month money rates are now seen topping out around 1.3 percent, well below most other major central bank benchmark rates.

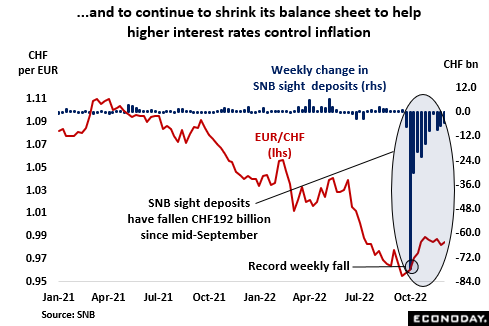

The SNB has also been making sizeable inroads into its bloated balance sheet. Drained through a combination of bill sales and reverse repos, sight deposits at the central bank have fallen more than CHF212 billion or 28 percent since the middle of September and, at CHF542.3 billion, currently stand at their lowest level since February 2017. Indeed, at the end of October, deposits plummeted fully CHF77.5 billion in a single week, the steepest drop since records began in 2011. The shrinkage has helped to underpin money market rates and so reinforced the tightening delivered by the hikes in the policy rate. It has also underlined the bank’s contentment with current levels of the Swiss franc. The slide in the EUR/CHF below parity in July had threatened to trigger a fresh wave of capital inflows into the local currency and it may well have been for that reason that consolidation of the balance sheet was deferred until September. However, with the SNB subsequently indicating that it is prepared to intervene on both sides of the FX market – a statement likely to be reiterated this week – the asset sales have had little impact on the franc and can be expected to continue over coming months and quarters.

Meantime, in recent months CPI inflation has largely behaved itself. Having climbed quite steadily to 3.5 percent in August, the headline yearly rate fell in both September and October and at 3.0 percent in November, matched its lowest level since May. Pipeline pressures in industry have similarly eased and total supply inflation in October was fully 2 percentage points below its May/June high. However, the core CPI rate has proved stickier and at 1.9 percent, last month’s reading was just a tick short of the highest print seen this century. Indeed, the central bank has expressed concerns that price gains have become more entrenched. Moreover, January could well see a move up in the headline rate if, as expected, utility companies raise electricity prices (the only month in the year that they are allowed to do so). The bottom line is that the SNB is not yet convinced that inflation is on a path that would meet its price stability goals within a reasonable timeframe. Consequently, pulling the plug on interest rate hikes now would be premature.

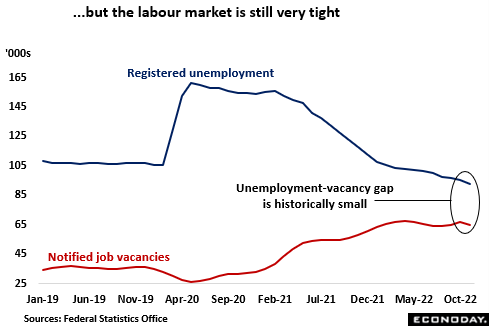

To this end, one of the bank’s biggest concerns is still the labour market. The latest data have offered some tentative signs of cooling with unemployment over the last three months falling only around half that seen in the first quarter. Similarly, over the same period, the increase in vacancies was about a quarter of the rise posted at the start of 2022. Nonetheless, the broader picture still shows a very tight market and with the jobless rate (November 2.0 percent) at its lowest level in more than two decades, inflationary pressure from rising wages is a risk that the SNB will be watching very closely. In fact, the central bank is on record as saying that rising unemployment will not stand in the way of further interest rate hikes.

The chances are that joblessness will indeed begin to climb next year although much will depend upon the global economy and energy prices. Quarterly real GDP growth was just 0.2 percent in the July-September period (and only 0.1 percent in Q1) and weaker demand from key markets in the U.S., the Eurozone and China is likely to undermine exports going forward. Retail sales volumes in October dropped to their lowest level since July 2021 and domestic activity could be significantly impacted in the event of a reduction in gas or electricity supplies. A recent survey found one in three businesses has already taken measures to counter possible energy shortages, mainly through reduced consumption. Consumer sentiment slumped to a new all-time low in October and while still quite well above the 50-expansion threshold, the manufacturing PMI has lost more than 10 points since this year’s peak and currently stands at a 2-year low. Similarly, at 89.5 in November, the KOF’s leading indicator was down fully 17 points since the start of the year and at its worst level since June 2020. All that said, on current trends the Swiss economy could still be one of the better performers in Europe next year.

Nonetheless, having outperformed expectations for much of the first half of the year, the data released since the middle of August have consistently undershot forecasts. Bar a short-lived (and very minor) blip in mid-October, the Swiss ECDI, which measures how recent economic activity in general has performed versus the market consensus, has now been below zero for four straight months. The indications are that the slowdown has been more marked than anticipated, possibly reflecting a larger than expected impact from the fallout from the war in Ukraine and/or what has proved to be surprisingly aggressive SNB tightening.

In November SNB President Thomas Jordan said that the central bank was “prepared to take any and all measures necessary to return inflation to price stability” and the policy measures delivered in recent months certainly support that claim. However, the risk now is that the tightening phase lasts too long as insufficient time is allowed for the policy actions already taken to work their way through the economy. The central bank may have no truck with inflation but any increase in rates in excess of 50 basis points on Thursday could significantly add to such risks.