High points for economic data scheduled for August 22 week

By Theresa Sheehan, Econoday Economist

August 22, 2022

Most of the August 22 week economic data will probably take a backseat to anticipation of Jerome Powell’s speech about “The Economic Outlook” on Friday at 10:00 ET at the Jackson Hole Symposium. It has been known in the past for a Fed Chair to use this platform to signal the direction of monetary policy or announce related initiatives like the monetary policy framework update or plans for the Fed’s balance sheet. This time around Powell will likely reiterate much of what he said at his July 27 press briefing or what was in the minutes of the July 26-27 meeting. Policymakers will continue to move to a restrictive stance on interest rates until they are sure that inflation is on a sustained path toward the 2 percent flexible average inflation target. He will probably also note that the reductions in the size of the Fed’s balance sheet will pick up the pace in September and provide less stimulus as well. Powell will be able to cite some tentative improvements on the demand side regarding inflation and supply chain delays, that the labor market remains strong despite the hikes in interest rates and slower economic growth, and that the data for early in the third quarter point to modest expansion. However, it is almost a month before the September 20-21 FOMC meeting, so he will include the caveat that the FOMC is data dependent and there’s plenty of data between now and then.

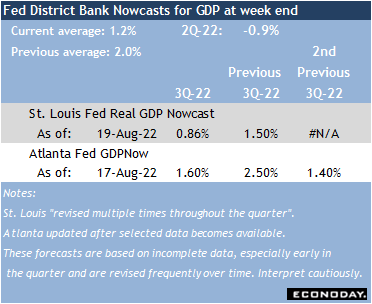

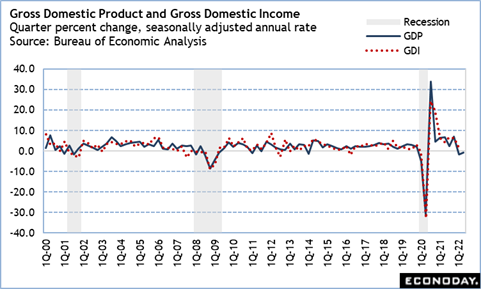

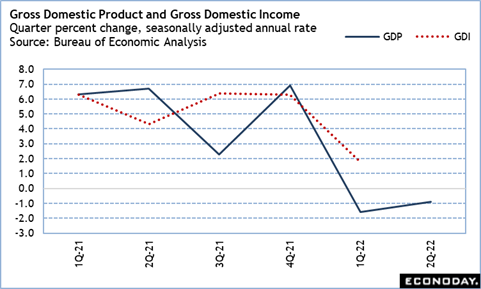

Early forecasts suggest that the second estimate of second quarter GDP at 8:30 ET on Thursday is not expected to be much revised from the advance estimate of 0.9 percent contraction. At this time the third quarter is nearly 2/3 done. As noted above, it looks like the two quarters of negative growth did not presage a recession, and concerns about a downturn will lift a bit. In the first quarter of 2022, some analysts pointed out that gross domestic income (GDI) was positive despite lower gross domestic product. It will be interesting to see if that is the case for the second quarter as well.

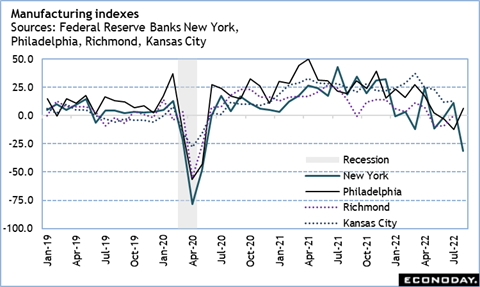

The two earliest surveys of regional manufacturing activity told two different stories for August. The New York Fed’s general business conditions index shocked with a 42.4 point plunge to minus 49.6, while the Philadelphia Fed’s general business conditions index surprised with a 18.5 point gain to 6.2 after two months of contraction. The picture should become clearer after the release of the Richmond Fed Manufacturing Composite Index for August at 10:00 ET on Tuesday and the Kansas City Fed Manufacturing Index at 11:00 ET on Thursday.

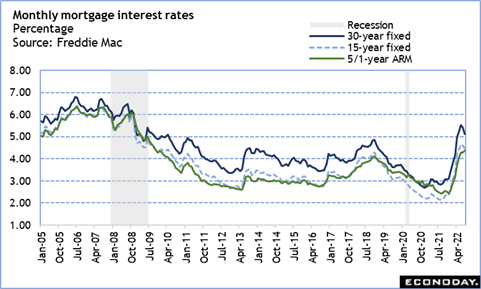

July data on sales of new single-family homes at 10:00 ET on Tuesday and the NAR’s Pending Home Sales at 10:00 ET on Wednesday are expected to share the weakness seen in other data for the housing market. However, a dip in mortgage rates in August may provide a brief bump in sales in the coming month or two reports. Consumers will be getting pre-approved for mortgages now in order to lock in a rate and buy in September and October. Rates are likely to go up again after the September FOMC meeting.

EARLY ORDER DISCOUNT

Use coupon Code

EARLY23

at checkout to save 10% on your order of the 2023 Econoday

MARKET-MOVING EVENTS FOR AN ENTIRE YEAR

Strategic investing and analysis are a lot easier when you can identify patterns and see how economic events and announcements correlate with specific market movements. The Econoday Journal provides a convenient and easy way to follow important economic events every day, every month, throughout the year.

- Enhanced new large format

- Spiral-Bound

- Monthly Monitor Calendar

- Space to write personal Market Impact Notes

- PLUS Our comprehensive Resource Center, featuring all the great information & insights you’ve come to expect from Econoday