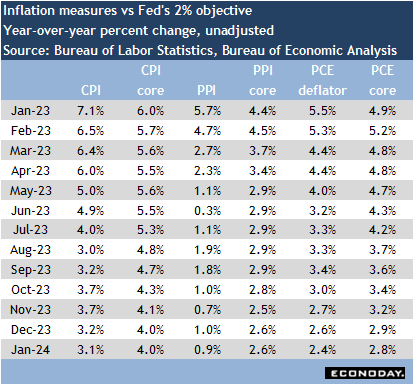

With the release of the January PCE deflator data, the overall inflation picture at the start of 2024 is one in which further progress on bringing inflation back to the Fed’s two percent flexible average inflation target will be a slow grind.

The PCE deflator is the Fed’s preferred measure, but it isn’t the only inflation reading Fed policymakers pay attention to. The CPI is also exhibiting a deceleration in making headway toward two percent.

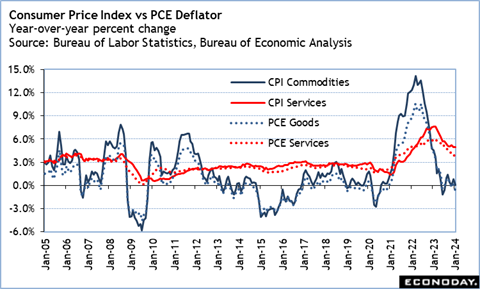

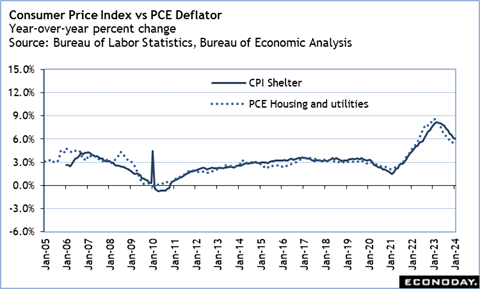

Where all-items indexes are seeing the most progress in disinflation, the core indexes – excluding food and energy – are at more of a plateau. The healing of supply chains and easing in commodities prices have had a major influence in bringing inflation lower, but services costs have yet to respond as completely. Also, the cost of housing – which is roughly 1/3 of consumer expenses – remains a source of upward price pressure.

The careful watch on the performance of inflation is against the background of relatively stable inflation expectations. One-year measures are short term and can be volatile often as gasoline prices fluctuate. Those for the medium term – of more importance to Fed policymakers – have been less volatile and suggest that over time inflation will return to target. This gives the FOMC credibility in its efforts to tame inflation in the present episode. However, the readings also suggest that inflation may remain somewhat higher than it was before the pandemic.