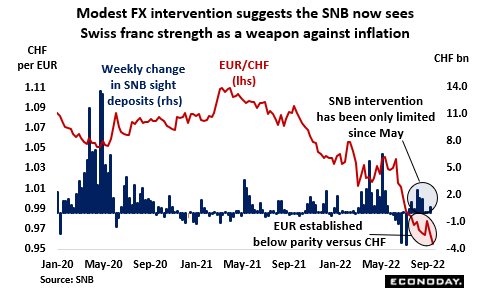

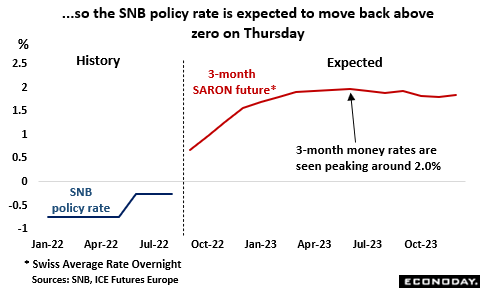

The SNB’s unexpectedly large 50 basis point hike in its benchmark rate to minus 0.25 percent in June was widely seen as indicative of a major shift in policy and proof of the central bank’s desire to get interest rates back into positive territory. With this in mind, the market call is for another increase of at least the same magnitude and quite possibly 75 basis points, putting the rate at 0.25 percent or 0.50 percent at Thursday’s Monetary Policy Announcement (MPA). Significantly, the last tightening occurred with the Swiss franc trading close to what investors thought to be the central bank’s pain threshold and was interpreted as evidence of the bank giving up on its efforts to weaken its currency. Since June, persistently heavy capital inflows have caused the franc to strengthen still further and the EUR/CHF cross-rate now seems to be very firmly established below parity. The SNB continues to make warning noises about excessive appreciation and financial markets remain alert to a possible surprise burst of intervention, but increasingly the sense is that a strong franc is now officially welcomed as a means of helping to keep a lid on inflation.

To this end, and despite the cross-rate breaking below parity in early July, SNB intervention in the FX markets has been quite limited. Weekly sales of the franc have exceeded CHF1.7 billion only once in the last three months having regularly topped CHF2 billion in April/May when at least two weeks saw sales of more than CHF5.5 billion. The apparent refocusing of policy follows from SNB President Thomas Jordan’s comment in June that the CHF was no longer “highly valued”. Indeed, he even went so far as to blame part of the increase in inflation since the March MPA to (limited) local currency depreciation and indicated that the bank would consider buying Swiss francs should the currency weaken too far. However, at that time, EUR/CHF was trading above CHF1.04, or around 9 percent higher than it is today and it remains to be seen how much additional appreciation the bank will tolerate before it feels obliged to act more forcefully.

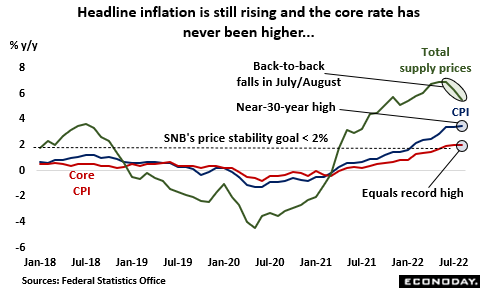

In any event, the SNB is watching inflation extremely closely. Against the current, hugely complex international backdrop many other central banks would see August’s 3.5 percent annual headline CPI rate as a policy triumph. However, the SNB takes its price stability goals extremely seriously and the ongoing widening gap between inflation and its near-2 percent objective mark will not sit at all well. That said, it has not been all bad news as total supply prices (domestic producer prices and import prices) fell in both July and August and, at 5.5 percent, their yearly rate is now at its lowest level since January. Much of the deceleration has been due to weaker energy prices but August’s annual core rate also fell for the first time since the same month in 2020 so it may just be that pipeline pressures are beginning to ease a little. But much will inevitably depend upon the energy markets and households are already expecting a sizeable increase in utility bills in 2023.

Either way, financial markets certainly believe that the June tightening was far from the last this cycle. June’s updated MPA forecasts had inflation slowing next year and in early in 2024 but also showed the rate both above 2 percent and rising by the end of the projection horizon. As such, even then the implicit message was that a policy rate of minus 0.25 percent was still too low to ensure price stability. Futures markets currently see 3-month money rates climbing to more than 1.5 percent by year-end before reaching a peak of about 2.0 percent in the middle of 2023.

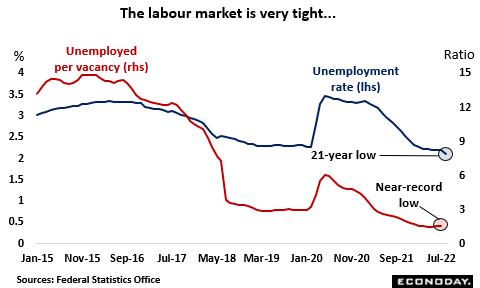

Meantime, the real economy has probably performed much as the SNB anticipated. Second quarter growth eased from 0.5 percent at the start of the year to a still respectable 0.3 percent with reassuringly solid contributions from household consumption and fixed investment. In addition, the labour market remains very tight. In fact, a dip in the unemployment rate to just 2.1 percent in August matched its lowest post since December 2001. Even so, while not as badly hit as most other countries in Europe, the Swiss economy has not been able to avoid altogether the fallout from the war in Ukraine. The country has minimal energy imports from Russia but only produces around a quarter of the energy it consumes. Consequently, it is still very susceptible to international price fluctuations. In addition, drought, low river levels and a lack of snowfall in the mountains have combined to reduce water reserves in many domestic hydroelectric basins to all-time lows. Consequently, the government earlier this month announced that electricity producers would have access to CHF10 billion in emergency state credit should they run into financial difficulty over the coming months. It has also indicated that in the event of a severe gas shortage, it would take more drastic measures.

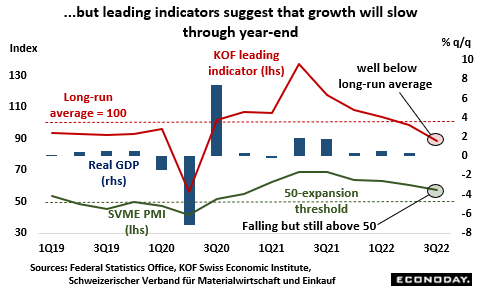

Indeed, as the Ukraine war has rumbled on, forward-looking indicators have pointed to a potentially sharp slowdown in economic growth. The KOF’s leading economic index has slumped more than 16 points since April and in August touched its weakest level since July 2020 in the midst of the first Covid wave. The SVME PM remains much more optimistic but this too is well off recent highs and, according to the OECD, a steady and ongoing decline put consumer confidence last month at its lowest mark since March 2021. The State Secretariat for Economic Affairs (SECO) is due to update its economic forecasts tomorrow.

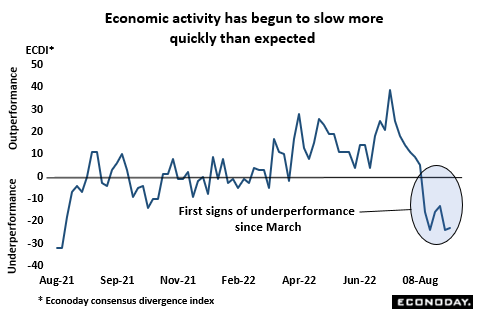

In fact, following half a year of surprising strength, the latest data have warned that the slowdown might be rather more abrupt than anticipated. The Swiss ECDI, which measures how recent economic activity in general has performed versus market expectations, slipped below zero in mid-August. Should it remain there, the signs would be that developments in Ukraine might be having a more negative effect than previously supposed. And if so, it might just temper the aggressiveness with which the SNB delivers any future interest rate hikes.

In sum, having bought huge amounts of foreign currency in recent years trying to prevent CHF appreciation, Thursday’s announcement is likely to re-affirm a fundamental shift in SNB policy that now sees a strong Swiss franc as a key tool in securing price stability.